RHJ

Thesis

Uranium is the most asymmetric and credible investment idea for the next few years, in my humble opinion. The uranium market is esoteric and dominated by a few countries and several enterprises. Most of them are private-public partnerships and, thus, are not available for us mere mortals to invest in. Apart from junior miners, we have a handful of excellent companies to bet on rising uranium prices. NexGen Energy (NYSE:NXE) is such a case. It is developing one of the best uranium deposits in the world located in Canada with outstanding grade and AISC below $25/lb.

NXE’s balance sheet is neat and clean, while the share dilution is kept to a minimum. Buying one NXE share as an investor, you receive 0.72 pounds of uranium, or three times more than DNN with 0.22 lb per share. The uranium bull market is in its first innings, so now is a good time to start building a position in uranium equities. NexGen, along with Cameco (CCJ) and Denison (DNN), are the best uranium miners in my view. That said, I give NXE a strong buy rating.

Uranium deficit and NexGen

The successful mining company is built on excellent deposits in safe jurisdictions by experienced management, keeping operations tight and efficient. Simply put, I look for Tier 1 mines with high-grade ore, AISC below the industry median, and a life of mine (LOM) of at least ten years run by a team with skin in the game.

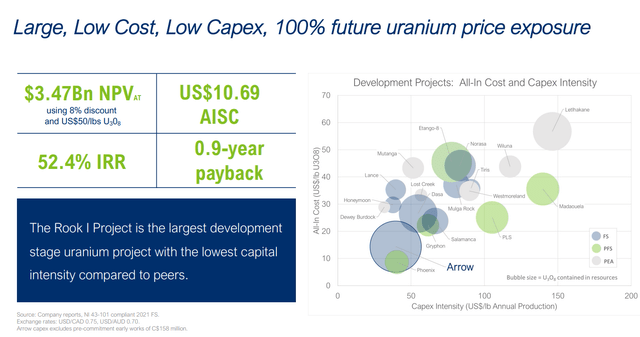

Nex Gen Energy is such a company. It develops the largest uranium deposit outside Kazakhstan with extremely high grade and AISC below $25/lb. The image from the last company presentation shows how impressive the Arrow project is.

Nex Gen presentation

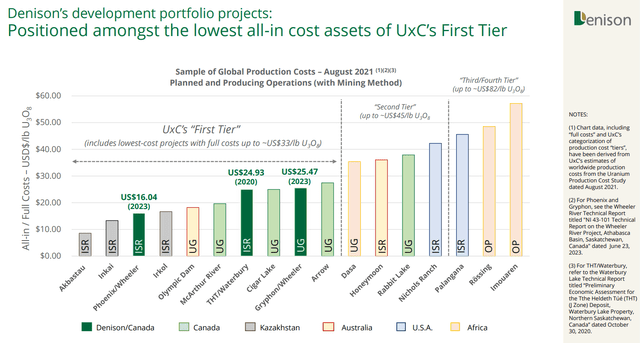

It is among the best in the world, along with Denison Mines (DNN) projects Phoenix and Gryphon. The grade of Athabasca Basin uranium deposits is outstanding. Denison and NexGen major projects have ore grades over 5%, while the world average is below 0.5%. The importance of the grade could not be overstated because it predetermines the cut-of-grade and AISC. The higher the grade, the lower the AISC, hence the cut-off grade. The relation between grade and AISC cost is illustrated on the graph below from Denison’s presentation.

Denison Mines presentation

Only Cameco’s mines in Canada currently have AISC below $25/lb. However, that will change with the NexGen and Denison projects. In the long term, this fact is crucial due to the fragmented uranium supply dominated by a few countries and companies.

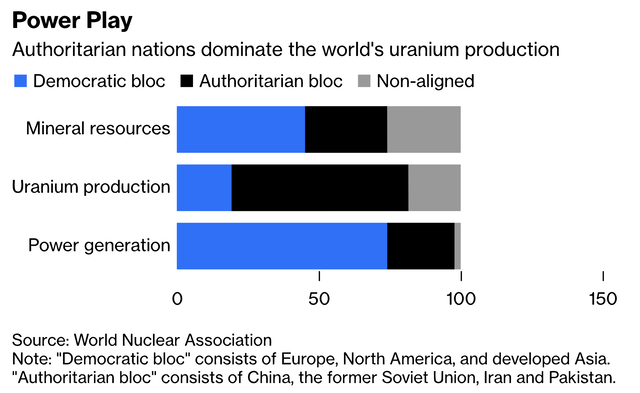

Most of the annual uranium output derives from authoritarian nations gravitating to Beijing and Moscow. The graph below illustrates the distribution of uranium resources, production, and power generation by political regime.

