Bitcoin is making deeper inroads into American household finances as homebuyers pressured by high borrowing costs and limited supply seek new ways to finance a down payment without selling their digital assets.

On March 26, Better Home & Finance and Coinbase launched a structure that allows eligible borrowers to pledge Bitcoin or USD Coin (USDC) stablecoin to secure a separate loan for a down payment, while still taking out a standard conforming mortgage on the home.

The arrangement brings crypto into one of the most closely watched parts of the U.S. credit system at a time when affordability pressures are already reshaping who can buy a home and when.

Timing is key in the field as Realtor.com’s 2026 report estimates the U.S. housing supply shortage at 4.03 million homes.

This is because the average 30-year mortgage rate recently rose to 7%, while total mortgage applications fell 10.5% and purchase applications fell 5.4%. At the same time, first-time buyers represented just 21% of the market, according to the National Association of Realtors’ latest profile.

Against that backdrop, lenders and crypto firms are betting that a growing class of potential buyers have wealth in digital assets but lack the cash liquidity needed to remove one of the biggest barriers to homeownership.

A new route to the mortgage market

The Coinbase-backed product is aimed at borrowers who want to maintain exposure to crypto markets rather than liquidating their holdings to raise cash for a down payment.

For many, that decision is about more than market timing. Selling cryptocurrencies can also trigger a tax bill and force investors to reduce positions they consider long-term investments.

Given all this, the structure at closing is built around two loans. The first is a standard mortgage on the property. The second is a privately funded loan backed by committed cryptocurrency and used to fund the cash down payment.

Better says the 15- and 30-year mortgage options will be available, subject to loan approval, and that the loans are designed in accordance with Fannie Mae guidelines so that the mortgage remains a conforming loan.

That distinction is important. The product does not replace the traditional mortgage with a crypto loan. Instead, it wraps a crypto-secured financing layer around the down payment, while the main mortgage remains in a conventional format.

For borrowers using Bitcoin, the initial collateral value must be at least 250% of the loan amount in fiat. For borrowers using USDC, the initial collateral value must be at least 125%.

In practical terms, a borrower could pledge $250,000 in Bitcoin to unlock a $100,000 cash loan, or $125,000 in USDC for the same result.

The companies are promoting the scheme as a way to maintain ownership of digital assets while gaining access to the housing market. Better says both loans can have the same interest rate and repayment term, creating one combined monthly payment.

The housing tension creates an opening

The product’s appeal is directly related to a housing market that has become more difficult to access, especially for younger buyers.

