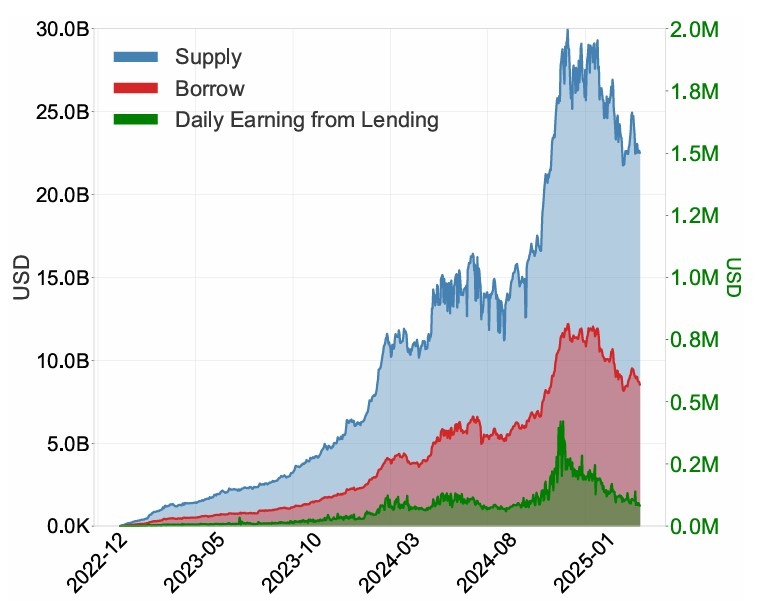

A Bank of Canada staff document showed that Aave V3 reported zero non-performing loans in 2024, with overcollateralization and automated liquidations helping to prevent lender losses in the Ethereum lending market.

Using transaction-level data from January 27, 2023 to May 6, 2025, the study found that positions were typically liquidated before the value of collateral fell below outstanding debt, helping to limit lenders’ losses across the sample.

But the model came with a trade-off, the paper said. While it protected lenders from uncovered losses, it also shifted risk to borrowers and limited capital efficiency compared to traditional lending systems.

According to the article, Aave V3’s design is based on automated risk controls rather than traditional underwriting, which requires borrowers to post more collateral than they borrow and liquidate positions when they exceed risk thresholds.

Recursive leverage stimulated loan demand

According to the paper, Aave V3’s lending activity was not driven solely by users seeking liquidity. This showed that recursive leverage accounted for more than 20% of total loan volume and 8.2% of loan transactions during the sample period.

Recursive leverage involves repeatedly borrowing against collateral, deploying the borrowed assets as new collateral and borrowing again to increase exposure.

Related: Aave V4 goes live on Ethereum after board vote approved the rollout

According to the study, the dynamics left borrowers more exposed as markets turned. According to the paper, liquidations on Aave V3 typically occurred in concentrated waves, with four assets accounting for 90% of the total liquidated value.

This includes Wrapped Ether (WETH), Wrapped Staked Ether (wstETH), Wrapped Bitcoin (WBTC) and Wrapped eETH (weETH).

The paper estimated that borrower losses during major liquidation events could be significant. It said liquidation costs typically ranged from 5% to 10% of liquidated value, while missed profits from subsequent price recoveries pushed combined losses to around 10% to 30% in some cases.

The staff document suggested that while the design for Aave V3 helped prevent uncollected bad debts in the sample, it did so by exposing borrowers to abrupt losses when collateral prices fell sharply.

Cointelegraph contacted Aave for comment but did not receive a response before publication.

Magazine: Are DeFi developers liable for the illegal activities of others on their platforms?