AlizadaStudios

Western Midstream (NYSE:WES) has seen its share price stagnate with a dividend yield of more than 8%. The company has a market cap of more than $10 billion, and its share price has recovered substantially from its COVID-19 lows. Over the past 2 years though, its share price has stagnated, despite it working to improve shareholder returns.

Western Midstream Ownership

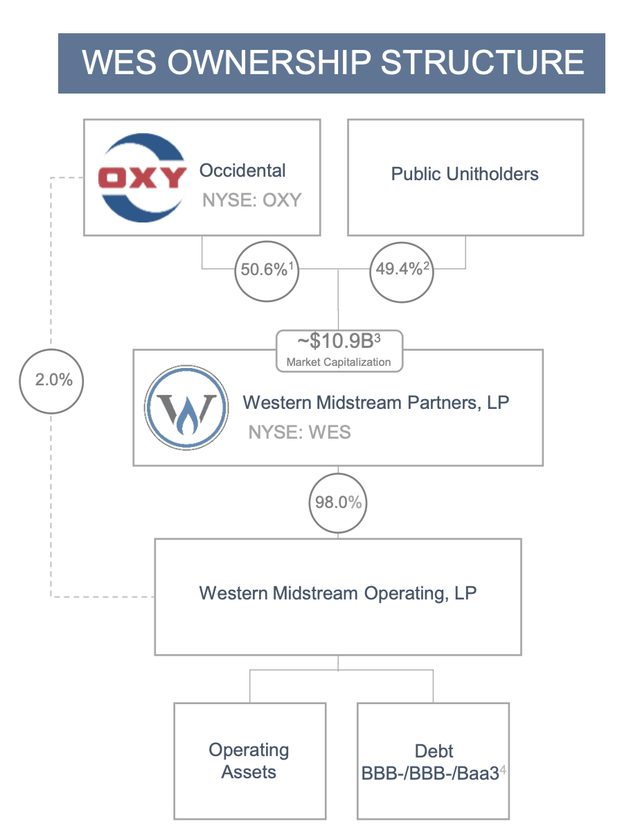

The company has a unique ownership structure where it’s majority owned by Occidental Petroleum (NYSE: OXY).

Western Midstream Investor Presentation

Normally this would be a general benefit, unfortunately, there’s two things here worth noting. The first is that Occidental Petroleum has struggled substantially in the past. There’s been concerns, with debt etc., and it remains a concern that given that Western Midstream is public, selling the stake could provide several billion immediately.

The second is that Occidental Petroleum’s stake in the holding company is 50.6%. Traditionally a holding company could provide a nice way to buy back shares, but here, the company will likely want to maintain its 50+% stake, meaning any sell down will likely be more proportional.

Western Midstream Operational Performance

The company has continued to excel through its operations, with its midstream stake.

Western Midstream Investor Presentation

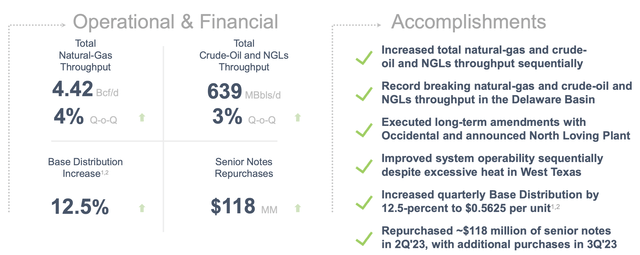

The company’s natural gas throughput was 4.42 billion cubic feet / day, up 4% QoQ. Crude oil and NGL throughput was 639 million barrels / day up 3% QoQ. The company’s continued volume improvement shows the strength of its core portfolio, and the market recovery. The company continues to gain long-term contracts and improve its portfolio reliability.

The company’s steady strength is trickling down to its financials. The company has increased its base by 12.5%, to $2.25 / year annualized. That’s incredibly strong for the company’s $27 share price. The company also managed to repurchase $118 million of its senior notes, and is continuing to reduce its debt load.

Western Midstream Guidance

The company’s overall financial position remains incredibly strong.

Western Midstream Investor Presentation

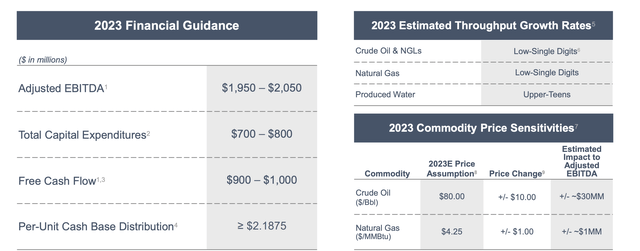

The company is targeting $2 billion in adjusted EBITDA with $750 million in capital expenditures. The company’s distribution is going to cost it ~$850 million meaning a total cost of $1.6 billion. The company has roughly $7 billion in debt that it’s continuing to reduce, highlighting its financial strength, but it continues to have a lofty debt load.

The company expects respectable growth rates, and we expect its cash flow to continue growing.

Meritage Midstream Investor Acquisition

The company has recently made the $885 million cash acquisition of Meritage Midstream.

The multiple on the transaction is 5.5x, which is relatively expensive by most metrics, however, it doesn’t count the potential synergies for the company. The company expects to increase dividends post acquisition, given the financial benefits of the acquisition, and the transition is expected to close for the company going into year-end.

Western Midstream Investor Presentation

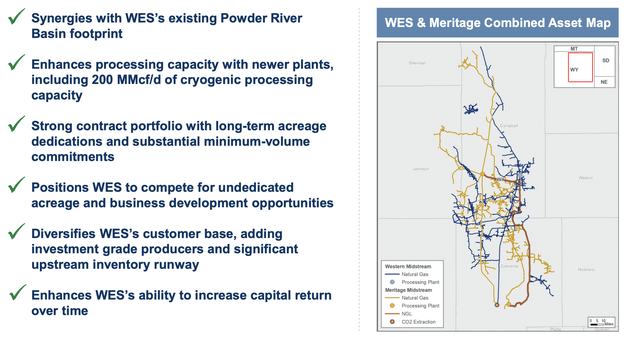

The above picture of the asset shows how it rapidly improves Western Midstream’s Powder River Basin footprint. The company gains 200 million cubic feet / day of new cryogenic processing capacity, and gets access to a large portfolio with substantial volume requirements. It also diversifies the company’s asset base and has strong synergy potential.

The company needs to pay down its debt before interest rates increase and affect its debt too much, but overall, it has strong shareholder return potential.

Thesis Risk

The largest risk to our thesis is the company’s reliance through both ownership and earnings with Occidental Petroleum. Occidental Petroleum is a strong company, but for example, COVID-19 almost bankrupted them. Honestly, without the invasion of Ukraine, their financial position would be dramatically weaker. That reliance has hurt Western Midstream before and could again.

Conclusion

Western Midstream has an impressive portfolio of assets. With the acquisition of Meritage Midstream, for $885 million, the company is dramatically improving its Powder River Basin asset base. The company is continuing to provide its strong dividend yield of more than 8.2%, and it has the ability to continue growing that dividend yield.

The company does have a bit of a debt problem; however, it’s continuing to pay down its debt and we expect it to be able to continue doing so. Overall, Western Midstream’s asset base makes it a valuable long-term investment. Let us know your thoughts in the comments below.