")

Klaus Vedfelt/DigitalVision via Getty Images

At a Glance

Mereo BioPharma (NASDAQ:MREO) finds itself at a pivotal crossroads, both clinically and financially. Since my last analysis, in which I recommended a “Sell,” the firm has notably extended its financial runway, thanks in part to milestone payments and reductions in R&D spending. While setrusumab and alvelestat remain key value drivers, the company has seen a glimmer of opportunity in its oncology candidate, etigilimab, amplified by recent industry data on anti-TIGIT agents. While these positives temper some of the previous concerns, particularly setrusumab’s uncertain long-term efficacy, they tip the risk-reward balance toward a more neutral stance, justifying an update to a “Hold” recommendation.

Earnings Report

To begin my analysis, looking at Mereo’s first half 2023 financial results, several financial metrics stand out. Revenue registered at $9M, primarily from a one-time milestone payment activated by the Phase 3 Orbit study. Notably, R&D expenses contracted sharply to $9.8M, a 41% YOY decline. This is principally due to a $5.5M decrease attributed to the termination of the etigilimab Phase 1b/2 study. On the other hand, administrative expenses increased by 8% to $11.8M, driven by fees associated with corporate activities. The net loss saw a substantial improvement, down to $13.6M from $23.8M in the previous year’s first half.

Financial Health & Liquidity

Turning to Mereo Biopharma’s balance sheet, as of June 30, 2023, the company had about $52.2M in ‘Cash and short-term deposits.’ Over the prior six months, net cash used in operating activities was approximately $16.5M, translating to a monthly cash burn of $2.7M. Post-June, the financial influx from the $9M milestone payment from Ultragenyx (RARE) and $11.5M through the Jefferies’ agreement elevates the liquid assets to an estimated $72.7M. The cash runway, accounting for these additional funds, extends to about 27 months. These numbers are based on historical data, so caution should be exercised when projecting future performance.

Mereo’s liquidity appears robust, especially with the recent injections of milestone and at-the-market payments. The company does have convertible loan notes amounting to around $4.6M in non-current liabilities and $5.2M in current liabilities. While these debts necessitate prudent capital allocation, they don’t overshadow the overall positive liquidity situation. Given this healthy financial status, Mereo seems well-positioned to secure additional financing, especially if timed with key R&D or regulatory milestones to enhance valuation. These are my personal observations, and other analysts might interpret the data differently.

Note: The currency conversions provided above are approximate, utilizing an exchange rate of 1 Pound sterling to 1.24 USD as of the report date, September 19.

Capital, Growth, Momentum, & Ownership

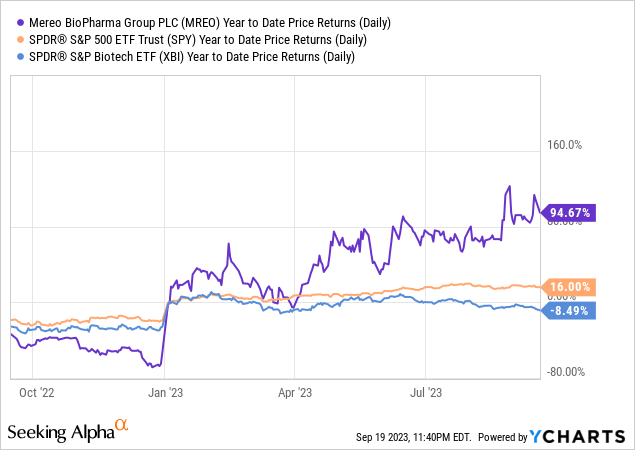

According to Seeking Alpha data, Mereo BioPharma’s capital structure exhibits reasonable liquidity given its cash reserves, albeit its market cap of $182.12M suggests a micro-cap risk profile (more on this below). Leverage remains modest relative to its market cap, providing some financial flexibility. Growth prospects appear mixed, as milestone payments, typically, are uncertain and unsteady. Stock momentum significantly outperforms SPY over a 9-month timeframe, yet is mixed when broader timeframes are considered.

