DeFi lending protocol Edel revealed a $403,000 exploit that hit the layer where tokenized shares attempt to become DeFi collateral.

Edel said that no depositors would bear losses, and that the team would absorb the bad debts, restore affected balances on a one-to-one basis, and rebuild the protocol’s oracle architecture for a version two release.

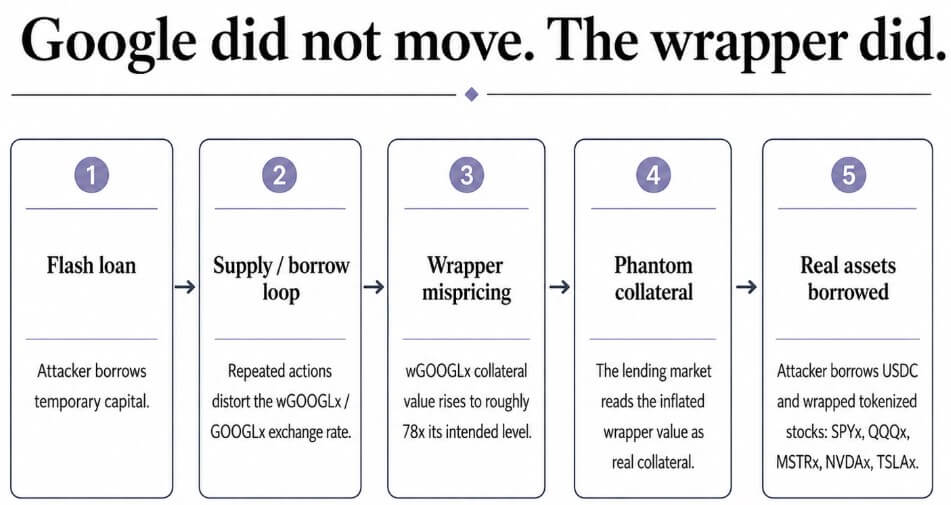

The attack manipulated the exchange rate between wGOOGLx, a packaged version of Edel’s tokenized Google stock, and GOOGLx, the token inside. Edel said the manipulation pushed wGOOGLx’s collateral value to about 78 times the appropriate level.

SlowMist traced the root cause to Edel’s pricing source, which used newestAnswer() to return the convertToAssets() rate of an ERC-4626 style vault. That conversion rate can be manipulated when an attacker controls enough of the underlying flow, and Edel’s price feed reads it directly.

CertiK described the same flaw on the credit side: the attacker manipulated the collateral price of wGOOGLx, which tracked the GOOGLx balance, and then borrowed against the inflated value.

GoPlus noticed that the attacker used a flash loan to deliver and borrow repeatedly, disrupting the wGOOGLx/GOOGLx conversion ratio. The inflated collateral then supported real borrowed assets, including 384,215 USDC and rounded positions in SPYx, QQQx, MSTRx, NVDAx and TSLAx.

Security companies published different estimates. Cyvers estimated the loss at about $353,000, GoPlus cited about $403,000 in losses and about $305,000 in profits for the attacker, and CertiK estimated the money taken at about $204,000.

The difference appears to reflect several measurements, including bad debt, gross loss, and attacker net profit.

The disconnect is likely because each company measures something different, such as bad debt, gross loss, or net profit.

The critical failure was in the exchange rate between the wrapped token and its underlying counterpart, a relationship that Edel borrowed market priced as if it were stable. Alphabet’s stock price was not the driving force behind the exploit.

The market in figures

RWA.xyz estimates the onchain value of tokenized stocks at $1.7 billion, up 2.17% in the past 30 days. The monthly transfer volume is $8.92 billion and the number of holders is over 396,000.

xStocks alone contains more than 100 stocks and ETFs across more than 50 integrated platforms, with a total transaction volume of more than $25 billion. It describes itself as fully supported and open to connecting to any DeFi protocol without permission.

Backed, the publisher behind xStocks, is explicitly marketing the tokens for DeFi use: lending out tokenized Apple shares or borrowing them without selling.

Kamino says it has become the first major lending protocol to accept tokenized equity as collateral, allowing users to deposit tokens such as SPYx, QQQx, GOOGLx, AAPLx, NVDAx, TSLAx, MSTRx and HOODx to borrow stablecoins or earn returns.

Robinhood launched stock and ETF tokens for EU customers in June 2025 and then opened a public testnet for Robinhood Chain. The network is an Ethereum layer-2 built on Arbitrum, designed around tokenized real-world assets including stocks, ETFs and private assets.

The selling point in all of this is the same: tokenized stocks should move and connect like any other crypto asset. Edel reminds us that once they move like crypto, they can also break like crypto.

The gap between support and security

A credit market prices different layers, such as the tokenized equity itself, the packaged version built on top of it, and the exchange rate a vault uses to convert between the two.

It also touts the oracle path that reports a value, the credit market’s own borrowing limits, and whether that collateral can actually be sold during a period of stress. Edel’s exploit was almost entirely in the wrapper and oracle layers.

Using a tokenized stock as collateral adds a second pricing problem on top of the equity itself. A protocol must also determine a price for each on-chain representation built around that stock, including how a wrapper’s exchange rate behaves under stress. That exposure comes from the integration of collateral built around a tokenized share.

Flash lending, collateral manipulation, and ERC-4626 exchange rate attacks have all cropped up in DeFi exploits before. The novelty of this exploit lies in the asset class these techniques target, and it appears to be one of the first clear exploits based on tokenized stock collateral.

How this works out

In the case of a bull, the protocols are working on isolating the wrapper risk over the next year. That means capping the amount of collateral in a credit market that can come from wrapped tokenized shares, separating issuer-level prices from wrapper exchange rates, and building oracle paths that can’t be moved by a single flash loan.

Tokenized shares then become credible collateral for conservative lending against liquid names like Apple, Nvidia, Tesla and Google. Edel is ultimately remembered as the early failure that forced better design before the category scaled up.

In the bear scenario, quotes trump risk work. More and more venues are accepting tokenized shares as collateral before oracle design and wrapper insulation catch up.

The number of wrapped tokens, bridges, and vaults built around each ticker continues to multiply faster than anyone can control them.

Along that path, more and more exploits continue to surface in the low hundreds of thousands of dollars, involving exchange rate manipulation and limited liquidity. Tokenized stocks have become a security concern over how DeFi protocols use them as collateral.

The first phase of tokenized shares was access: giving eligible users tokenized exposure to names like Apple or Google. The second phase was trading, which required moving that claim through chains around the clock.

Edel came at the beginning of the third phase, the collateral, where holding a tokenized share also makes it possible to borrow against it.

The first two phases of tokenized shares rewarded whoever recorded the most tickers or reached the most chains. The next one every time rewards whoever can correctly price a packaged stock under stress.