murat4art

Investment Rundown

Hexcel Corporation (NYSE:HXL) is priced like a growth company right now I think seeing as the p/e is at over 30 which may still be below the 5-year average for the company of 36. The factor of the matter is that HXL is a premium-valued business that isn’t necessarily delivering the growth numbers to justify the price currently. On October 23 we got the last earnings report from the comment and I don’t think it’s the result I would equate to a company valued at these prices. The sales grew by 15% YoY, reaching $420 million. With a sales multiple 124% higher than the industrial sector I think it’s not sufficient growth numbers right now. I would be looking for over 20% at least for the company to be an appealing buy right now.

What has to be said though is that revenue has been consistently increasing following the quick drop caused by the pandemic. Air travel is on the rise again and that is a significant tailwind for HXL of course.

My reasoning behind the hold comes down to the lack of value I get from buying right now. The price will have to stagnate for a significant amount of time for the earnings to catch up to what I think is a reasonable valuation. The company does pay a dividend but has been diluting shares since 2020 and that doesn’t help any buy case out there.

Company Segments

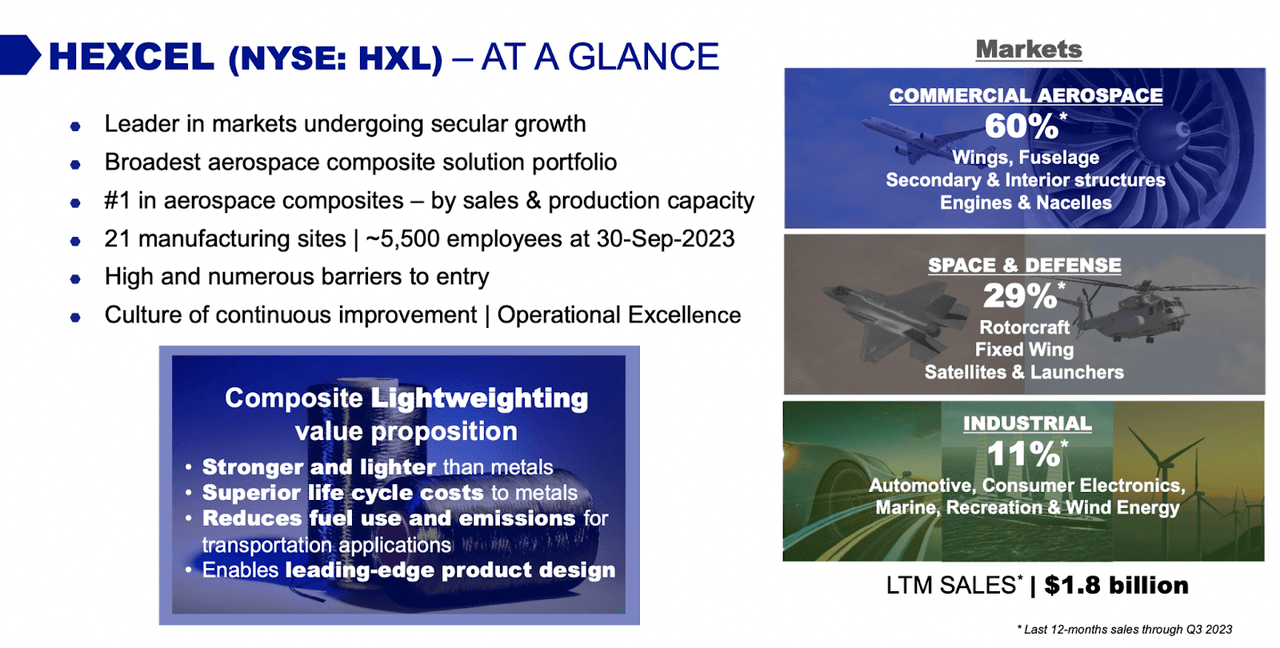

HXL is a key supplier of structural materials to the largest players in the aircraft manufacturing industry, namely Boeing (BA) and Airbus (OTCPK:EADSF). Impressively, over half of HXL’s net sales, a significant 52%, are attributed to these two aviation giants, emphasizing their crucial position within the aerospace sector.

