Brandon Bell

The Kroger Companies (NYSE:KR) is a retail chain with potential for positive earnings and free cash flow momentum related to its digital transformation. Kroger offers investors not only upside in earnings and FCF as the company expands its product offering, store footprint and invests in its digital transformation/online capabilities, but the company’s shares are trading at a truly compelling valuation factor: valued at just 10X FY 2024 earnings, an investment in Kroger implies a 10% earnings yield and the retail chain has guided for positive sales growth in FY 2023 as well. I believe the risk profile is skewed to the upside following Kroger’s consolidation from $50 to $45, and I see 25% revaluation potential!

Kroger is a growing retail chain with a huge opportunity in the digital market

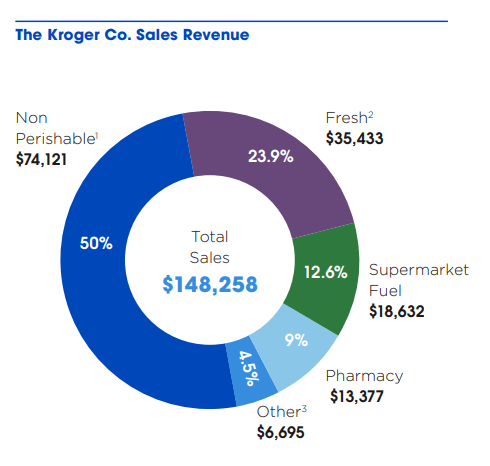

Kroger is a well-known retail chain that provides shoppers with brand groceries, fresh foods, household items, produce, meat and seafood as well as other items. In FY 2022, the company owned 44 distribution centers, 1,637 supermarket fuel centers, 2,252 pharmacies and offered its products in 35 states plus the District of Columbia. The retail company achieved a massive $148.3B in revenues last year… the majority of which was achieved in the non-perishable category, followed by fresh produce sales.

Source: Kroger

With more and more transactions being conducted online, I believe Kroger has a huge opportunity to grow its digital sales business going forward. In the first-quarter alone, digital revenues were up 15% year over year, and they were up 12% year over year in the second-quarter as the company’s investments into its digital transformation is paying off. Sales from Kroger’s digital channel already exceed $10B and are set to grow much stronger than Kroger’s consolidated top line. According to long term revenue projections (provided by Seeking Alpha), Kroger, like most retail chains, is expected to see top line growth in the low single digits going forward, but new online channels offer the opportunity for faster channel growth.

Strong guidance for FY 2023, strong capital return potential

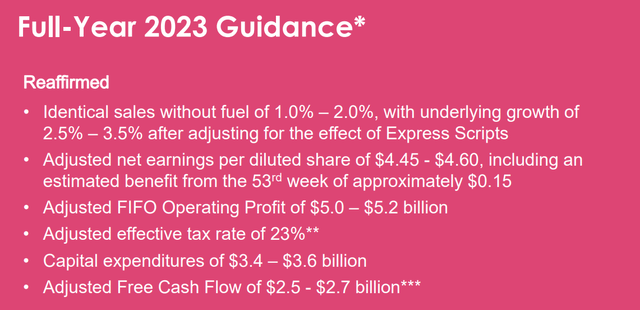

Retail is a tough business, with retailers’ business models typically evolving around a high-volume, low-margin strategy. However, Kroger has guided for earnings growth as well as positive adjusted free cash flow for FY 2023 which implies attractive potential for incremental capital returns. Kroger has guided for 1-2% positive sales growth on a same-store basis and, importantly, adjusted free cash flow of between $2.5B and $2.7B in the current fiscal year.

