UniqueMotionGraphics

Chinese electric vehicle companies have seen a significant improvement in their delivery prospects in the last two months. Companies that benefit from the unleashing of pent-up demand include Li Auto (NASDAQ:LI), NIO (NIO) and XPeng (XPEV). As a result, Li Auto has meaningful (vehicle margin) surprise potential when it presents Q3’23 earnings. Vehicle margins have been under pressure due to weakening pricing (thanks to Tesla (TSLA)’s price cuts) and weak demand at the beginning of the year, but marginally improved in the second-quarter.

Given the rebound in demand and broad-based delivery momentum for all three EV companies, I believe Li Auto is set to report yet another sequential increase in its electric vehicle margins for the third-quarter. The delivery outlook for Q4’23 is also likely going to be very strong — I expect a raise in the quarterly delivery outlook to 115-120 thousand EVs — which could potentially create an upside catalyst for Li Auto’s shares as well.

Previous rating

I recommended Li Auto as a strong buy after the company reported second-quarter earnings which showed that the company was moving towards its first-ever full-year profit. Additionally, I now see a major margin improvement on the horizon as well as a strong delivery outlook for Q4’23… given that Li Auto keeps growing significantly faster than the competition. Considering that shares have dropped 30% from their 1-year high at $47.33, I believe that the risk profile has improved dramatically for the benefit of long term investors ahead of the Q3 earnings release. Li Auto is now my 6th largest portfolio position.

Li Auto continued to outgrow the EV competition in September

Li Auto remained in a class of its own in September. At the beginning of the month, the EV maker reported that it delivered a massive 36,060 electric vehicles to customers in September… which was more than twice the delivery volume of companies like NIO or XPeng. Both companies delivered between 15-16 thousand EVs last month. Li Auto’s realized growth rate in October was 212.7% which means that the EV maker grew its deliveries about 4.9 times faster than NIO and 2.6 times faster than XPeng. Li Auto is on a winner streak here and already executed well in the first half of the year in which it saw considerably stronger delivery momentum than its EV rivals…

|

Deliveries |

Jul-23 |

July Y/Y Growth |

Aug-23 |

August Y/Y Growth |

Sep-23 |

September Y/Y Growth |

|

LI |

34,134 |

227.5% |

34,914 |

663.8% |

36,060 |

212.7% |

|

NIO |

20,462 |

103.6% |

19,329 |

81.0% |

15,641 |

43.8% |

|

XPEV |

11,008 |

-4.5% |

13,690 |

42.9% |

15,310 |

81.0% |

(Source: Author)

Surprise potential in Q3: margin expansion and delivery guidance

Given the extremely high volume of EV product sales driven by strong demand in the third-quarter, I believe Li Auto has a lot of potential to put an impressive earnings report for the third-quarter on the table.

Li Auto, most important of all, could make a difference with its Q3’23 earnings report and report a second quarter of sequential margin growth.

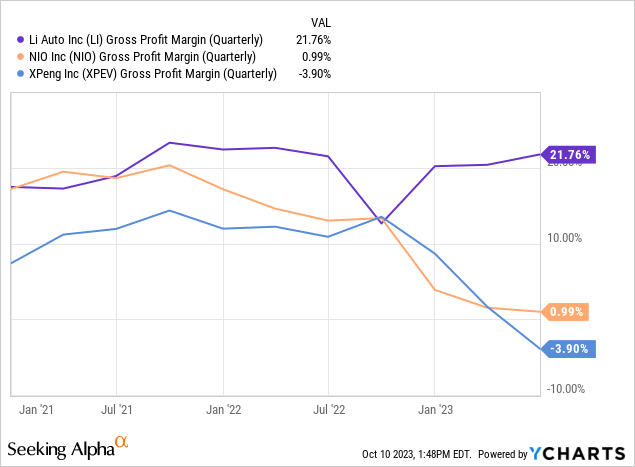

Li Auto’s vehicle margins marginally deteriorated 0.2 PP in the first-quarter, but have shown signs of a recovery in the second-quarter… which is when they expanded 1.2 PP Q/Q. Given strong demand for Li Auto’s vehicles and growing scale, investors definitely would want to pay some attention to growth in margins: I estimate that the EV firm could see 2-3 PP sequential margin growth in the third-quarter and Li Auto could definitely surprise to the upside here.