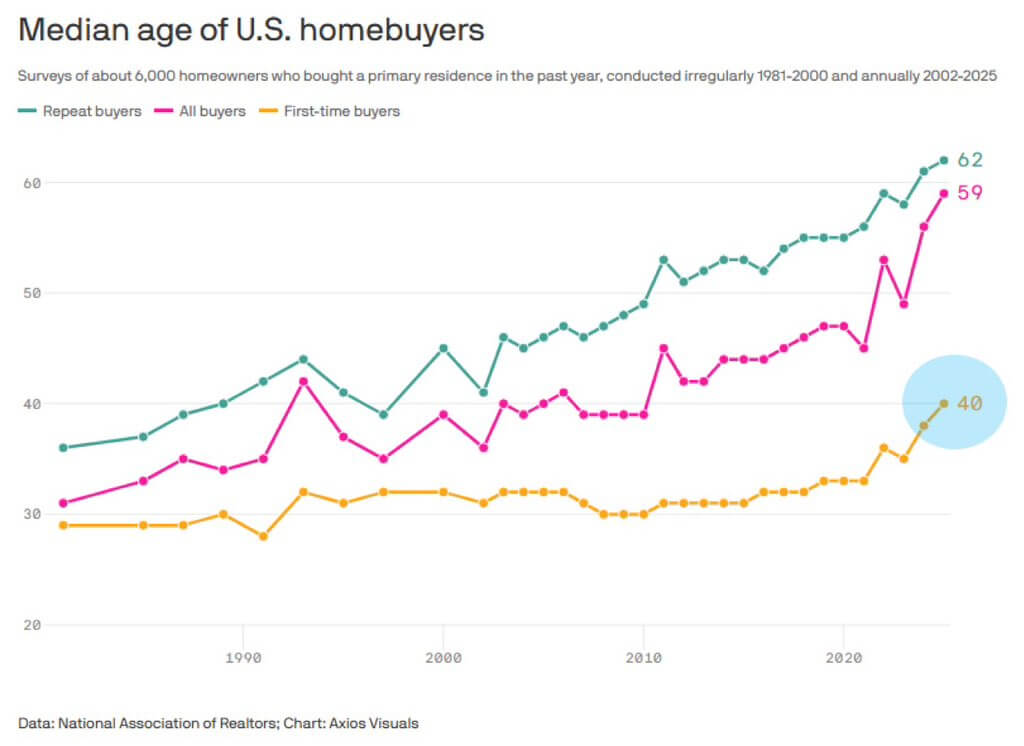

According to the National Association of Realtors, the average age of a first-time homebuyer was 40 in 2025, reflecting the combined effect of high mortgage rates, higher home prices and limited inventory.

The pressure is even greater for households lower on the income scale. The NAHB/Wells Fargo Cost of Housing Index for the second quarter of 2025 found that the average family needed 36% of its income to cover the mortgage payment for an average new home. Among households with a lower income, that share rose to above 71%.

These figures help explain why companies see opportunities in linking digital assets to home financing. Traditional underwriting relies heavily on documented income, credit history and cash reserves.

That framework tends to favor households that have already built wealth through home equity, rising incomes or long-established financial assets.

At the same time, millions of Americans have built positions in crypto. For context, about 20% of American adults, equivalent to 52 million people, own some form of cryptocurrency, and the majority of them are young.

The NCA 2025 State of Crypto Holders report confirmed that 67% of token holders are 45 years old or younger and 26% earn less than $75,000 per year.

That gives the product a clear target audience: younger buyers with significant exposure to cryptocurrencies but limited willingness or ability to convert those assets into cash at the time of purchase.

How the crypto promise works

The companies have tried to structure the product so that it looks less like a volatile crypto loan and more like a mortgage-compatible financing instrument.

Borrowers who pledge Bitcoin or USDC are not subject to margin calls or replenishment requirements if the market value of their collateral declines.

Better says market movements alone do not lead to liquidation. Instead, the pledged assets are only at risk if a borrower falls 60 days behind on payments, a threshold the companies say reflects the treatment of payment stress on conforming mortgages.

The crypto is held in escrow for the term of the down payment loan and returned once that obligation is repaid. Borrowers cannot trade the pledged assets while they are locked up, which preserves ownership but limits flexibility.

For USDC borrowers, the stablecoin can continue to earn rewards, which could help offset mortgage costs and reduce the borrower’s net effective financing burden.

Meanwhile, the broader ambition extends beyond one mortgage product. Better and Coinbase say they plan to expand the scope of eligible digital assets over time to include tokenized equities, fixed income and other tokenized real estate assets.

This is a sign that they see the mortgage offering as a first step in introducing on-chain wealth into mainstream consumer finance.

Policy support and political resistance

Meanwhile, this launch arrives in a political climate that has become more receptive to crypto, but not without resistance.

Fannie Mae’s role, along with the Federal Housing Finance Agency’s oversight, could help make such products more mainstream than previous crypto-linked mortgage offerings.

Last year, FHFA Director Bill Pulte directed Fannie Mae and Freddie Mac to prepare to consider crypto as an asset in mortgage applications, reflecting the Trump administration’s broader support for the digital asset industry.

That policy opening created space for commercial products built around crypto wealth, but also drew criticism from lawmakers who see the idea as a new source of risk for housing finance.

Democratic senators, led by Elizabeth Warren, objected to the proposal. argue that current policy does not allow federally backed mortgage channels to consider cryptocurrency unless it has first been converted into U.S. dollars and properly documented.

They warned that expanding acceptance criteria to unconverted cryptocurrencies could introduce new risks to both the housing market and the broader financial system.

That criticism goes to the heart of the debate surrounding products like Better’s.

Proponents see them as a way to turn digital wealth into access to the real world, without forcing borrowers to sell assets and leave the market. Critics see a danger in bringing a volatile and still-evolving asset class closer to the fundamentals of U.S. home lending.

So the final outcome may depend on whether crypto-backed mortgages remain a niche instrument for affluent digital asset holders, or evolve into a broader financing channel for buyers left out by the traditional down payment hurdle.