SrdjanPav

All values are in CAD unless noted otherwise.

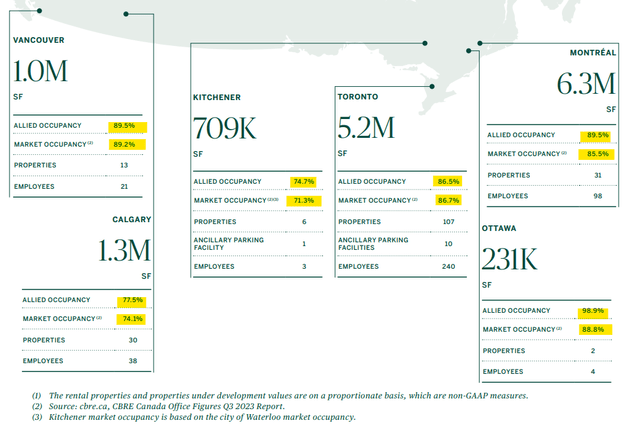

Allied Properties Real Estate Investment Trust (OTC:APYRF)(TSX:AP.UN:CA) holds a portfolio of 200 income earning properties, spanning 14.8 million square feet in gross leasable area or GLA. The good news is that the properties are unique and are located in the downtowns of the respective cities. The not so good news is that these are office properties. Coming back to their unique features, the properties are what are called “Class I” workspaces and are typically characterized by “high ceilings, abundant natural light, exposed structural frames, interior brick and hardwood floors”. Borne from re-use of industrial structures, when available to use, they can look like this or a variation thereof.

Investor Presentation

Offices have not been very popular since 2020, and employers have an uphill task in cajoling their workforce back to the beehive, even on a hybrid basis. With offices giving the Class I building feels, it must make the task a tad bit easier, which explains why, although Allied’s occupancy is far from the best, it is better than most of the collective rest.

Q3-2023 Financial Report

Toronto houses more than half of its portfolio and that is the only market where its occupancy lags the average by a smidge. Montreal and Calgary have around 30 Allied properties each, with the occupancies of 89.5% and 77.5%, respectively. While these numbers, especially those of Calgary, reflect the poor macro environment for this sector, the average occupancy in the two markets is comfortably lower than that of this REIT.

Prior Coverage

We have covered this office REIT on the platform previously, with the most recent being in June of this year. We reviewed the Q1 results and the sale of its data center, at the time. Allied was taking steps to deleverage with the asset sale, and expected its net debt to adjusted EBITDA to decrease from over 10X to 8X, on completion of the sale later in the year. Our verdict summed up our feelings on the business.

8.0X is what we would call a “good start”. Considering conditions for office space, we would aim for at least 7.0X and perhaps a 6.0X if Allied can manage it. If they do get there, you can expect that AFFO would be quite a bit lower, but it will definitely improve the risk-reward profile. As things stand, Allied appears at an attractive discount to NAV and might be a play for those bullish on the office sector. For our part we reject the idea that we need to be chasing this with such negative trends in place. We also remain highly skeptical of the published NAV and think the market has got this more or less correct in terms of fair value of the office buildings.

Source: Allied Properties: Data Center Sale Takes Some Pressure Off

The REIT continues to take a beating and not being lured in by the apparent value was the right call.

