GnosisDAO’s GIP-151 was passed with 215% of the required quorum, 49 votes representing a voting weight of approximately 2.15 times the 75,000 $GNO minimum threshold.

The proposal allowed for a one-off pro rata redemption of government bonds $GNO holders to surrender tokens in exchange for a proportionate share of the liquid government bonds. An adopted governance vote on a treasury of this size redefines what governance tokens can be used for.

Until now, the value of a governance token has rested on a pile of soft arguments, such as control over protocol direction, rate switches that could be activated, and treasury subsidies that could drive network growth.

When a DAO can be voted on to return assets to its holders, the token functions as a probability-weighted claim on the balance sheet, regardless of how it is legally classified.

The background report on the previous GIP-150 redemption action cited a GnosisDAO treasury of roughly $223 million, an estimated redemption value of nearly $170 per year. $GNOand a market price of approximately $132, a 27% discount.

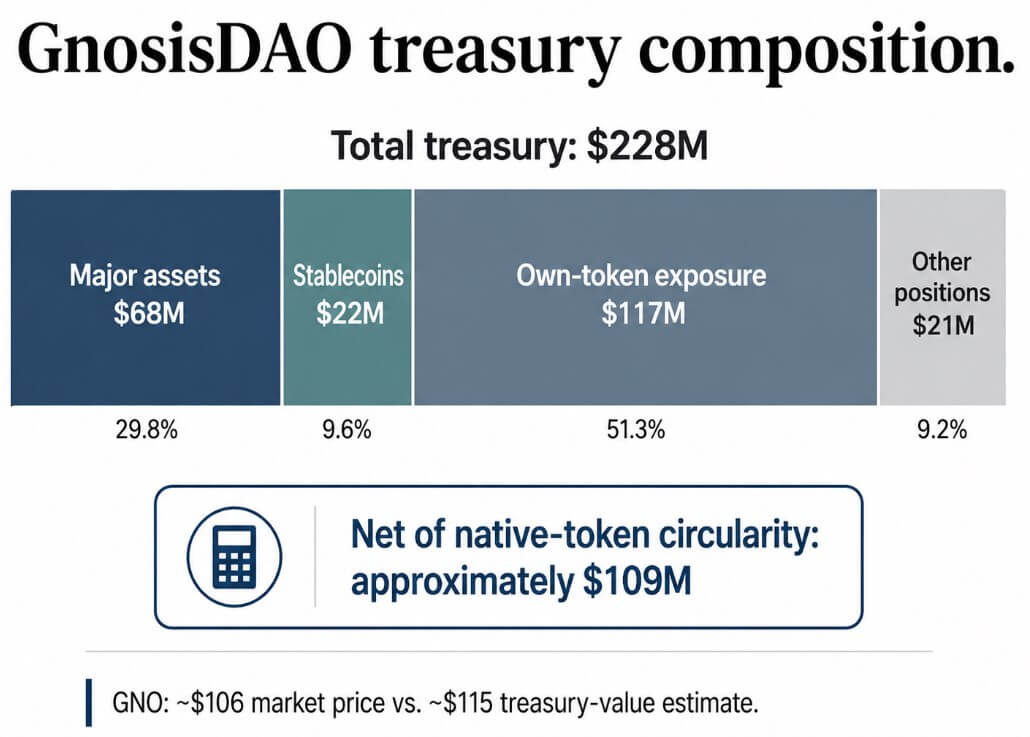

According to current data from DeFiLlama, the total treasury is approaching $228 million, with approximately $68 million in large assets, $22 million in stablecoins, $117 million in native token exposure, and $21 million in other holdings.

After deducting the native token circularity, the liquid treasury is approximately $109 million. This is what DeFi analyst Ignas says $GNO at about $106, versus about $115 in treasury value per token around the time of GIP-151’s passage.

The transaction that validates GIP-151

That discount creates an investable structure that consists of buying tokens below the adjusted state value, accumulating influence over the board, voting for redemption, and closing the gap.

That’s the closed-end fund activism playbook applied to decentralized infrastructure, and Gnosis has now shown it can be executed.

The Investment Company Institute estimated the total assets of the closed-end fund at approximately $791 billion By the end of 2025, there was a market big enough to give rise to decades of activist doctrine around NAV discounts, and DAO’s government bonds are now part of that doctrine.

At one $GNO price almost $104 and a quorum threshold of 75,000 $GNOa position that meets the quorum costs approximately $7.8 million before derailment or opposition occurs. The quorum of 215% reported by GIP-151 implies an actual voting weight of approximately 161,250 $GNOor about $16.8 million at that price.

