Justin Sullivan/Getty Images News

Investment Thesis

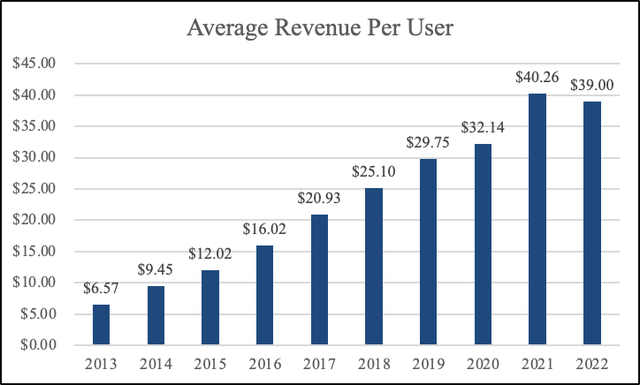

Meta Platforms (NASDAQ:META) is a main beneficiary of what people are calling the new oil. Data is the most valuable thing to advertisers. With it, they know what audiences to target. Without it, it’s a hit or miss. Facebook (Meta’s app) is the largest social media in the world, with nearly 3 billion active monthly users. Meta’s large user base allows it to generate valuable data which advertisers find useful. Meta’s average revenue per user as of the latest quarter stood at 10.60, which is almost five times more than SNAP’s. This figure has increased through the years, demonstrating the company’s pricing power and the continued value it provides to advertisers.

Created by the author

You can’t talk about Meta without talking about Mark Zuckerberg. A bet on Meta is essentially a bet on Mr. Zuckerberg. He owns 13% of Meta and has more than 57% voting power. Although some are skeptical of the recent investments he has made in the metaverse, I believe, given Mr. Zuckerberg’s experience, he wouldn’t invest more than $30 billion if he didn’t believe in the project. Plus, most of his wealth is tied to the company, which should provide investors with confidence.

Meta still has more room for growth as the shift towards online advertising continues. The company’s family of apps has leading positions in Android and iPhones. Facebook has an 18% market share in digital ad revenue. The industry is expected to grow at a CAGR of 7.57% until 2027, driven by continued smartphone penetration. As a leading online advertiser, I expect Meta to benefit from this growth. Meta has a solid balance sheet with strong liquidity (current ratio of 2.3) and very little leverage.

Personally, I like management teams that are always on their toes, keeping up with trends and competition in order to evolve and improve. Meta recently came up with great products that will boost their top line, such as subscriptions for the blue checkmark, the VR product, and the Thread app. What these things have in common is that they increase user engagement, thus providing more value to advertisers. Additionally, Meta’s ownership of multiple social media apps makes it hard for advertisers to switch and find similar value at a different company.

Upcoming Earnings

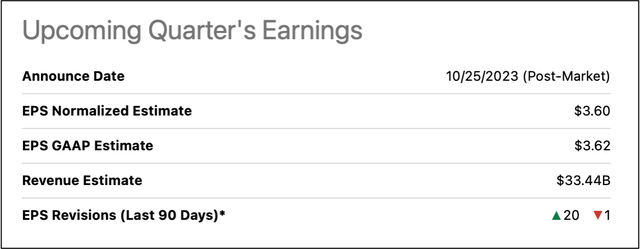

Meta is set to report third-quarter earnings on October 25th after market close. Consensus estimates are $3.60 EPS and revenue of $33.4 billion, implying a 95% and 21% increase year-over-year. Meta has crushed earnings for the last two quarters, beating EPS, Users, and Revenue expectations. I believe momentum is in the company’s favor, especially with new sources of revenue, such as the blue checkmark, the VR product, and the Thread app. Additionally, margins have been improving quarter by quarter, providing investors with more confidence. I believe the company is on the right track, but if they miss earnings and stock dips, that might offer investors the chance to buy a great compounder at a cheap price.