Mereo’s diversified ownership provides some stability, but its 33.74% hedge fund stake can result in price volatility unrelated to its core business metrics. Moreover, the company’s micro-cap status amplifies liquidity and volatility risks. Setrusumab and alvelestat offer both growth potential and event-driven hazards, as their market readiness remains years away. Regulatory challenges and the possibility of dilutive capital measures further complicate the risk landscape.

Mereo BioPharma’s Advancing Pipeline and Strategic Positioning

Mereo BioPharma’s position in the market is notably strengthened by the evolving dynamics in the anti-TIGIT therapeutic landscape, accentuated by Roche’s (OTCQX:RHHBY) recent inadvertent SKYSCRAPER-01 interim analysis. Specifically, Roche’s data, reported in February 2023 based on a November 2022 cut-off, presented an intriguing albeit not yet conclusive improvement in median overall survival with tiragolumab plus Tecentriq over Tecentriq monotherapy—22.9 months versus 16.7 months, respectively. The hazard ratio stood at 0.81, indicating a potential survival advantage that warrants further scrutiny. Moreover, the safety profile showed no new concerns, amplifying the relevance of anti-TIGIT agents like Mereo’s etigilimab, which has concluded its Phase 1b trial and showed clinical efficacy in specific resistant tumor subsets.

Meanwhile, Mereo’s setrusumab, developed in collaboration with Ultragenyx, has delivered encouraging Phase 2 anatomical outcomes for Osteogenesis Imperfecta (OI), a pediatric bone density disorder. Progressing into dual Phase 3 studies, the drug is on track to substantiate its clinical credentials further, and updated data is eagerly awaited.

On the pulmonary front, alvelestat has emerged as a promising contender for Alpha-1 Antitrypsin Deficiency-related lung disease (AATD-LD). The therapeutic candidate is set for critical Phase 3 trials, delineated by positive feedback from regulatory authorities like the FDA and EMA, and its upcoming Phase 2 outcomes are highly anticipated given the targeted specificity of its endpoints.

Collectively, Mereo’s portfolio is well-diversified, encompassing various developmental stages and spanning from rare skeletal disorders to respiratory ailments and cancer therapeutics. This multifaceted approach, now buttressed by favorable industry developments—specifically Roche’s latest anti-TIGIT data—compounds the compelling investment thesis for Mereo.

My Analysis & Recommendation

Given these positive changes, I am moving my stance on Mereo BioPharma from a “Sell” to a more neutral “Hold”. This change accounts for the company’s strengthened financial position and promising clinical developments, particularly in setrusumab and alvelestat. The contraction in R&D expenses and an extended cash runway afford Mereo a financial buffer that cannot be ignored, particularly in an industry sector that hasn’t fared well recently.

While the clinical progress of setrusumab and alvelestat remains promising, key data readouts that can definitively tip the scale in their favor are still on the horizon. The clinical impact of these assets, especially regarding setrusumab’s fracture-reduction efficacy and alvelestat’s patient-reported outcomes, remain major question marks. Thus, prudence demands a cautious approach.

The newfound focus on etigilimab, thanks to Roche’s anti-TIGIT data, adds another layer of complexity to Mereo’s valuation. While this might suggest the potential for upside, the asset is still in the early stages and its role in the broader oncology market remains to be validated. However, upcoming data from the ESMO presentation in late October could be a major catalyst.

To summarize, while uncertainties in Mereo’s portfolio persist, the risk/reward balance is finely poised. The company has some runway to navigate these uncertainties, and until we see more conclusive data or a significant catalyst, it might be prudent to hold the stock and await further developments. Keep a close eye on upcoming milestones, including clinical data releases and potential partnerships, as they could serve as pivotal moments for re-evaluating the stock’s status.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.