Xsandra/E+ via Getty Images

Kura Sushi USA (NASDAQ:KRUS) operates 47 Japanese restaurants across the United States standing out with a high-tech concept that features digital ordering, service robots, and a conveyor belt sushi bar system.

The story here since the company’s 2019 IPO has been the massive growth momentum as sales more than tripled in the period since. What’s even more impressive is that Kura Sushi has been able to expand aggressively while turning profitable this year. Indeed, the stock has been a big winner, with shares up more than 375% in the past 3 years.

On the other hand, we’re highlighting a more recent round of volatility with shares down nearly 40% since reaching a high of $110 in July following its last quarterly report. While there was a good case to be made that valuation was stretched at the top, we believe this selloff is now overdone. In our view, KRUS remains a high-quality growth name and is well-positioned to rebound.

KRUS Financials Recap

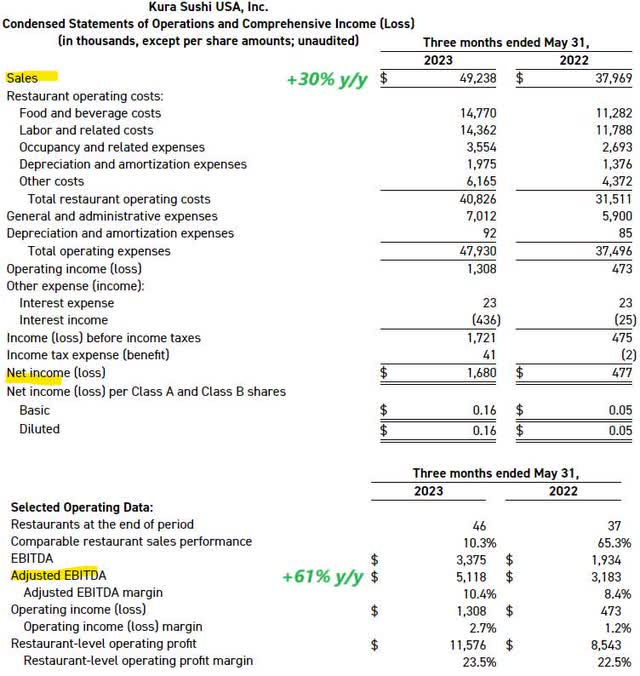

The first point here is that Kura Sushi USA’s headline metrics are fantastic. The company reported Q3 earnings with EPS of $0.16, beating the consensus estimate by $0.12, and up 220% from $0.05 in the period last year. Revenue this quarter at $49.2 million, was up 30% from the period last year.

The strong point has been the comparable sales trend, up 10.3% y/y in Q3, indicative of good brand awareness among returning customers. The company counts on a loyalty program that signed up 120k new members during the quarter.

The result here is that the restaurant-level operating profit at $11.6 million, at a 23.5% margin has widened from $8.5 million last year as 22.5% of sales. Similarly, adjusted EBITDA this quarter at $5.1 million is up 61% y/y.

Management notes that they’ve pushed pricing higher by about 6% from last year on average, although the increases have been more modest sequentially from recent quarters. Lower inflationary pressures have helped on the cost side with an effort made to control general and administrative expenses.

Finally, we can mention that Kura Sushi ended the quarter with $71 million in cash and equivalents against zero debt. There was a secondary offering that raised $55 million in cash during the quarter, but the understanding is that the underlying cash flow trends are sufficient to fund the expansion plans organically.

source: company IR

What’s Next for KRUS?

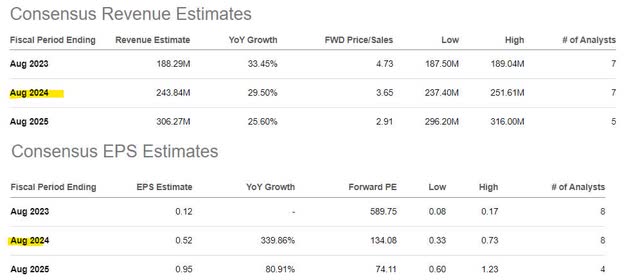

In terms of guidance, the company sees fiscal 2023 sales between $187 and $189 million, representing a 33% increase at the midpoint from 2022. From the 7 new restaurant locations already opened this year, the plan is to reach 9 to 11 by the end of fiscal Q4 covering the period that ended August 31st.

These targets are in line with the current consensus where the market sees 2023 EPS of $0.12. Looking ahead, the expectation for annual top-line growth to be maintained around 30% for the next two years supports an outlook for EPS to accelerate higher in 2024 towards $0.52 and $0.95 by 2025.

These forecasts are aggressive, but otherwise achievable if the pace of new restaurant openings is maintained, coupled with some comparable restaurant sales increases and modestly higher pricing as part of the bullish case for the stock. Simply put, the idea here is that Kura Sushi USA can open a new location that will turn accretive to the bottom line given the favorable unit-level economics.

Seeking Alpha

Is KRUS Overvalued?

So far the operating and financial performance speaks for itself. Everyone loves sushi and it is clear to us that Kura has hit a homerun with its technology-enabled concept that has already proven itself to be replicated across 14 states and Washington DC. The aspect of being company-operated and not relying on franchisees maintains a layer of authenticity and quality control to deliver a consistent “Kura Experience”.

The parallel we can draw here is to Chipotle Mexican Grill, Inc. (CMG), which was able to take its brand of fast-casual/ quick-service southwestern food into the mainstream over the past two decades. While Kura Sushi might not have that same scale just yet, the early trajectory shares some similarities.

source: company IR

That being said, the elephant in the room comes down to valuation. Even with the large share price correction in recent months, KRUS is still trading at a 5x sales multiple and P/E ratio of 589x considering it just turned consistently profitable. That metric narrows down to 134x by next year, which needs to be placed in the context of accelerating earnings and 30% top-line growth.

That poses the risk that if growth simply underperforms or there is some setback in the timetable for new restaurant openings, the stock has a proverbial air pocket to the downside as valuation resets lower.

That being said, when we look at the figures as-is, the argument we make is that KRUS deserves a premium given its profitable growth and brand momentum. The earnings multiple is spicy, but can make sense if we project a continuation of the earnings and unit-level economics over the next several years allowing the financials to sort of catch up.

Going back to Chipotle as a benchmark for restaurant growth stocks, it’s notable that KRUS is currently trading at a discount in terms of its forward sales multiple into 2024 and at a modest spread on an EV to forward EBITDA basis. We’d also consider Wingstop Inc. (WING) as comparable to KRUS which currently trades at an even higher premium.

The point here is to say that KRUS is pricey, but there is some precedence for this current valuation and market cap value around $750 million.

KRUS Price Forecasts

From the stock price chart, we make the case that the selloff in KRUS from its highs has gone too far and shares are now oversold. The current level around $70.00 has returned to some technical support we believe should hold and set up a rebound higher.

We rate KRUS as a buy with a price target for the year ahead at $85.00 representing a 40x multiple on the current consensus 2024 EBITDA level around $22 million. At this level, KRUS converges towards the premium of Wingstop as a high-growth restaurant concept peer.

We mention the risk that growth disappoints or the strategy execution sputters. There is also the consideration that the macro backdrop deteriorates, where a broader consumer spending slowdown undermines the expansion strategy. Over the next few quarters, the key monitoring points here are the adjusted EBITDA margin as well as the comparable restaurant sales.

Seeking Alpha