Investor Presentation

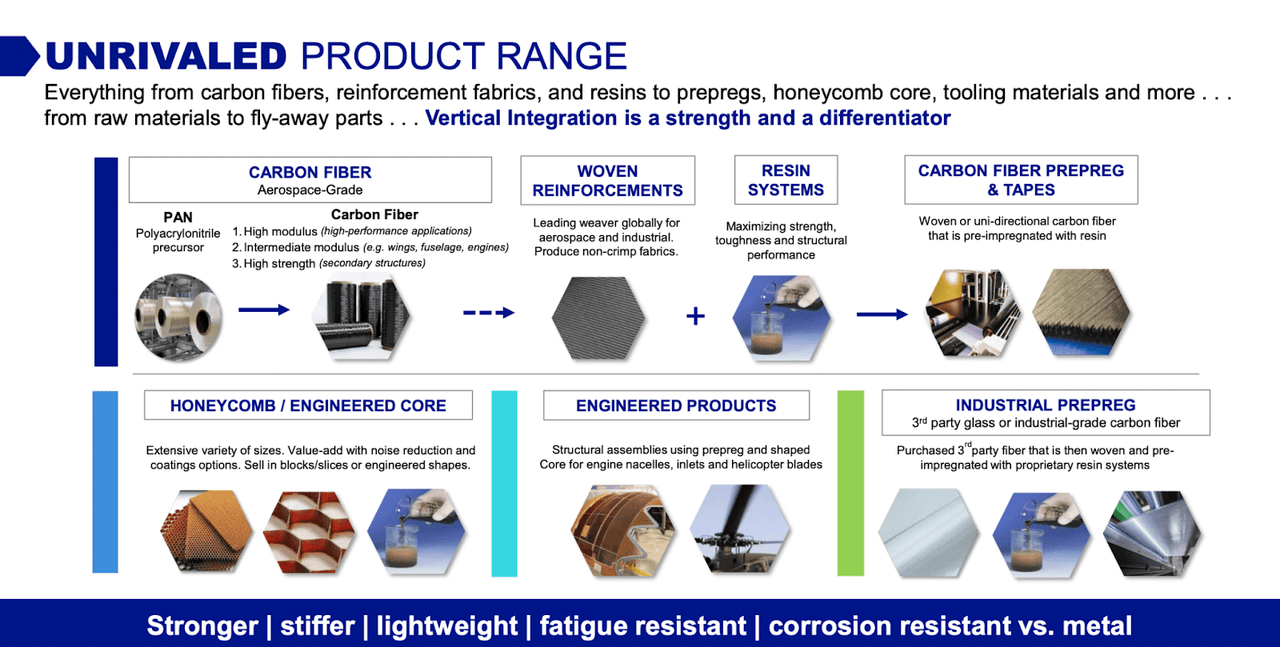

In terms of its revenue streams, commercial aerospace stands out as a major driver, accounting for a substantial 58% of the company’s total sales. HXL specializes in the development, manufacturing, and marketing of an extensive range of aerospace materials, including carbon fibers, structural reinforcements, honeycomb structures, resins, as well as composite materials and components. These cutting-edge materials find application not only in the commercial aerospace sector but also extend their influence to space and defense industries, as well as various industrial applications.

Investor Presentation

HXL is organized into two distinct segments: Composite Materials and Engineered Products. This segmentation reflects the company’s commitment to delivering specialized solutions to meet the demanding requirements of the aerospace and industrial markets, solidifying its role as an influential player in these critical sectors.

