Win McNamee/Getty Images News

Government shutdown averted

The House and the Senate passed a continuing resolution (a stopgap spending bill) to keep the government open for 45 days at current funding levels, with overwhelming bi-partisan support. The Congress will now have more time to pass the 12 appropriations bills (or an omnibus bill) to fund the government for the 2023/24 fiscal year.

It seems like this was actually a surprise to most, even Goldman Sachs expected a shutdown with a 90% probability. Apparently, the House Speaker McCarthy reached out across the party lines and secured the support from the Democrats to pass the stopgap spending bill, and their only sacrifice was the aid for Ukraine – this satisfied the moderate Republicans. The Democrats apparently expect a separate bill to approve the further aid for Ukraine. So, everybody’s happy, except of course the more conservative Republicans, who could move to vacate the Chair and remove the Speaker McCarthy.

What will happen in 45 days? Probably the approval of the government funding for the next fiscal year with another moderate-center compromise. But what does this mean for the financial markets?

The big picture

The US governance is based on a democratic process where the people elect their representatives to the Congress, and the President. Given the diverse population with diverse beliefs, the Congress is also diverse, either right-leaning or left-leaning, which reflects the population’s predominant political view. However, unless one side has full control of the House, the Senate, and the Presidency, the Congress is forced to make a compromise when making the major decisions, like government spending.

So, who really controls the Congress? The Republicans are a coalition of the right-leaning electorate while the Democrats are a coalition of left-leaning electorate, and each side is on a political spectrum ranging from the moderates to the more extreme.

However, in reality, the Congress is controlled by the coalition of the center-right and the center-left, or by the moderates. There are a no major fundamental differences between moderate Republicans and moderate Democrats – thus, there is always a ground for a compromise. That’s the underlying strength of the system – so-called bipartisanship.

Yet, moderate Republicans are more pro-business, thus, their major legislative priority is low corporate taxes and low taxes for the wealthy. Moderate Democrats generally support the social safety net; thus, their legislative priority is government spending. As a result, the moderate-center compromise must have both – low taxes and high spending.

So over time, after numerous “circus shows” of government shutdowns and debt ceilings, and the resulting moderate-center compromises, what are the results? A $33+ trillion in debt and 120% Federal debt/GDP ratio – and that’s the problem. The US debt levels are reaching unsustainable levels.

So, now consider the views of more “extreme” wings of each party? Both sides realize that the US debt levels are unsustainably high. Thus, the extreme left wants to increase the taxes on the corporations and the rich – that’s wealth redistribution. The “extreme” right wants to significantly cut government spending.

The truth is the US government needs to do both: increase taxes and decrease spending – that’s the recommendation of credit agencies. The reality is that the center-moderate coalition is unlikely to do either – increase corporate taxes or significantly cut spending. In my opinion, they will “push the can down the road” for as long as they can.

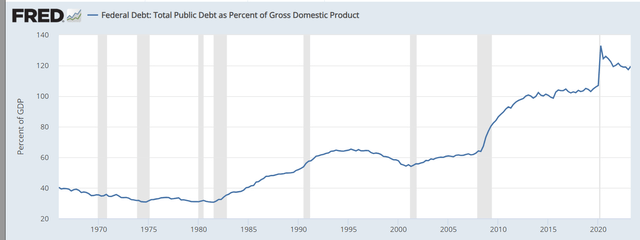

Here is the chart of Federal debt as a percentage of GDP – it’s currently just below 120%.

FRED

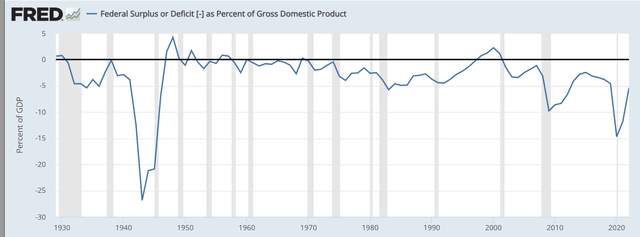

Here is the chart of the federal deficit as percent of GDP. It’s currently above 5%, which is the highest ever outside of a recession or a major war like WW2.

FRED

The effect on the financial markets

The major theme currently affecting the financial markets is the unfolding trend of supply/demand imbalance in US Treasury Bonds – and this is reflected in higher interest rates or yields, and specifically higher real yields.

Specifically, from the demand side, the deglobalization could be causing less demand for US Treasuries from China (due to US-China decoupling) and also OPEC countries (as less petro dollars are recycled into the US Treasuries). In addition, Japan is likely to buy less Treasuries as BOJ gradually tightens monetary policy. These trends are unlikely to reverse.

From the supply side, the supply of US Treasuries is increasing as the US fiscal deficit grows – the US Treasury needs to sell more bonds to finance government spending. In addition, the Fed is currently implementing the balance sheet reduction program, or QT.

Thus, the centre-moderate coalition and their policy of higher spending and lower taxes is running into a real barrier, and that’s the increase in long-term interest rates (TLT). As interest rates increase, the interest payment on outstanding Treasury Bonds could become unsustainable, which could require an even higher supply of Bonds, all while demand is decreasing.

The Fed could stop QT, and restart QE to monetize the government debt. However, the Fed is also facing a major barrier to monetizing government debt, and that’s inflation. Premature easing of monetary policy could de-anchor the inflation expectations and further boost the nominal interest rates.

The “extreme right” position to cut government spending is not really that extreme – rising long term rates really are a major danger to the US economy and the US financial markets.

The US stock market (SPY) has been falling since July as the long term rates started to rise. Unfortunately, long term rates are likely to continue to rise as the US Treasury Bond supply continues to increase due to higher government spending. Thus, the stopgap spending measure and the eventual passing of the spending bill to fund the government could actually be a negative for the stock market.

Implications

The Government shutdown has been averted for now based on strong bi-partisan support. In 45 days, the US Congress is likely to pass the bill to fund the US government for the next fiscal year, also based on strong bi-partisan support.

This is definitely the good news for the economy, for the affected Government employees, and for everybody else. However, this is not necessarily good news for the financial markets. Specifically, the long-term interest rates are likely to continue to rise due to unsustainable debt levels, and consequently the stock market is likely to continue to fall.