")

Araya Doheny

Asana (NYSE:ASAN) checks a lot of the boxes in a typical investment I look for in the tech sector nowadays. The company has posted resilient top-line growth rates while delivering robust operating margin expansion, all in spite of a tough macro environment. The company has a net cash position to help it weather the storm, while retaining the potential for accelerated revenue growth upon an improved macro environment. Management (specifically the CEO) has a large stake in the company and is aggressively buying stock on the open market. To cap it all off, the stock trades at reasonable valuations which do not need a lot of acceleration in growth rates to make it work. I reiterate my buy rating for the stock – this is a name which is getting less and less risky as it continues to execute against its growth opportunities.

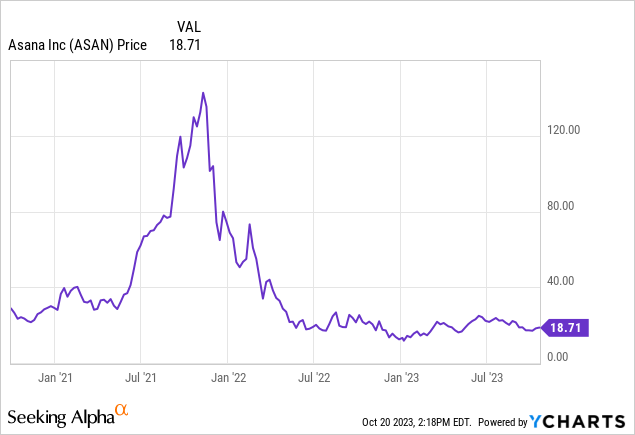

ASAN Stock Price

I am doubtful that ASAN returns back to all-time highs any time soon, as it previously traded at egregious valuations. Even if it falls far short of that, it can still produce solid returns for shareholders at current levels.

I last covered the stock in June where I rated the stock a buy on account of the potential for a generative AI inspired push as well as the large insider buying. The stock has pulled back dramatically since then – increasing the margin of safety and the potential reward.

ASAN Stock Key Metrics

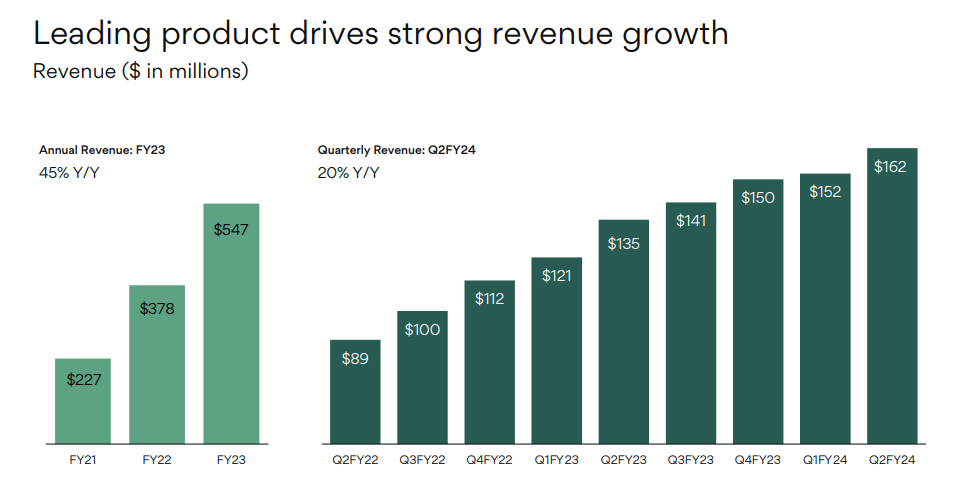

In its most recent quarter, ASAN delivered 20% YoY revenue growth to $162 million, ahead of guidance for $158.5 million. This was a strong number that represented solid acceleration in sequential growth rates.

FY24 Q2 Presentation

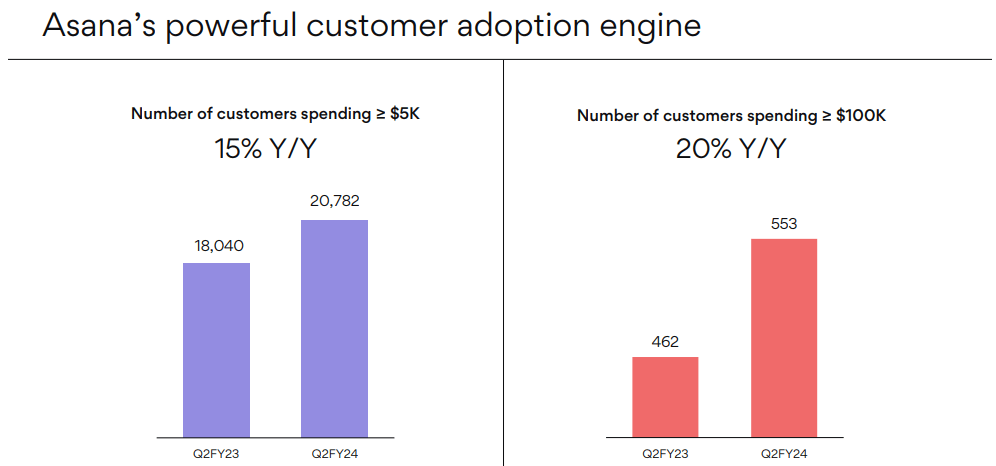

ASAN surprisingly saw solid growth in customers especially among larger customers.