Seeking Alpha

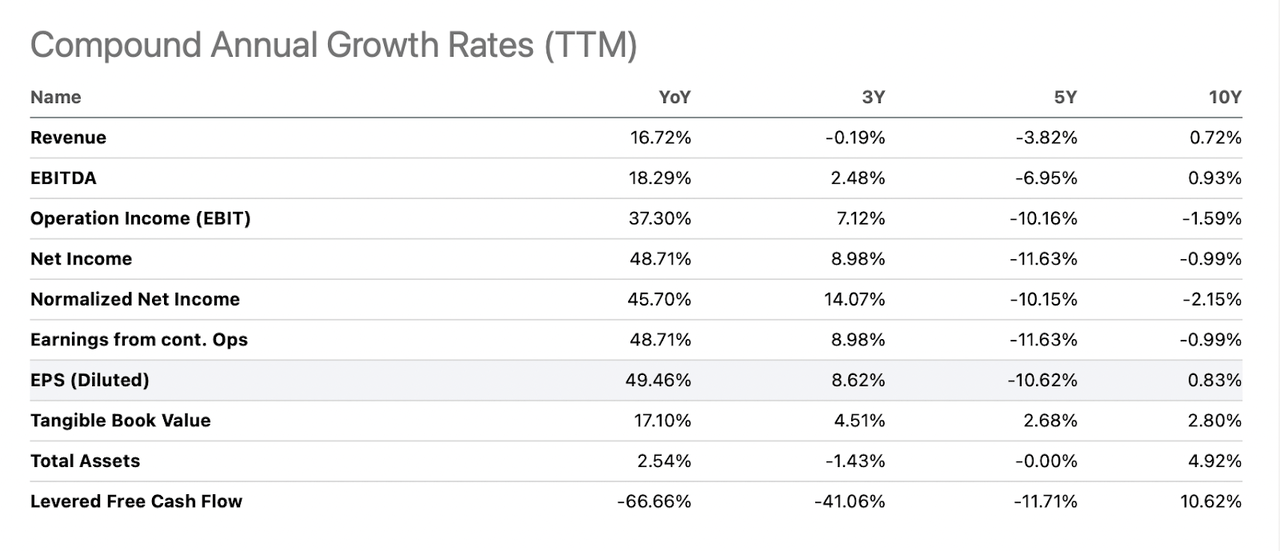

The solid customer base the company has amassed consists of some of the largest aircraft and travel companies has resulted in sticky revenues but not necessarily strong growth numbers. With just 0.72% CAGR for the revenues over the last 10 years, I don’t see how HXL could ever justify the current multiples it’s receiving.

Earnings Highlights

Investor Presentation

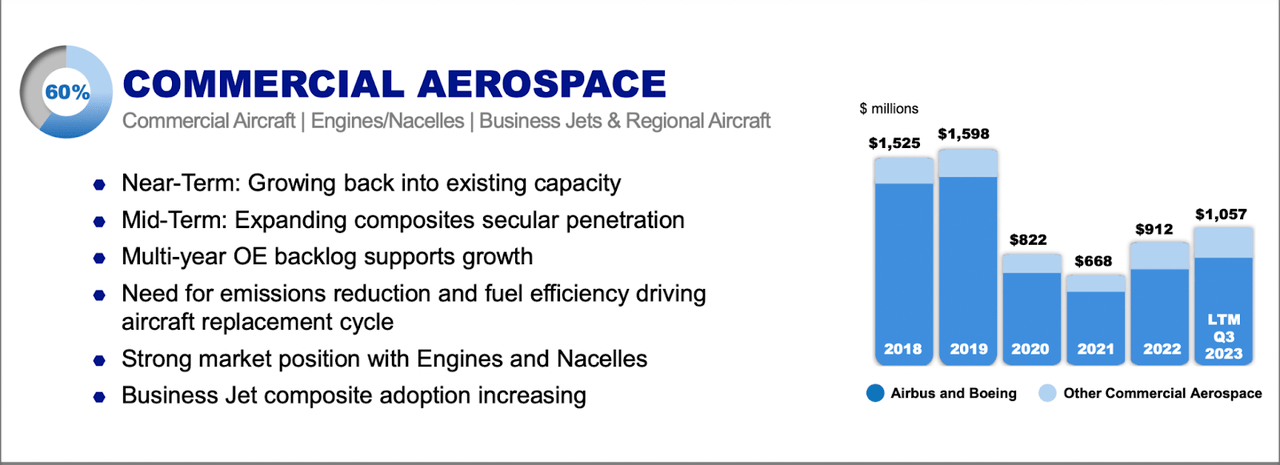

Investing into companies exposed to travel trends is right now based a lot on the industry rebounding to pre-pandemic levels and HXL is a bet on just that right now. The revenues in 2019 amounted to $1.5 billion in the commercial aerospace segment or $2.3 billion for the entire business. In the last 12 months, the company has netted $1.7 billion in total which leaves around 35% more in top-line revenues left to be filled for a complete recovery. Should the bottom line see the same 35% increase then HXL is at $2.53 and with a reasonable p/e of 16 we get a price target of $40.