Insider blocks, delegation structures, eligibility rules and organized opposition all influence whether a given position wins a vote, but the numbers show why governance tokens over large liquid government bonds now carry a control premium that the market has not historically priced.

The transaction generates a simple screen: liquid government bonds per token, market discount to adjusted NAV, quorum threshold, delegated concentration, foundation or multisig veto risk, composition of the government bonds and execution path.

DAOs with legally inaccessible, foundation-controlled or native token-heavy government bonds remain stranded on their discounts.

How governance changes when capital enters the room

Traditional DAO governance assumes that voters are builders, delegates, users, and participants with operational interests in the future of the protocol.

The Treasury activism imports another voter via the NAV buyer, who holds governance tokens to extract balance sheet value and has no particular interest in what the DAO builds next.

A governance forum that used to debate grant allocations, roadmap priorities and parameters for rate changes must now answer a preliminary question: Should the DAO retain these assets and, if so, on what terms?

In the event of a bull case, GIP-151 is executed gracefully, distributing liquid assets, settling illiquid positions via a claim token, and keeping legal friction within limits.

Governance tokens gain a credible new valuation anchor: the probability-weighted right to extract value from the treasury.

Other DAOs with liquid, transparent government bonds and permeable governance are facing immediate demands to justify why their tokens should trade below the value of the assets they manage. A clean execution could pull $GNO towards or shortly above the Treasury estimate of $115, while remaining holders reprice the governance premium.

The bear case involves execution delays, disputes over qualifying offerings, heavy discounts on illiquid assets, or a treasury defense campaign that exposes insider concentration, causing the market to disregard both payout certainty and post-redemption protocol functioning.

The broader risk to the DAO market is that several copy redemption attempts fail simultaneously, demonstrating that most government bond discounts are structurally inaccessible, and the NAV activism thesis deflates before it fully takes hold.

The legal exposure that follows

The SEC’s 2026 crypto guidelines state that crypto assets that are not security assets can still be sold as part of an investment contract when the surrounding facts meet the Howey test: monetary investment, common enterprise, expectation of profit, and dependence on the management efforts of others.

Pro-rata redemption of government bonds gives regulators cleaner facts to conduct that analysis.

Regulators can now more directly ask whether buyers own a governance token to participate in protocol decisions or expect returns from a pooled treasury managed and distributed by others.

The legal risk increases sharply if projects, delegates, activists or market materials explicitly consider tokens as treasury claims.

The distinction between “governance token enabling repayment” and “redeemable government interest” is the line that will be challenged by litigation and enforcement.

A second exposure results from the composition of the government bonds. The Investment Company Act applies to issuers whose principal activity is investing, reinvesting or holding securities, with a 40% threshold for investments in securities set in the statutes.

An adopted repayment mechanism raises the question of whether there is a DAO $ETHstablecoins, tokenized securities, RWAs and LP positions, and can vote to prorate them, is starting to look more like a redeemable asset pool than an operational network.

The debate over the CLARITY Act adds a structural wrinkle, as the Senate bill distinguishes between decentralized and centralized platforms, with the latter subject to obligations like financial institutions, including monitoring transactions and reporting suspicious activity.

A DAO can be truly decentralized at the protocol layer, while concentrating treasury control in insiders, multisigs, or delegation blocks. Gnosis offers regulators a real-world example of that gap.

The DeFi spillover

DAO treasuries fund liquidity programs, grants, market-making budgets, protocol contributors, and LP positions.

Redemption votes, whether standalone or part of an activist norm, force sovereigns to liquidate assets such as stablecoin outflows. $ETH selling, unwinding LP positions and scaling back incentive programs.

The total market capitalization of stablecoins is almost $314 billion, of which Ethereum holds about half, according to DeFiLlama. With the Fed maintaining its target range at 3.50% to 3.75%, the opportunity cost of unused DAO stablecoin reserves is quantifiable and easy to argue in a governance forum.

Gnosis’s risk increases if five or 10 government bond-rich DAOs simultaneously face coordinated redemption campaigns as the resultant asset sales and cuts occur in protocols that share liquidity, validators and grant recipients.

Rook DAO, Fei/Tribe, and Aragon have each shown that DAO treasury conflicts can be resolved through redemption structures.

The ANT redemption of approximately $115 million in Aragon came after a protracted governance battle, which the foundation resolved by returning capital to ANT holders. GIP-151 was created by going through standard governance, above quorum, without the DAO visibly collapsing first.

This procedural route converts a pattern of isolated governance crises into a repeatable strategic tool.

Any DAO that controls a treasury larger than its market cap is now trading at a discount that serves as an activist target. Whether the DAO structures can withstand that, and whether US regulators resolve the legal issue before the market does, are the forward-looking variables that Gnosis has left open.