Frank Peters

Introduction

FTAI Aviation (FTAI) is the result of a spin-off between it and FTAI Infrastructure (FIP) which occurred in August 2022. Post spin it is a Cayman Islands exempted company which will no longer be subject to Schedule K-1 reporting. Shareholders who held shares in 2022 prior to the spin however should have received a final K-1 in 2023. Due to its mid-cap nature ($3.4 billion market cap) and approximately one-year lifespan as a separate company, FTAI was relatively underfollowed by the market. However, it is being discovered and its prospects are apparently becoming better thought of as the company’s common stock is up >120% over the last year.

NASDAQ:FTAIP is one of a number of preferred issues of FTAI including FTAIO, FTAIN and FTAIM. It is an 8.25% cumulative fixed-to-floating preferred issue currently trading at $22.82 for a 9.1% simple yield. This preferred however becomes floating in September of next year at what would be a much higher rate. Thus, it appears too cheap relative to FTAI’s other preferred. For example, FTAIP would need to trade at around $24.50 to produce about the same return as recently issued FTAIM.

More importantly, FTAIP is likely to be called. The preferred will switch to floating at 3-month Libor + 6.88% in September 2024. At about 12.5% for current Libor, this is a very unattractive rate for the firm relative to other preferred and debt. Rather than letting that occur the firm is likely to call FTAIP which would produce a 18% return to first call for current investors. We believe this is an attractive return verse the risk investors are taking on.

Why Management will want to call FTAIP in September 2024:

If FTAIP were allowed to switch to floating at 3-month Libor + 6.88%, the firm would have to pay approximately a 12.5% yield at current rates. However, FTAI has been able to recently issue new preferred at 9.5% fixed (FTAIM) potentially saving FTAI 3% in interest by refinancing FTAIP into new preferred. Alternately, FTAI debt is currently rated BB- by Fitch. While not investment grade, borrowing for other similar BB- debt is currently available at about 8%. This implies FTAI would save >4% by refinancing this preferred into debt instead of letting it switch to floating. Finally, management has been using excess cash flow to buy back discounted debt in the recent past ($200 million worth of discounted 2025 debt was bought in 2022). Hence there is a lot of incentive for management to refinance this preferred rather than to let it float, and a number of potential different alternatives for them to do so.

Why Management has a decent opportunity to refinance or pay off this preferred:

As stated, similar debt to FTAI’s BB- has been refinanced at 8% recently. Also, the firm itself was able to issue new preferred FTAIM at 9%. Both imply the debt and preferred market remain open to the firm. Furthermore, the firm has been producing a decent amount of cash flow from both ongoing operations and asset sales. Finally, FTAIP’s debt schedule is reasonably spaced, and its coverage is good.

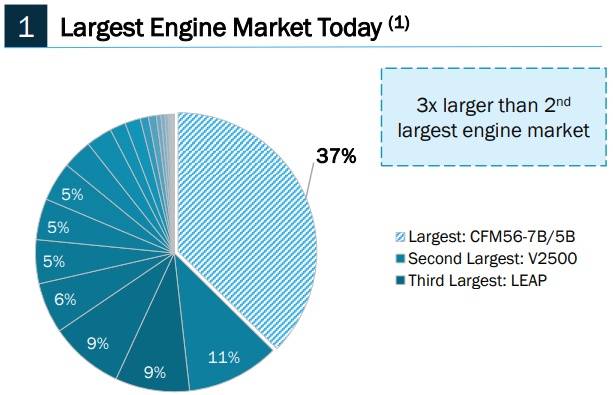

Fitch likely rates FTAI below investment grade (BB-) due primarily to its high debt load, a whopping 83% of FTAI’s book assets (CFM56 plane engines and airframes). However, these assets are of high quality, in high demand and very likely undervalued. As most will be aware, airlines have been doing very well post Covid. Their problem is not having enough usable airframes and crews, not too many. Furthermore, FTAI leases exclusively CFM56 engines and airframes to these airlines. These engines are not only the most popular aircraft engine in the world, but they are also expected to have useful lives through 2045.

Company Presentation

Sales of these “used” assets further support the notion they are more valuable than what is reported under GAAP accounting rules. In 2022, FTAI’s aviation leasing segment showed a substantial net profit from asset sales. They received $208 million in asset sales revenue, but the cost of these assets on the books was only $159 million. This is more than a 30% premium to book value, strongly suggesting GAAP reporting undervalues FTAI’s assets. Fitch can’t give a firm credit for this implied value, but we can. I estimate true debt to assets is approximately 58%; much lower than the 83% implied by standard GAAP required balance sheet depreciation. This occurs because GAAP depreciation on these assets tends toward 15-25 years thanks to bonus depreciation and MACRS despite the average CFM56 engine having more than a 30-year useful life. Were GAAP to record FTAI’s net debt / assets as being 58%, they would undoubtedly receive a higher rating than BB- from Fitch.