Investor Presentation

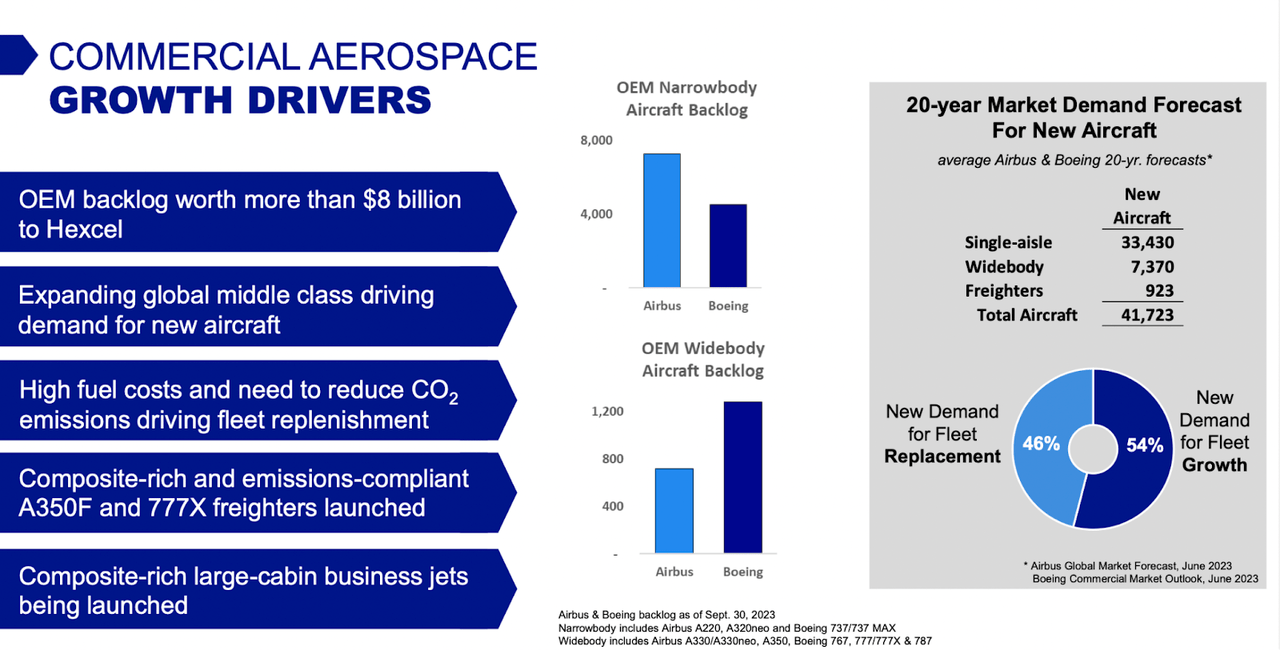

The market demand is still vital for the business and this should be a key driver for the recovery eventually coming true. Right now HXL has also managed to gather up over $8 billion in OEM backlogs. The 20-year forecast demand for new aircraft is around 41 000 accounting for both Airbus and Boeing. Most of that is coming from Boeing as well.

Returning to the price targets I had mentioned before. If HXL sees a full recovery we could expect a realistic share price of $40. Between 2019 and 2013 HXL saw its bottom line expand by 63% in total, or an average of 10.5% YoY. For the sake of it, let’s say that HXL sees a full recovery by 2025 and has an EPS of $3.61 which was the result in 2019. That puts a price target of $57 for the company. With a 10.5% growth rate by 2030, the EPS would be $5.94 and a 16x earnings multiple gives a price target of $95, a 61% upside from today’s levels. Over 7 years that is an 8.7% CAGR. What still keeps me from rating it a buy is the fact that elevated interest rates could limit the company’s ability to fund the expansions and projects to boost production levels. HXL still has a substantial amount of debt at nearly $800 million which will be a burden for them going forward. I think a more realistic CAGR between now and 2030 is around 6% for the EPS which isn’t sufficient for the company to be a buy right now. To get what I would prefer, which is a 12% CAGR between now and 2030 we need an entry point of around $37 which of course is a fair bit below today’s prices and a reason for my hold.

