Aave, the leading credit protocol, will pursue a “revenue-based protocol strategy” over the next 12 months, according to founder Stani Kulechov.

Kulechov believes this is the next phase where DeFi moves beyond the token speculation phase. write on X“Sustainable, consistent revenue proves that DeFi can evolve from pure token speculation to sustainable businesses backed by balance sheets.”

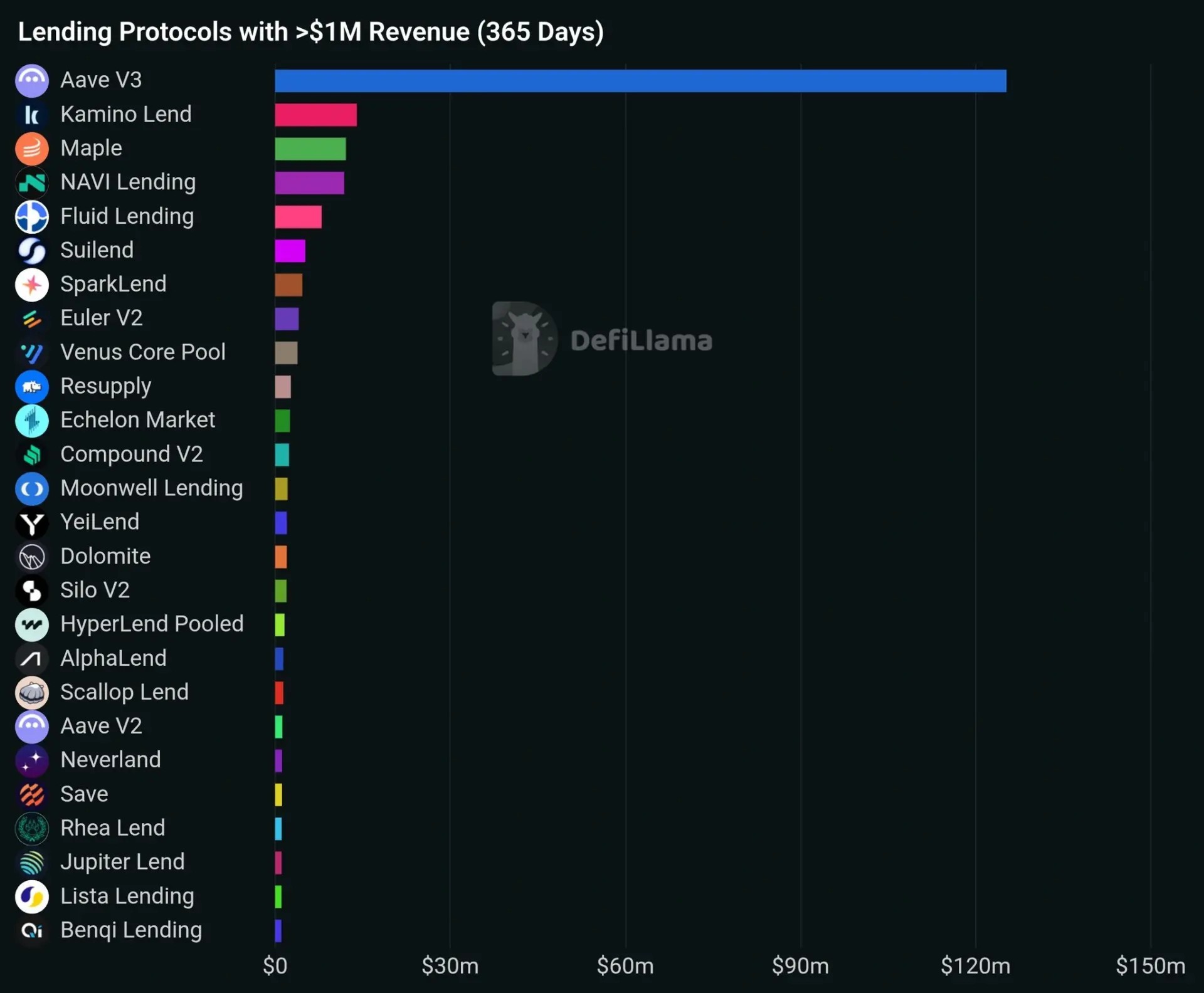

How does Aave’s revenue compare to other lending protocols?

Data from DeFiLlama shows that Aave has generated $7.96 million in fees over the past seven days and over $14 billion in total value retention (TVL). No lending protocol comes close to either benchmark, with the next on the list in terms of largest TVL, Morpho, at $7.5 billion, while JustLend trails at over $3.5 billion.

DeFi analyst DeFi Tiger highlighted the gap on Xnoting that Aave V3 alone made more in the past year than the rest of the lending protocols in the rankings combined, adding that while most lending markets are still fighting for market share, Aave is already the credit layer through which DeFi runs.

The launch of the V4 is gaining traction

On May 22, Frax, the news platform linked to DeFi platform Frax Finance, reported that V4’s combined deposits and loans exceeded $100 million for the first time, with $80 million in deposits and $25 million in loans. That milestone came just one day after Kulechov himself noted that V4’s offering had reached $75 million and incentive programs had gone live.

That same day, Kulechov had posted on X: to report that “Aff [is] will expand into institutional loans and loans with Aave V4 and $GHO.” $GHO is the protocol’s own overcollateralized stablecoin.

Aave has been placing aggressive expansion bets

Aave has been busy this year pursuing several initiatives that fit its revenue-focused strategy, despite an exploit that led to more than $10 billion exiting the protocol in April. The turnover strategy fits in with a pattern of initiatives that Aave has followed this year.

Cryptopolitan has previously reported on Aave’s consideration of a return-based charity giving featureallowing users to divert interest on deposits to humanitarian causes while keeping the principal intact. That proposal emerged in May as a temporary executive check, positioning the protocol as more than a pure credit market.

Previously, in March, Aave Labs has rolled out the V4 reinvestment moduledesigned to leverage approximately $6 billion in inactive stablecoin deposits for low-risk return strategies. The same update introduced email and password logins to the Aave app, eliminating the need for seed phrases and lowering the barrier for new users.

Institutional interest has followed. In April, Grayscale’s head of research discussed Aave’s potential to become a “household name,” while an analytical article from the Bank of Canada on Aave V3 concluded that DeFi lending is “operationally viable” with good governance.

The future of Aave

Kulechov’s 12-month timeline will depend heavily on the extent to which V4 adoption maintains its current momentum. The institutional integrations also appear to be an integral part of the strategy, and bringing all these integrations together will go a long way in achieving the goal of the protocol.

There is also the protocol’s governance that needs to be stabilized after a turbulent first quarter that saw the departures of key contributors BGD Labs and the Aave Chan Initiative (ACI).