World Nuclear Association and Bloomberg

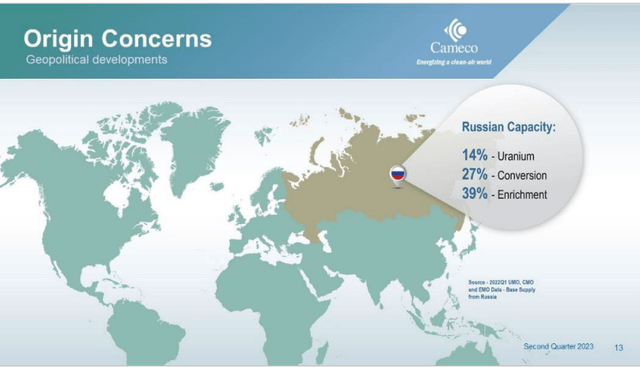

It is no exaggeration to say that Europe and the US depend on uranium imports from countries ruled by authoritarian elites, such as Niger, Kazakhstan, and Russia. The latter is among the top three players at each step of nuclear fuel production. The image below from the last Cameco presentation shows the Russian role in the nuclear fuel cycle.

Cameco presentation

The uranium bull market has the best asymmetry and high credibility among investment ideas. The reasons are rooted in the looming deficit caused by shrinking supply and growing demand.

A few variables drive the uranium market. Due to increased geopolitical fragmentation, energy security will become even more crucial than before. New economic alliances will be created, and the old ones will be destroyed. Hence, global political and economic transformation will lead to changes in commodity supply chains. The West urgently needs to develop its sources of uranium to remain independent from its rivals. Last but not least is the demand created by the clean energy transition trend. Nuclear power has the best metrics (carbon footprint per MW, accidents per unit of power, required area per MW) among all energy sources, including renewables.

On the other hand, the supply is constrained by a chronic lack of investments, political fragmentation, and, more subtly, a growing deficit of mining engineers. Altogether, these factors create a perfect storm for uranium and put miners such as NexGen in a pole position to benefit from those dynamics.

Company Financials

The NexGen balance sheet is more than adequate for a mining company in the development stage. The table below shows a few metrics I use to estimate a company’s solvency and liquidity. The data is from the last financial report.

|

Quick ratio |

6.78 |

|

Current ratio |

6.78 |

|

Long-term debt/Equity |

16.8% |

|

Total debt/Equity |

16.8% |

|

Total liabilities/Total assets |

17.2% |

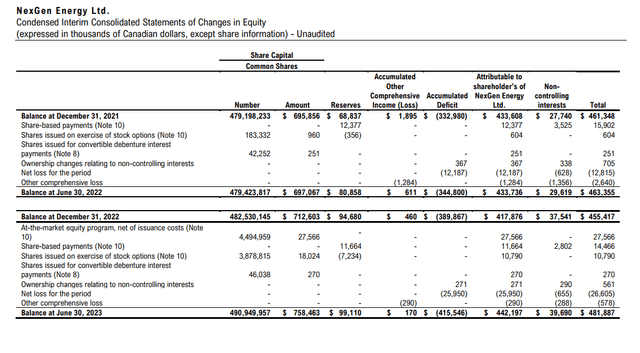

NexGen’s ratios are more typical for enterprises with producing mines. To maintain its balance sheet health, NexGen did not use excessive share dilution as seen below:

Nex Gen financial report

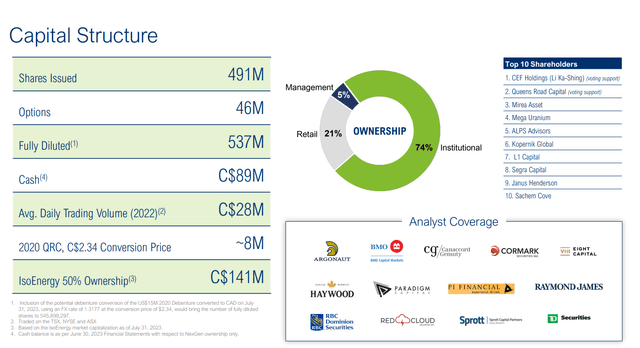

The number of fully diluted shares has grown to 2.2% for the last Q2 and the graph below shows NexGen’s capital structure.