Risks

HXL faces robust competition from companies of comparable sizes, both domestically within the United States and on the global stage. The landscape of this market is characterized by intense competitiveness, with numerous manufacturers offering products with similar applications in their respective portfolios. The industry conditions often favor new entrants, making it imperative for HXL to remain at the forefront of innovation and product development. Should HXL lose some of the partnerships it has with either Boeing or Airbus I think the revenues are in deep trouble. It seems that the partnership is ongoing as in 2021 HXL managed to sign a long-term contract as a supplier of some products and goods for the Boeing 777x family.

Macrotrends

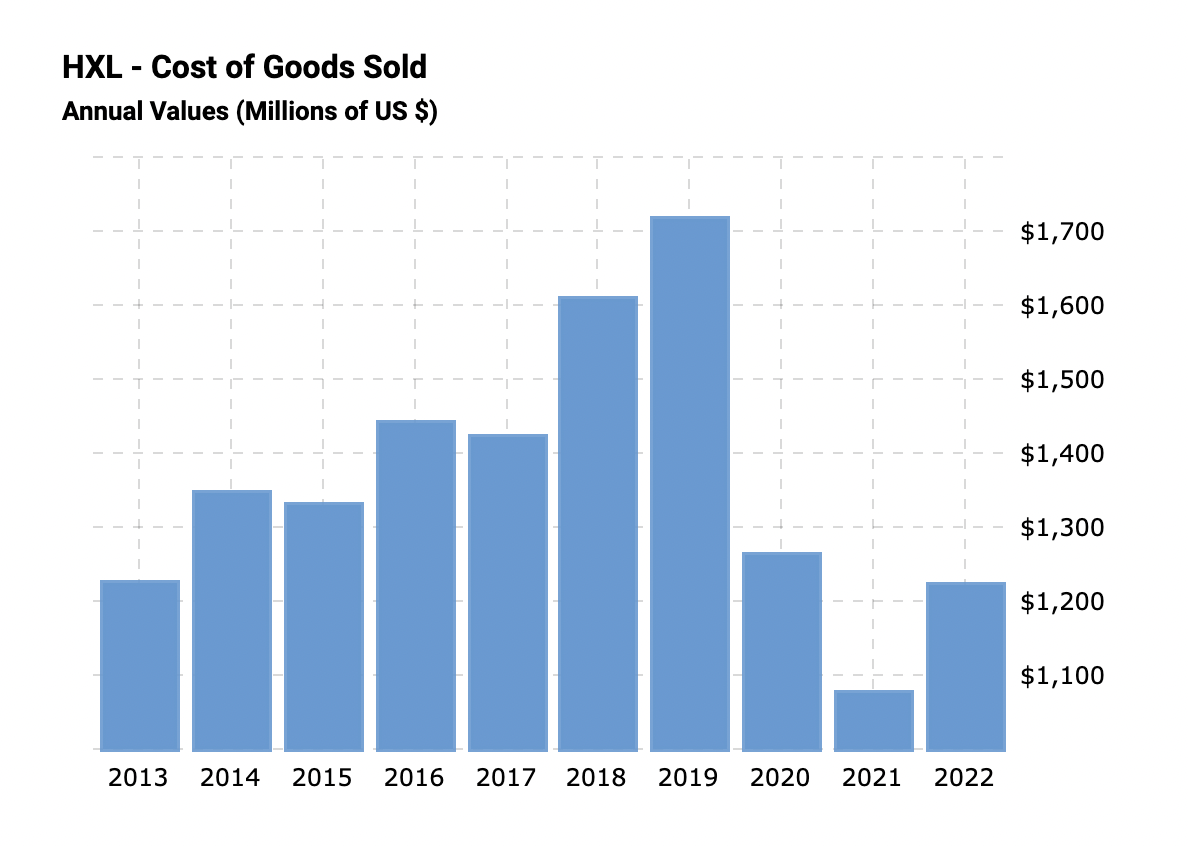

The rising cost of goods could also be a cause for concern. Should the margins not expand rapidly following top-line recovery then the outlook for potential investment returns be muted and result in the share price falling. rising material costs and higher interest rates will make it more difficult for the company to be expanding rapidly.

Final Words

HXL is a recovery story playing on how aviation and air travel will return to pre-pandemic levels. I am a little bit skeptical of this and won’t be rating the company a buy. It is still trading quite a bit above where I would be comfortable buying and because of this, I think it’s more reasonable that HXL is rated as a hold until we potentially see those entry points.