FY24 Q2 Presentation

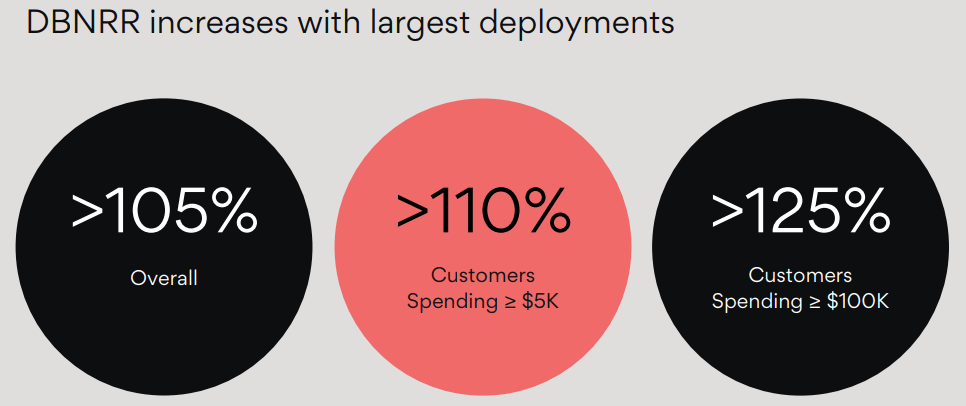

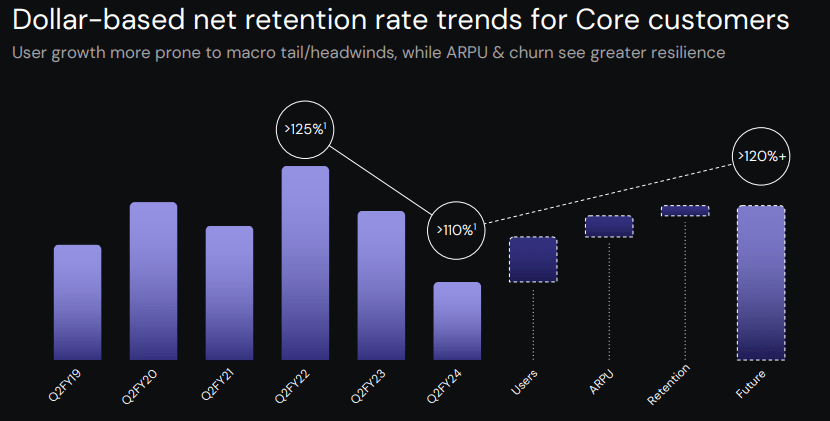

ASAN still saw its dollar-based net retention rate decline to 105%, which held back overall growth rates. Dollar-based net retention rates remain strong among its larger customers at over 125%.

FY24 Q2 Presentation

Management expects the dollar-based net retention rate for “core customers” (defined as customers spending more than $5k) to eventually expand to over 120% upon an improving macro environment, which would help bring back healthy headcount growth.

FY24 Q2 Presentation

ASAN delivered $10.4 million in non-GAAP operating losses, coming slightly ahead of guidance of $24 million in losses. ASAN ended the quarter with $537.5 million of cash versus $45.7 million of debt, representing a strong net cash position capable of sustaining many years of operating losses.

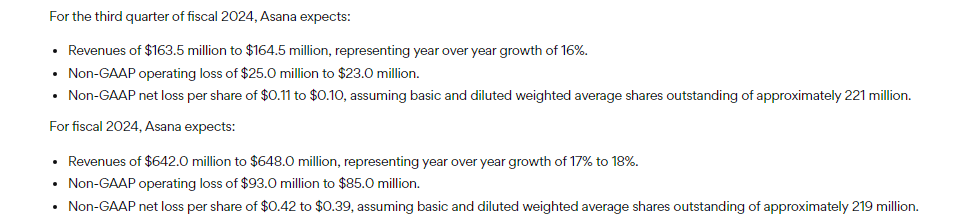

Looking ahead, management maintained its revenue guidance for up to $648 million in revenue for the full year, implying $169.5 million in fourth quarter revenues or 13% YoY growth. Management did however reduce its operating loss expectation from $110 million to $85 million.

FY24 Q2 Presentation

On the conference call, management noted that guidance is incorporating the expectation that the macro environment remains roughly the same moving forward. Management also noted that the tough macro environment has impacted its business due to its large exposure to tech companies (which makes up 30% of its business) – the tech sector has famously undertaken aggressive headcount reductions over the past year. Management expects its dollar-based net retention rates to continue trending lower, but remain above 100%. This is because ASAN has previously been working through changes to its sales organization leadership – growth rates are expected to improve as the company moves past those challenges. Management noted that while free cash flow generation is expected to turn negative next quarter, they remain committed to delivering positive free cash flow generation on a sustainable basis “by the end of calendar 2024.” That distinction of “calendar” versus “fiscal” year seems to imply that we need to wait another year before the company achieves that target.