Seeking Alpha

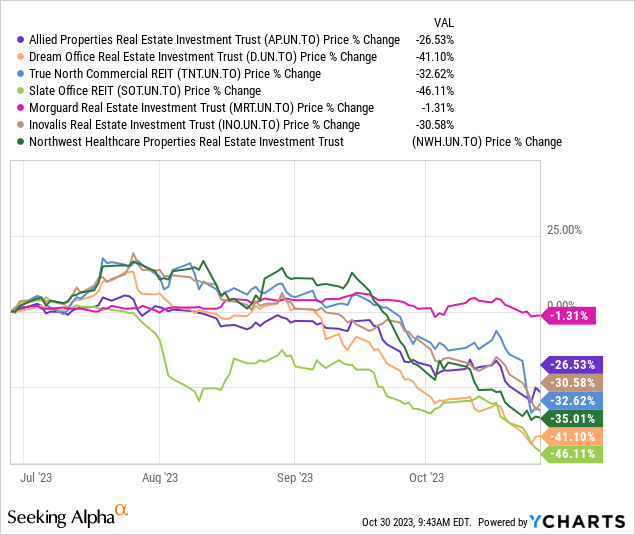

But it is not alone in this misery, in fact, it has not even faced the worst of it.

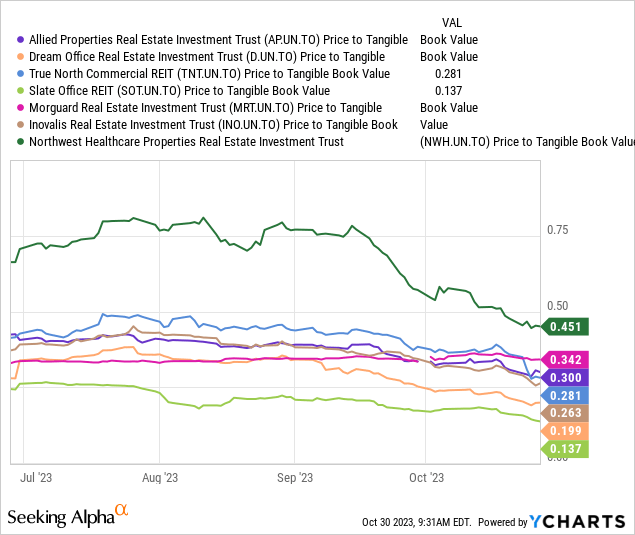

That honor has been reserved for Slate Office REIT (OTC:SLTTF)(TSX:SOT.UN:CA) and Dream Office Real Estate Investment Trust (OTC:DRETF)(TSX:D.UN:CA). The REIT sector, on the whole, has suffered a browbeating over the last few months, but investors have reached within their reserves to eke out a special bludgeoning for anything that relates to an office. Morguard Real Estate Investment Trust (OTC:MGRUF)(TSX:MRT.UN:CA) being the sole vanguard in the above list, possibly thanks to some heavy retail exposure. The market has shown disdain over the net asset valuation published by these REITs and demanded deeper and deeper discounts for investing in them.

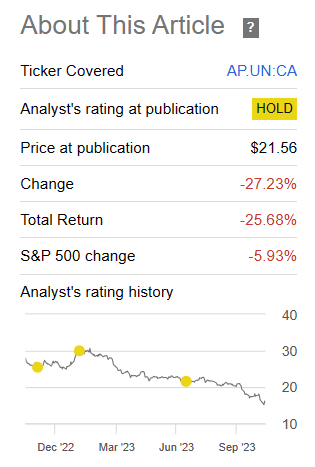

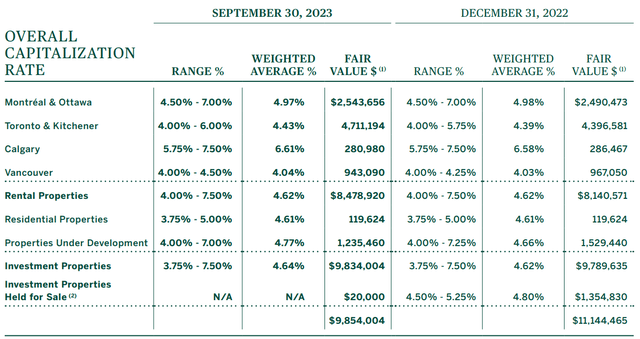

Today, however, Allied will be our object of focus, and the REIT still seems to be in a state of denial as far its capitalization rates are concerned.