Nex Gen presentation

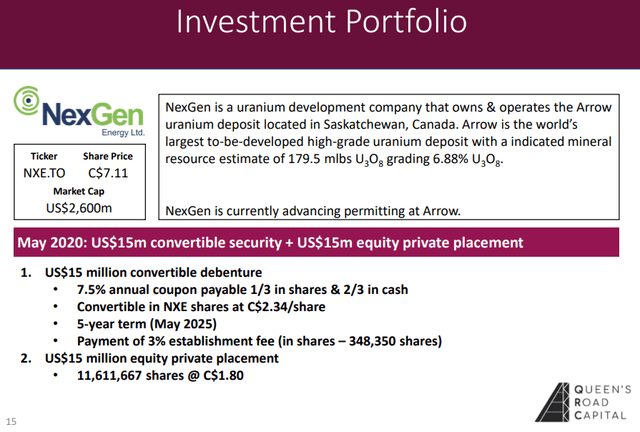

Two things I like to point out. The largest shareholders are CEF Holding and Queens Road Capital. The latter provides financing by acquiring convertible bonds and debentures. Queens Road currently owns 11,611,667 shares and convertibles with a face value of $15 million. More details are provided below on the image from the Queens Road presentation.

Queens Road Capital

On August 31, 2023 Queens Road announced another financing round with convertible debentures. Hybrid debt instruments have a few advantages. A convert makes much more financial sense for successful issuers than a brokered equity raising, as the dilution negatively impacts significantly more than the coupon.

CEF Holding is a conglomerate of Li Ka Shing, one of the most affluent Asians. Warren Gilman, one of NXE’s directors and CEO of Queens Road, has worked for CEF for many years. Mr. Gilman owns 8.16% of Queens Road and 0.11% of NXE. NexGen’s CEO, Leigh R. Curyer, owns 1.02% of the company’s shares.

Company Valuation

NexGen is not producing uranium yet. Thus, to estimate its value, I will use NAV, but instead of owners earning per unit of production, I will apply the company’s pilot project Arrow NPV:

- Net asset value, including Arrow’s NPV

- Plausible Reserves/Fully Diluted Shares and EV/Plausible Reserves

I use the following formulas to estimate plausible reserves and net asset value:

PR (plausible reserves) = 100% * P&P Reserves + 50%*M&I Resources + 30%*Inferred Resources

NAV = 0.8*NPV + cash + inventories + total receivables – total liabilities

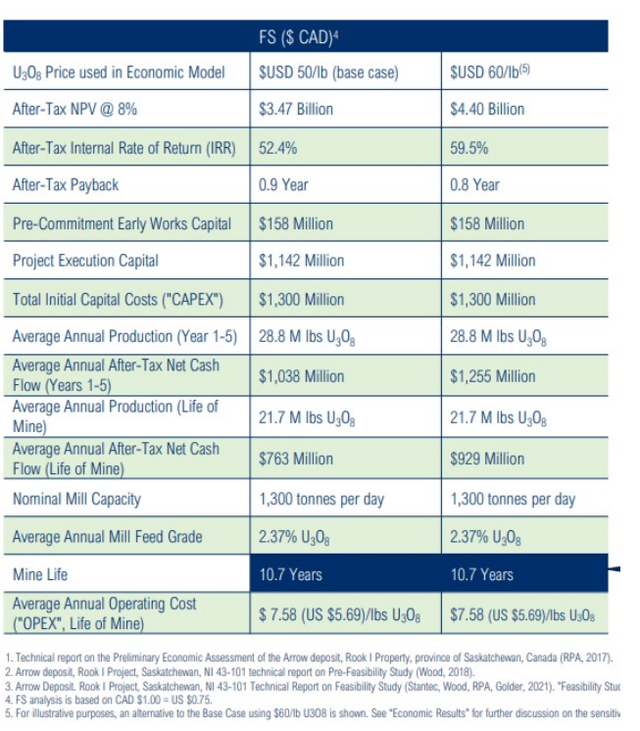

I used NPV from the last company presentation. However, I multiply by 0.8 due to the low discount rate used in the calculations. NXE project is based in Canada, but the 8% discount rate is too good. Going into detail, it is closer to 8.8% – 9.2%. It seems a negligible difference, but such a minor change in the rate leads to notable variation in the outcome. The image below from the last company presentation shows the NPV input data.

Nex Gen presentation

NexGen presentation

I use two scenarios with uranium price at $50/lb (conservative case) and $60/lb (base case).

