Feverpitched

Dear readers,

Granite Point Mortgage Trust (NYSE:GPMT) is a relatively small mortgage REIT with a loan book of just above $3 Billion. I’ve been covering the stock here on Seeking Alpha for a while. After my initial analysis in February I issued a SELL rating at $6.06 per share, because I concluded that there was a high risk of a dividend cut, then after Q1 earnings things improved a bit and I upgraded the stock to a BUY at $4.40 per share. Having examined Q2 earnings and in light of the increased risk of a higher for longer scenario, I now want to publish an update and explain why I’ve exited my position with no plans to re-enter.

What is the problem?

To quickly recap, Granite Point’s main issue is that a large portion (40%+) of their loans outstanding are offices. To make matters worse, some of them are relative old and struggle with high vacancies. I think by now everyone is familiar with the reasons why offices aren’t necessarily the best asset to own at this time. From Granite Point’s perspective, the problem is that as interest rates increase and these increases translate into higher interest payments on their floating rate portfolio, there’s a real risk that some borrowers will default on their loan and hand over the keys to the property. Normally, a creditor has enough of a buffer and can recover the loan amount by selling the property, but in case of distressed offices, it may prove difficult to do so and the mREIT may suffer losses.

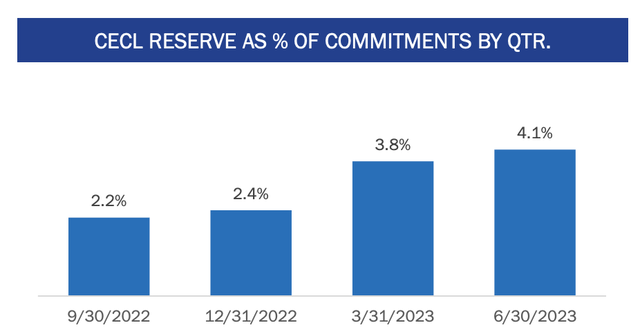

Reserves, defaults, write-offs

Management has been getting ready for a wave of defaults by increasing their CECL reserve significantly over the past year. As of today, the reserve stands at 4.1% of the whole portfolio (about $135 Million or $2.50 per share). Half of the reserve is designated specifically for four 5-rated loans with an aggregate principal balance of $245 Million, implying an estimated (expected) loss rate on these loans of 25%. Since these four loans we all issued between 2017 and 2019 and had origination LTV of 65-75%, the CECL reserve will be sufficient if the mREIT can sell the foreclosed properties for 50% of the value at underwriting. Having researched a number of office REITs I think this is quite realistic as roughly speaking office values were cut in half since pre-pandemic.

GPMT Presentation

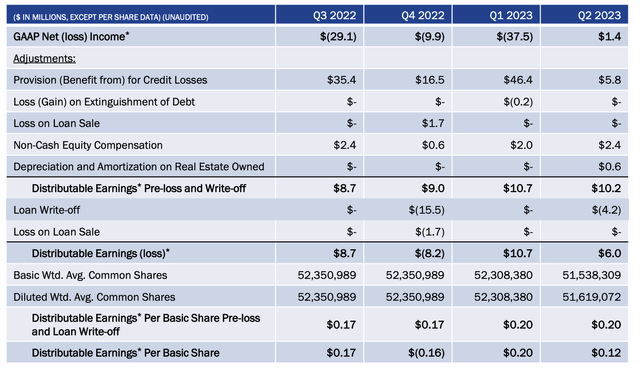

Granite Point had to deal with the first major write-off in Q4 2022 when it took a $15.5 Million loss on a $114 Million office loan (5-rated at the time). During Q2 2023, another 5-rated loan office defaulted. This time a $29 Million loan on a property in Phoenix. The foreclosure resulted in an immediate write-off of $4.2 Million. Going forward, I think it’s quite possible that more loans will default, especially if interest rates remain high.

Dividend NOT covered at all

Looking at the last four quarters, GPMT has averaged distributable earnings of just $8.25 per quarter. Note that distributable earnings are before provisions for credit losses (i.e. the CECL reserve), so really excluding any of the bad stuff that could happen. Still, over the last 12 months, the company hasn’t made nearly enough to cover the $0.20 quarterly dividend. A last 12 month payout ratio of 242% says it all.

GPMT Presentation

My worry is that the mREIT keeps paying out a 17% annual dividend (which has been confirmed for Q3) when they’re clearly not generating enough cash to cover the dividend. Not even excluding the CECL reserve. They should preserve their liquidity in anticipation of defaults. Last quarter, things seemed to have improved somewhat, but in Q2 the mREIT went right back to where it was. I don’t see this as sustainable and see a dividend cut as very likely over the next 12 months.

Valuation is interesting, but …

I encourage everyone to see my detailed calculations in my last article, but in short, the appeal here is that the stock trades at a major discount to book value which implies a default of 30-40% of loans in the portfolio. In other words, the market has essentially written-off the entire office loan portfolio.

Of course, this is interesting from a pure value perspective. I don’t think Granite Point is at risk of going bankrupt at this point and if you don’t mind high volatility, there is probably some upside here when the credit cycle turns.

But the issue is that if the company experiences a couple more defaults (which is very possible) and consequently has to cut the dividend, we will likely get an opportunity to enter at an even lower price. Moreover, while my base case remains that interest rates will decrease over the next 12-18 months, I want to be prepared for a higher for longer scenario, which assumes sticky inflation.

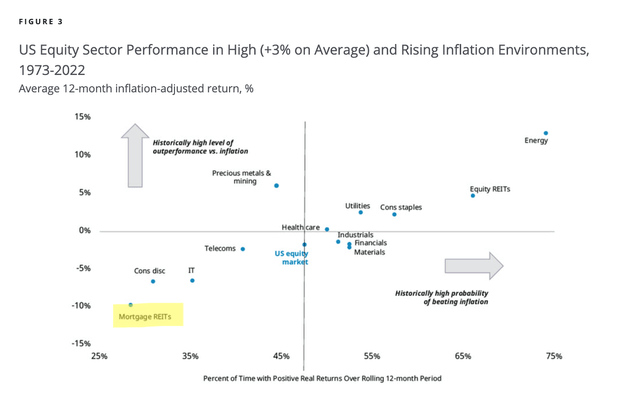

Studies have shown that mortgage REITs are the worst sector to own in a high inflation environment as they underperform 75% of the time with an average 12-month return of -10%.

Hartford Funds

For these reasons, I rate the stock a SELL and have no intention of re-entering any time soon. I will reconsider after they cut the dividend and/or after interest rates decrease.