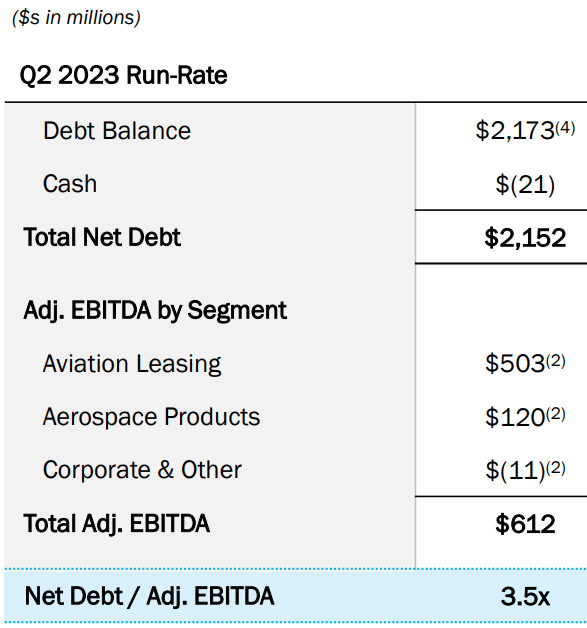

FTAI’s Debt / EBITDA is also a pretty solid 3.5x and expected to continue to stay within the 3-4x range by management. This too implies a rating much better than BB-.

Company Presentation

Unfortunately, Fitch can’t consider implied asset values above book. It must use GAAP accounting figures. Hence the discrepancy which knowledgeable investors can take advantage of.

We would be remiss if we didn’t also note FTAI’s stock can be sold at a 123% price higher than this time last year if necessary and that is unlikely to be necessary as its debt is reasonably well spaced out.

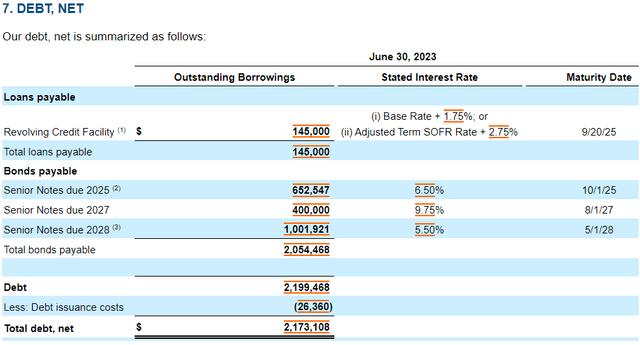

10Q

The first $653 million doesn’t come due until 2025 (after FTAIP switches to floating), and the majority does not come due until 2028. This 2025 debt carries a fixed rate of 6.5% so to be clear with a BB- rating it would likely carry a 1.5 – 2% higher rate. However, it’s worth noting that the company made significant progress in reducing its debt load by paying off or buying back approximately $200 million of the 2025 debt at a discount last year. Thus, if they continue at this rate, the debt should be significantly reduced or potentially even paid off by the time it matures. This would greatly mitigate refinancing risk.

Alternatively, if I were CFO, I would at least consider buying back some FTAIP at a discount on the open market instead of the 2025 6.5% debt. While this preferred yields 9% currently, not that attractive vs. buying back 2025 debt at an effective 8% savings, the CFO should also consider this particular preferred will soon turn into 12.5% floating. Thus, it may also make sense to use some cash flow to buy back some of it.

Regardless, FTAI’s Net Debt / EBITDA, the ability of other BB- Fitch rated firms to refinance at 8% and FTAI’s ability to pay down debt with cash flow implies an ongoing ability to refinance the fixed-to-floating FTAIP preferred to a significantly lower rate as necessary.

FTAI’s Common Dividend provides an additional buffer for Preferred:

Another aspect to consider is the $128 million in common dividends paid by FTAI each year. If push were to come to shove, this cash flow can be used to pay off or refinance debt. Furthermore, not only would the common dividend have to be eliminated before any preferred dividends are cut, but the preferred dividends also represent less than one-fourth of the common. I note in past situations where preferred payouts are relatively small compared to the common and a covenant is breached, it is not unusual for the common dividend to be cancelled but not the cumulative preferred.

Take Away:

In conclusion, investing in FTAIP currently offers an attractive 9.1% yield, and the possibility of a 12.5% floating yield in late 2024, but more likely a 18% yield to first call. We further note FTAIP would need to trade at around $24.50 to produce about the same return as FTAIM. Considering this, FTAIP appears to clearly offer a more favorable deal compared to FTAIM and FTAI’s other preferred.

Potential investors will of course need to conduct their own further due diligence, taking into consideration the risks associated with the company’s leverage. However, we think the risk is significantly less than Fitch’s BB- rating implies. Ultimately, FTAIP’s appeal lies not in the lack of all-risk, but rather in the potential for an above average return vs. the risk actually being taken. Each investor will need to make an assessment of their own risk profile and their appropriate allocation tolerance level prior to making an investment.