Q3-2023 Financial Report

The needle has barely moved since our last coverage (4.62% – overall), giving a whole new definition to the pace of a snail. Let us review the third quarter results that were released a few days ago and see if there is a reason for this show of confidence.

Q3-2023 Results

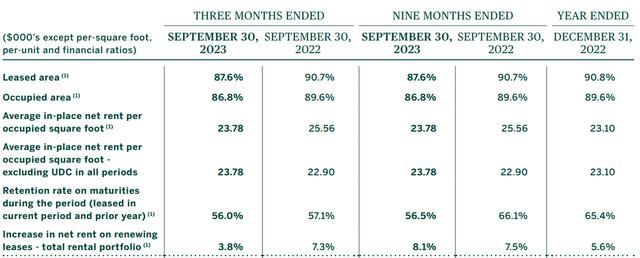

The occupancy, as well as the retention rates were lower year-over-year.

Q3-2023 Financial Report

Excluding the now sold data center, at the end of Q3, Allied had higher average in-place rent compared to the prior periods, as well as to the end of last year. During the Q1 earnings call, Management had expressed confidence that the occupancy levels would rise to the low 90s by the end of the year. While they did not provide a range this time around, with around 1.1 million square feet of GLA under negotiations, they still expect this number to rise in the coming quarters.

Jonathan Kelcher

Okay. And then just switching gears to occupancy. Based on what you’re seeing right now and what you have in your pipeline and what you know about next year’s maturities, do you see occupancy trending up over the next few quarters?

Cecilia Williams

We do feel that, we could be at an inflection point right now. We want to see how deal that we currently have under negotiation materializes over the course of Q4 and then Q1. We have over 1.1 million square feet that we’re currently negotiating across our city portfolio. So we’ll see how those convert to done deals, but we’re feeling pretty confident about things right now.

Source: Q3-2023 Earnings Call Transcript

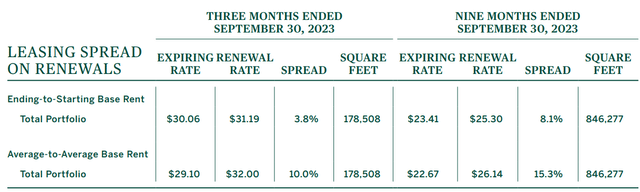

The weighted average lease term was 5.8 years at the end of Q3, with about 10.2% of the portfolio coming up for renewal by the end of 2024. On the renewals it completed in Q3, Allied earned a 3.8% spread, with a 10% spread using the period averages.