Seeking Alpha

Valuation

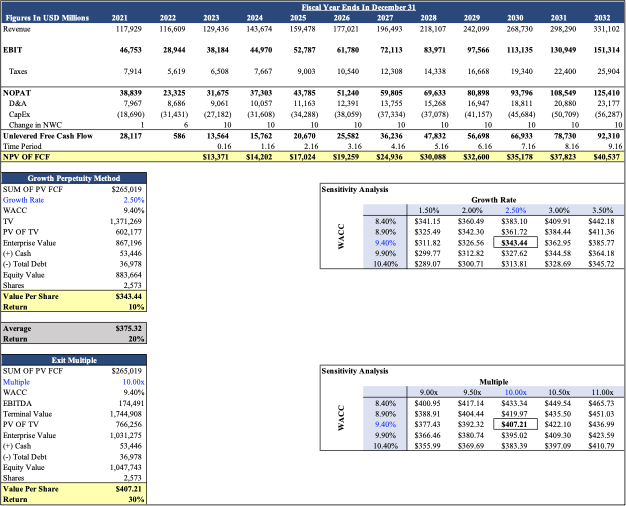

As I’m writing this, the stock is sitting at $313. META is trading at a forward PE of 23.64x the FY23 consensus of $13.31 and 19.10x the FY2024 consensus of $16.48. On a trailing free cash flow basis, the stock yields over 2.33% relative to its enterprise value. I used the discounted cash flow method to value META.

My base scenario includes total revenue growing by 11% from 2023–2032, driven by a continued shift to online advertising, price increases, and new products. I have gross margin expanding by 28 bps annually from the current margin of 79.45%. I used a WACC of 9.40%, a growth rate of 2.50% (lower than GDP growth rate), and a multiple of 10.00x (discount to TTM and FWD).

Other assumptions include a 13% marketing and sales margin, 9% for G&A, and 22.50% for R&D. M&S and G&A Margins are based on historic figures, however I estimate R&D spending to stay elevated in the next two years as the company continues pouring cash into the meta verse before slowly normalizing spending. Using these assumptions, I arrived at a value per share of $343 per share for the growth perpetuity method and $407 for the exit multiple method. Taking the average of both methods, I arrived at a value per share of $375, translating into a 20% return from the price of this writing.

Created by the author

My downside scenario includes total revenue growing 10% from 2023–2032, driven by a slower shift to online advertising and less frequent price increases. I assumed the gross margin would expand by 22 bps annually from the current margin of 79.45%. I used a WACC of 9.40%, a growth rate of 2.30% (lower than the GDP rate), and a multiple of 9.00x (discount to TTM and FWD).

Other assumptions include a 13.50% margin on marketing and sales, 9.50% for G&A, and 23.50% for R&D. I took the same approach as I did for my base case scenario. The only difference is that operating expenses will be at a higher rate, and R&D spending will take longer to get back to historical figures. Using these assumptions, I arrived at a value per share of $273 per share for the growth perpetuity method and $322 for the multiple methods. Taking the average of both methods, I arrived at a value per share of $298, translating into a 5% downside from the current price.

Mitigates

I believe a major risk associated with Meta is regulation. If new laws come into play that restrict the amount of data companies can collect, then Meta won’t be able to provide as much value to advertisers because, at the end of the day, advertisers choose Meta because of its large database. Competition is another concern. In the social media space, we have seen time and time again that a new platform comes into play that can easily lure users away from dominant apps such as Facebook. So far, Meta has done a great job at evolving and improving its apps to keep up with change, but one has to keep an eye out.

Conclusion

To sum it all up, Meta is a founder-led company that has been a great compounder over the years. The stock was very cheap last time this year—cudos to those who bought in at that time. I believe the shift to online advertising still has room for growth, underpinned by continued smartphone penetration. A big chunk of Mr. Zuckerberg’s wealth is tied to the company, which means his views are aligned with those of the shareholders. My valuation implies a value per share of $375, translating to a 20% upside