- Cash $75.9 million

- Short Term Investments $5.4 million

- Total receivables $1.1 million

- Total Liabilities $75 million

- Fully diluted shares 543 million

- Arrow After-tax NPV (uranium at $50/lb) $3.47 billion

- Arrow After-tax NPV (uranium at $60/lb) $4.40 billion

Conservative case NAV = $2.66 billion

Conservative NAV per share = $4.8

Base case NAV = $3.52 billion

Base NAV per share = $6.48

NexGen’s current market price = $6.09 on Sept 21, 2023

I compare NexGen with similar-sized companies developing projects in Canada and the US. Cameco or Centrus Energy (LEU) are not relevant competitors. The former is a fully integrated nuclear energy company, while the latter is a player in its own league. Below are the companies I use to estimate NexGen’s relative value:

- Denison Mines

- Fission Energy (FSSU)

- Uranium Energy Corp (UEC)

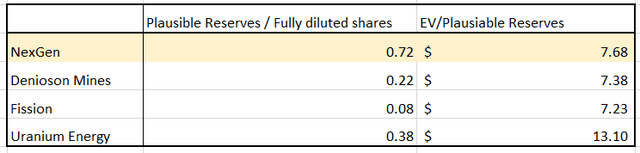

I use Plausible Reserves/Fully Diluted Shares and EV/Plausible Reserve to measure how cheap or expensive NXE is.

Author`s database

Author’s database

NexGen offers 0.72 lb per share, much better than its competitors. The second is Denison, with three times less. On the other hand, to receive those pounds of uranium, we pay $7.68 per lb in line with Denison and Fission. Only UEC EV/PR is significantly higher.

Risk

As a mining company, NexGen carries the following risks:

- Metallurgical

- Geological

- Financial

- Country specific

- Economic

- Operational

More pronounced are metallurgical, economic risks, and operational risks. Geology finds the ore; however, metallurgy tells us how to extract it. The latter means the cost per unit. Arrow seems to be the best uranium mine under development, but till the mines start producing, we are not guaranteed that AISC will match the feasibility study figures.

The economic risk means high inflation and rising interest rates. The former will push the building and operating costs higher, while the latter will increase the cost of financing. The operational risk is too tough to assess for retail investors. However, considering the quality of the management team, operational risk is under control in my view.

The country’s risk is almost nonexistent. NXE projects are in Saskatchewan province, the most prominent uranium region in the world. Thus, all related processes, such as permitting, infrastructure, and supporting services, are already well established. The same is true for geological risk. The area has been explored for decades and thus is well known, and surprises are not likely.

The market risk is always present regardless of the industry. Nevertheless, uranium mining stocks have a low correlation with the broad indexed, as seen by their performance in the last eight months.

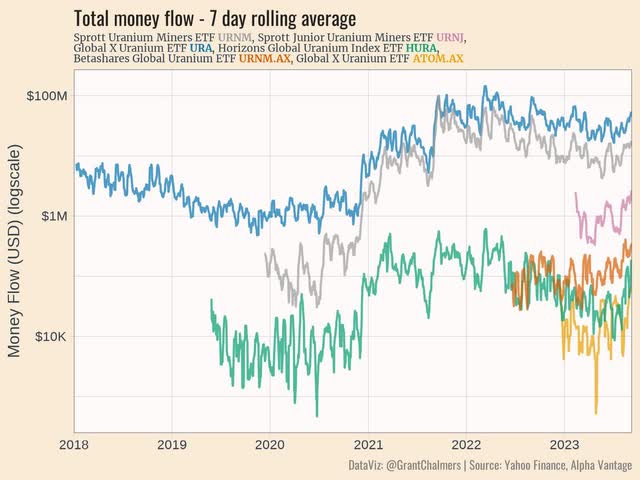

Going deeper into details, one more risk always creeps around impulsive bull markets. I mean the risk of being late for the party. We are observing the first leg of the uranium bull run. The table below shows the inflows of major uranium ETFs.

Alpha Vantage

Once we reach a late stage, that chart will look way different. Instead of flat inflows, they could soar parabolically, i.e., most retail is all in, too. Then, it’s time to reconsider the timing of the investment. However, we are in the first innings, and the risk of being too late is not present in my opinion.

The institutional investors started slowly to recognize the potential of the uranium thesis. Blackrock and ARKK lead the pack by buying Cameco shares. Blackrock fund Brown to Green Materials has Cameco as the second largest position with 3.87% of the portfolio.

That does not mean it will be a smooth ride north. Volatility is inherent in uranium miners’ stocks; thus, investing in uranium must embrace volatility. Do not forget that the latter is an admission fee for exposure to potentially exponential returns.

Conclusion

NexGen is a wager betting on the next uranium bull market. The company develops the Arrow project, one of the best in the world, given its grade, AISC, and resource base. The project has completed the Feasibility Study and is currently preparing Front End Engineering Design. NXE has a healthy balance sheet due to flexible financing provided by Queens Road Capital. NexGen is undervalued measured with a NAV base case scenario. Besides that, for one NXE share, we receive 0.72 pounds of uranium, significantly more than its peers. Considering the company’s quality and value, I give NXE a strong buy rating.