For context, NIO’s vehicle margins rose 1.1 PP in Q2’23 while XPeng suffered a 6.1 PP margin decline in Q2’23. XPeng reported an almost 9% negative vehicle margin in the second-quarter which was a key reason for me to not recommend the EV firm as a buy anymore: Deteriorating Margin Trend Is A Concern (Rating Downgrade).

Li Auto reported a vehicle margin of 21% in Q2’23 which was by far the highest. Besides stronger than average vehicle margins, Li Auto also presents the strongest gross margin play in the industry group. I believe Li Auto could surprise both in terms of vehicle and gross margins in Q3’23 given the continual surge in deliveries…

The EV firm is also set, in my opinion, to deliver a strong outlook for Q4’23: Li Auto guided for 100,000 to 103,000 electric vehicle deliveries in Q3. The firm ended up delivering, as per the latest update, 105,108 EVs in Q3’23, showing near-300% Y/Y growth. For Q4’23, I estimate that Li Auto could deliver 115,000-120,000 electric vehicles.

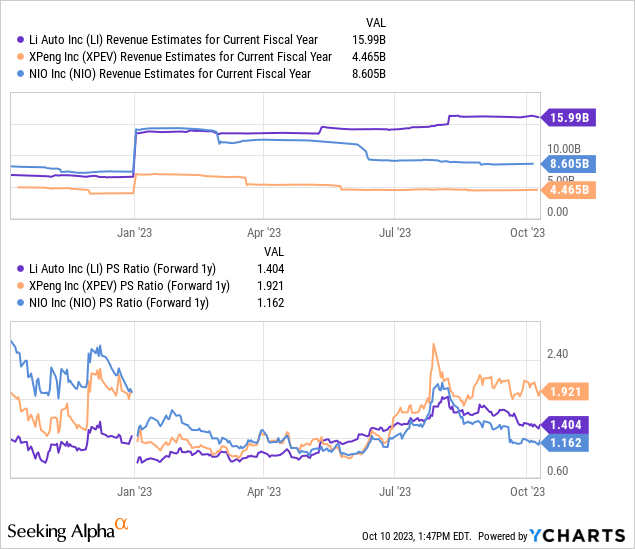

Li Auto’s valuation relative to EV rivals

Li Auto, as ironic as it is, trades at the second-lowest P/S ratio in the industry group despite posting the strongest vehicle margins and the fastest delivery growth. XPeng, which ranks as the bottom, still has the highest P/S ratio. Li Auto is currently valued at 1.4X FY 2024 revenues and the EV maker is expected to generate 53% revenue growth next year. For context, NIO is projected to see a year over year top line growth rate of 57% while XPeng has an estimated revenue growth rate of 71%.

Risks with Li Auto

The biggest risk with Li Auto in the upcoming earnings release is that the company’s vehicle margins, against my expectations, could drop… which would likely add pressure on Li Auto’s valuation factor. However, the odds of this are low, in my opinion, since the firm’s delivery sheets from August and September were exceptionally strong. A monthly delivery forecast of less than 40 thousand EVs in Q4 would be a disappointment to me as well.

Final thoughts

Li Auto is set for a very strong Q3’23 earnings report, in my opinion, that could surprise in a number of ways, especially with regard to vehicle margins as well as run-rate monthly delivery volumes. Li Auto is already expected to generate a full-year profit in FY 2023, but the company is also set to deliver a strong Q3’23 earnings sheet with regard to revenues. With nearly 300% Y/Y delivery growth in the third-quarter and being by far the strongest gross margin play in the industry group, Li Auto is the most compelling bet in the EV market for me this earnings season!