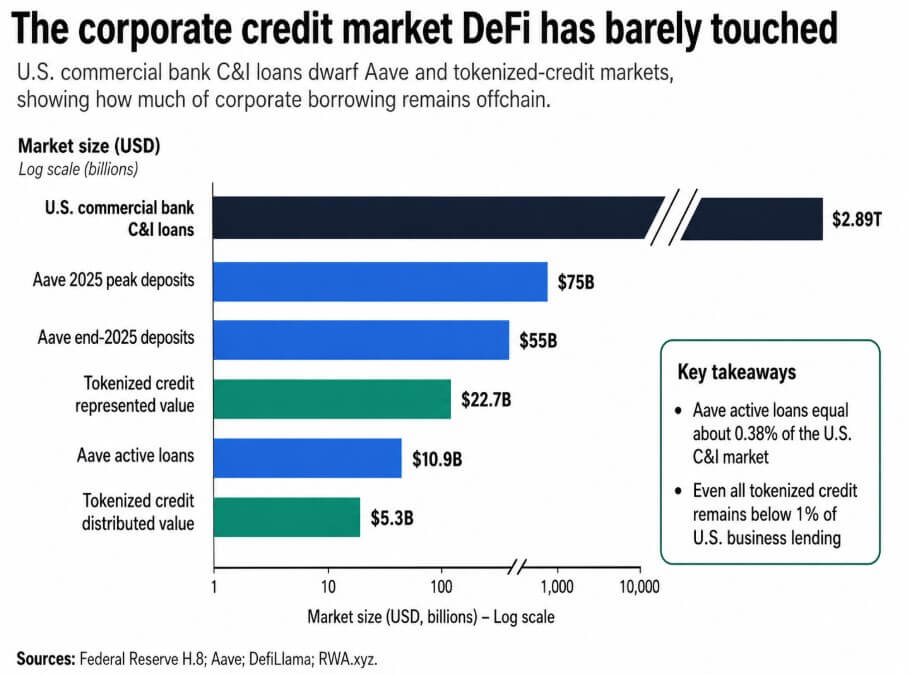

U.S. commercial and industrial lending totaled $2.89 trillion at commercial banks for the week ended May 13, up about $183 billion since the beginning of the year and 8.19% above year-ago levels.

Corporate America has borrowed heavily as interest rates rise and continues to borrow to tighten banks’ lending standards, adding more to bank balance sheets in the first five months of 2026 than most DeFi protocols have ever achieved in total.

Aave ended 2025 with $55 billion in deposits, after peaking at $75 billion, putting the company alongside midsize U.S. banks in terms of asset size. DefiLlama data shows that the current active loan portfolio is $10.9 billion, approximately 0.38% of the U.S. C&I loan market.

Tokenized credit across all on-chain platforms, including Maple, Centrifuge and STOKR, reaches $5.3 billion in distributed value and $22.7 billion in represented value, according to RWA.xyz.

Together, these figures represent less than 1% of what US banks provide to businesses alone.

The tariff paradox

Aave V3 on Base shows a 30-day average $USDC to borrow $APR of 4.24%, compared to the Federal Reserve’s published interest rate on prime loans for US banks of 6.75%.

The Fed’s April Senior Loan Officer Opinion Survey found that banks tightened C&I lending standards for all corporate sizes, increased premiums on riskier loans, and imposed stricter covenants and collateral requirements, even as C&I balances continued to rise.

The collateral risk of Aave interest rates, that is, the cost of accessing liquidity against assets that the protocol can automatically liquidate, while the repayment risk of a bank’s prime interest rates depends on whether a company will generate sufficient cash flow to service its debts.

These are structurally different credit products, and the 250 basis point gap between them reflects that structural difference.

A company typically borrows because it needs capital for cash flows, receivables, inventories, purchase orders, or future contracts. These are the business fundamentals that a bank endorses, and Aave cannot yet assess the chain.

Aave’s own V3 documentation describes the lending model as always being over-collateralized, with liquidations triggered when collateral coverage falls below defined thresholds.

This structure works well for crypto-native borrowers looking for stablecoin liquidity, but leaves corporate borrowers without a suitable product.

What the infrastructure still lacks

Cash flow underwriting requires evaluating a borrower’s ability to repay over time from sales, margins and contracts.

DeFi protocols price token collateral dynamically and accurately, without an equivalent mechanism for assessing a company’s revenue quality or covenant compliance.

Corporate loans are useful precisely because the borrower does not have liquid collateral equal to the amount borrowed, and DeFi’s most proven credit markets rely on overcollateralization to reduce default risk by eliminating the need for trust.

Real-world collateral requires valuation, verification, custody, legal enforceability, and recovery processes that smart contracts alone cannot perform.

Tokenized lending platforms like Maple and Centrifuge have made progress, but their combined distributed value of $5.31 billion represents a fraction of the obligor-backed loans flowing through traditional banking facilities each quarter.

Aave can liquidate ETH or $USDC collateral in a single block, while corporate credit training involves covenants, waivers, restructuring negotiations, servicers, bankruptcy proceedings and courts.

Aave’s Ethereum/$USDC to borrow $APR on May 26 was 12.82%, compared to a 30-day average of 4.72% for the same pool, which tripled over the measurement period.

A corporate treasurer managing a revolving credit facility needs a predictable cost of capital, and that shift makes on-chain variable credit structurally incompatible with standard treasury practice.

Aave’s credit delegation mechanism allows vendors to delegate lending authority to other users, with enforcement via off-chain legal agreements or on-chain smart contracts, demonstrating that DeFi has the conceptual primitives for collateralized lending.

It also shows why the bridge to corporate lending still runs through legal infrastructure and off-chain trust, the very components that DeFi has not yet automated at scale.

Two speeds

In the bull case, tokenized collateral rails, institutional credit managers, stablecoin settlement, and enforceable claims converge into a functioning corporate credit funnel.

On-chain private credit could reach $100 billion to $300 billion, between 3.5% and 10.4% of the current U.S. C&I market. The path will first run through crypto-native companies and fintech lenders, where borrowers are already active in digital asset environments, before expanding to traditional corporate borrowers.

The April CPI is at 3.8% annualized, wage growth is slowing to 115,000, and the tightening of credit standards for banks are creating conditions where programmable alternative credit rails should attract the attention of treasuries that already use stablecoins for settlement.

In the bear scenario, DeFi acts as a powerful liquidity market for crypto-backed loans, while corporate credits largely remain on bank balance sheets.

On-chain credits are in the $5 billion to $20 billion range, less than 0.7% of the C&I market, as the legal, underwriting, and recovery infrastructure matures more slowly than token markets.

Banks retain the compliance, reporting and legal recovery apparatus that corporate borrowers need, and building an equivalent infrastructure across the chain takes longer than deploying a new credit pool.

DeFi has demonstrated that on-chain money markets can handle deposits, interest rates, automated liquidations, and global stablecoin liquidity at meaningful scale.

The next opportunities in corporate lending lie in underwriting capacity, legal enforceability and institutional trust.