Source: Kroger

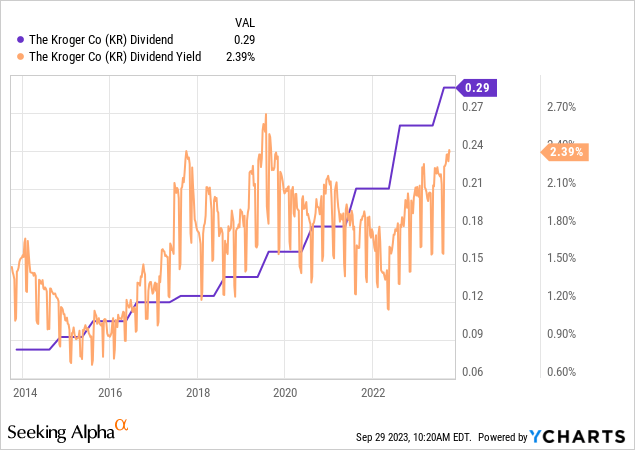

This free cash flow creates optionality for Kroger and its investors, as the company could decide to return a considerable percentage of this free cash flow to shareholders going forward. Kroger already pays a growing dividend to shareholders and the company has guided for 8-11% annual shareholder returns consisting of 3-5% net earnings growth (through organic growth, digital transformation effects and an expansion of its store footprint) and 5-6% additional growth coming from dividend payments and stock buybacks. In September, Kroger raised its dividend by a massive 11.5% to $0.29 per-share. The dividend has grown rapidly over the last decade, which makes the shares of Kroger especially attractive to dividend investors.

Kroger/Albertsons merger deal

Kroger agreed to acquire rival grocery chain Albertsons Companies (ACI) for $24.7B in the fourth-quarter of FY 2022. The deal was strategically intriguing because the combination of the second and fourth-largest grocery chains would have allowed them to challenge industry-leader Walmart (WMT) and create synergy potential. However, the deal is seeing regulatory headwinds as the Federal Trade Commission is said to challenge the merger deal on anti-trust grounds.

Kroger and Albertsons have agreed to sell more than 400 of their stores to C&S Wholesale Grocers in a bid to get regulators to approve the deal. If the deal falls through, Kroger’s valuation may be set to experience some valuation pressure in the short term. Given that the company is free cash flow-positive and has potential in the digital market, my investment choice with regards to Kroger would not change in case the merger with Albertsons didn’t happen.

Valuation of Kroger: double-digit earnings yield

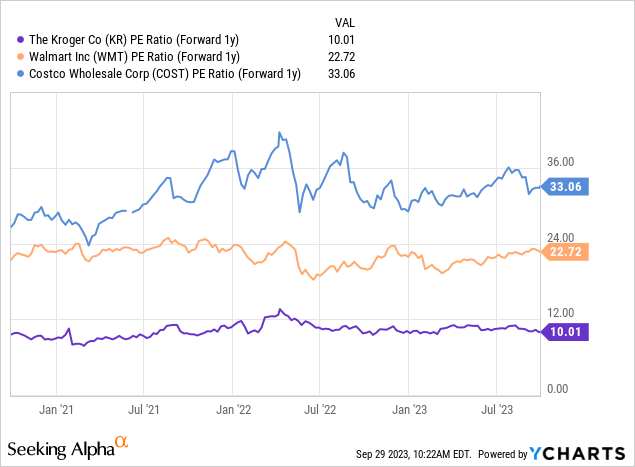

Besides a positive outlook for net earnings growth and the opportunity in the digital space, I believe the most compelling factor of Kroger’s value proposition relates to its cheap valuation. Shares of Kroger trade at only 10X forward earnings, which implies a 10% earnings yield going forward. The company is also, like I said, paying a decent dividend and could be buying back more shares going forward as well… which of course makes a lot of sense as long as the valuation is as low as it is now. Compared against other retail companies, Kroger also has a valuation advantage, since larger scale retailers like Walmart (WMT) and Costco (COST) trade at considerably higher earnings-based valuation factors.

I believe Kroger, in the longer term, could be valued at 12-13X forward earnings which implies, based off of FY 2024 estimated earnings of $4.47 per-share, a potential fair value range of $54-$58. At a midpoint of $56, shares could have 25% upside potential.

Risks with Kroger

The retail business is notoriously competitive and margins are low, which I consider to be the biggest risk not just for Kroger but for all retail companies that operate a large number of retail stores. The second-biggest commercial risk that I see for Kroger is that the company’s digital revenue growth may slow, which could weigh on the company’s valuation factor.

Final thoughts

Kroger is a well-known retail brand in the United States and the company has submitted a robust financial forecast for FY 2023 that includes positive top line growth as well as at least $2.5B in (adjusted) free cash flow… which could result in a nice sum of cash being spent on stock buybacks going forward. The company also just raised the dividend for shareholders, by a whopping 11.5%. I like Kroger’s opportunity in the digital sector as well as the company’s low valuation based off of P/E which translates into a double-digit earnings yield for shareholders. Considering that shares have recently consolidated from $50 to $45, I believe the risk profile is skewed to the upside, especially for those investors that want to buy a cheap retail company that generates double-digit dividend growth for investors!