Is ASAN Stock A Buy, Sell, or Hold?

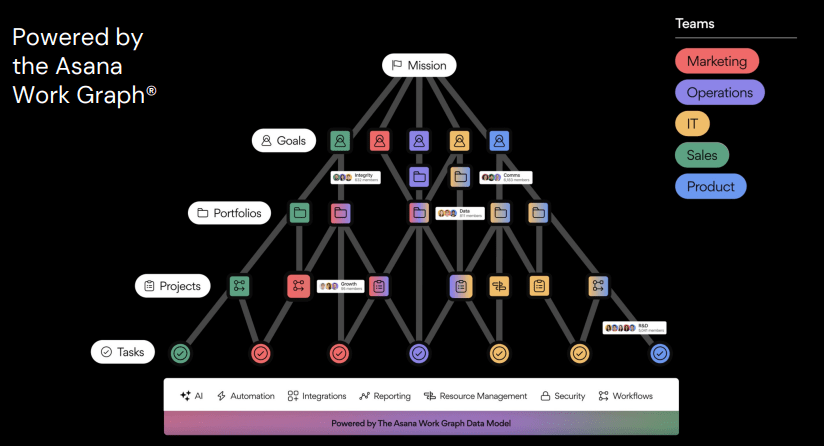

ASAN is an enterprise tech company which helps its customers increase productivity by facilitating organization of project workflow between teams and departments.

2023 Investor Day

Asana’s Work Graph aims to increase visibility of work between departments to drive stronger overall company performance. If you are interested, you can read more about the company’s Work Graph here. The large amount of digital paperwork involved in these processes makes generative AI a natural upgrade to the company’s products. While the tough macro environment is likely to pressure growth rates in the near term, I expect generative AI to be an important catalyst to eventually help accelerate top-line growth over the long term. As of recent prices, the stock traded hands at around 6x sales.

Seeking Alpha

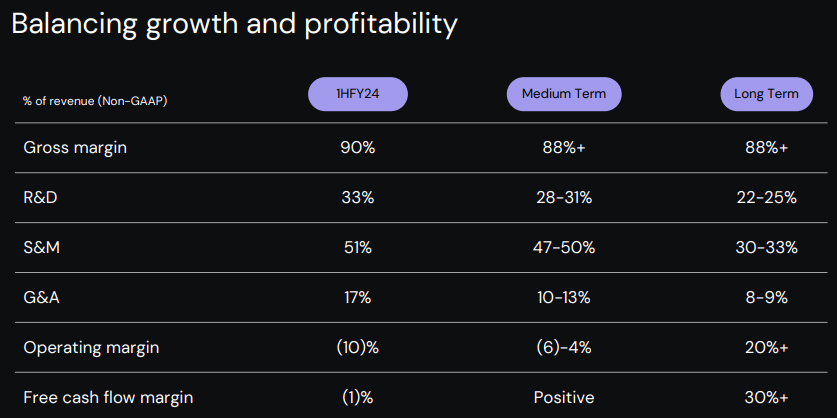

Management has guided for at least 20% operating margins over the long term.

2023 Investor Day

Based on assumptions of 15% revenue growth, 20% long term net margins, and a 1.5x price to earnings growth ratio (‘PEG ratio’), the stock might trade at 4.5x sales, making the current valuation look like nothing special if not a bit stretched. But if the company can accelerate growth to 20% and generate 30% net margins over the long term, then that fair value target jumps to 9x sales, implying sizable upside.

I must remind readers that ASAN is a unique name in the tech sector in that its co-founder and CEO Dustin Moskovitz (who is also a co-founder of Facebook) is a very large shareholder in the company. What’s more, CEO Moskovitz has a very modest compensation plan which the company notes is by his own choice.

2023 DEF 14A

In spite of already owning a large portion of the company’s stock, CEO Moskovitz continues to purchase stock in the open market in large chunks.

Openinsider

ASAN is a true “owner operator” kind of stock – the CEO clearly has high conviction in his company and stock’s prospects.

What are the key risks? ASAN operates in a crowded space and is going up against names like monday.com (MNDY) as well as incumbent Atlassian (TEAM). At some point, I would not be surprised if market saturation occurs and it would become difficult to win customers away from the competition. ASAN does appear to be more of a disrupter in the sector but I suspect that customers will need a steep discounted price in order to switch away from software that they have already been using for many years. In my view, the biggest risk is in the valuation. ASAN, while not obviously overvalued, appears to have gained credit from their CEO’s voracious appetite for the company’s stock. It is possible that Wall Street has been pricing in the potential for CEO Moskovitz to eventually just make an offer for the rest of the company. I find such a scenario to be unlikely and it is possible that as Wall Street comes to the same view, the stock may come under pressure.

I reiterate my buy rating for the stock given the strong balance sheet, potential for accelerating top-line growth, and high insider ownership.