Q3-2023 Financial Report

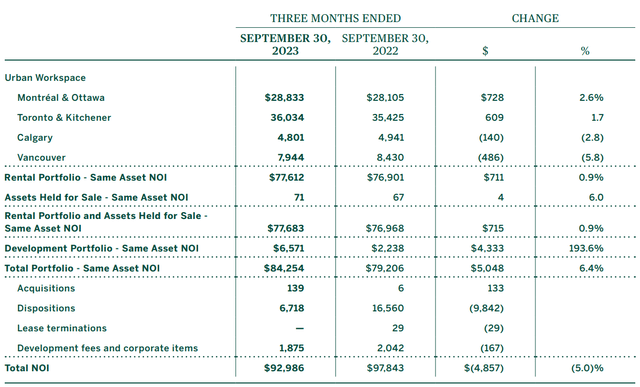

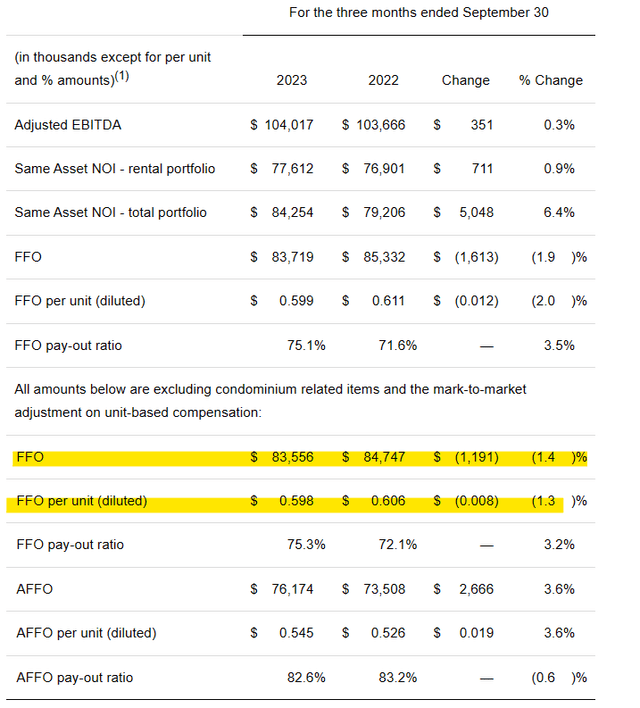

The net operating income or NOI from same assets was higher by 0.9% year over year.

Q3-2023 Financial Report

This increase was aided by the aforementioned rental rate growth, along with higher occupancy in Montreal and Toronto. The jump in variable parking revenue completed the trifecta of good tidings. The overall NOI dropped by 5% compared to the prior year due to the sale of the data center. The 40% increase in year over year interest expenses did not help, and the funds from operations or FFO followed the NOI’s lead with a 1.3% decline.

Q3-2023 Press Release

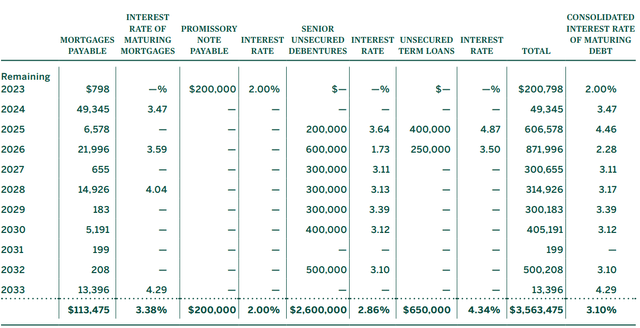

The FFO fell less than the NOI as a higher interest income offset some of that. Point to note on the 40% increase in the interest expense, a portion of this was due to the inclusion of the distributions on LP units under this category on the REIT’s conversion to an open-ended trust. Collectively, on its debt, Allied enjoys a minuscule weighted average interest rate of just 3.10%, with a chunk of it coming up for renewal in 2024.

Q3-2023 Financial Report

The proceeds from the data center sale, however, have provided the much needed liquidity with debt to EBITDA down to 7.9X. Management did say though that they had no plans to draw the paid-down credit facility over the next five years.

Outlook & Verdict

If you believe the cap rates used by management, then there are really no issues going long. There should not be any issues with the debt load either. After all, debt to assets is under 33% according to management. Of course, no one is buying that. Allied entered into an agreement to sell just one tiny asset in Montreal for $20 million, which should close in Q4-2023. If these NAV values are to be believed, Allied should be selling at least $200 million worth of properties a quarter and using 75% of the proceeds for debt reduction and remaining for buybacks. What exactly the REIT is waiting for, we are not sure.

The current implied cap rate is 9.3%, so the market is having absolutely none of it. For our part, we are convinced that this has gone too far, at least relative to where valuation stands today (about 8% cap rates for these properties). It also remains best positioned to navigate the challenges ahead as it has minimal debt and lease maturities over the next 12 months. But we also come back to “why bother?” We believe Allied’s fair value today is at least $20.00, but that does not offer us a compelling setup. There are other REITs where the risk-reward is better like we see for H&R Real Estate Investment Trust (OTCPK:HRUFF) (HR.UN:CA). There, you can bet on office properties while having a cushion from non-office sectors that are better poised to navigate the recession. We continue to rate this a “hold” even though we think bulls finally have some chance of making money.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.