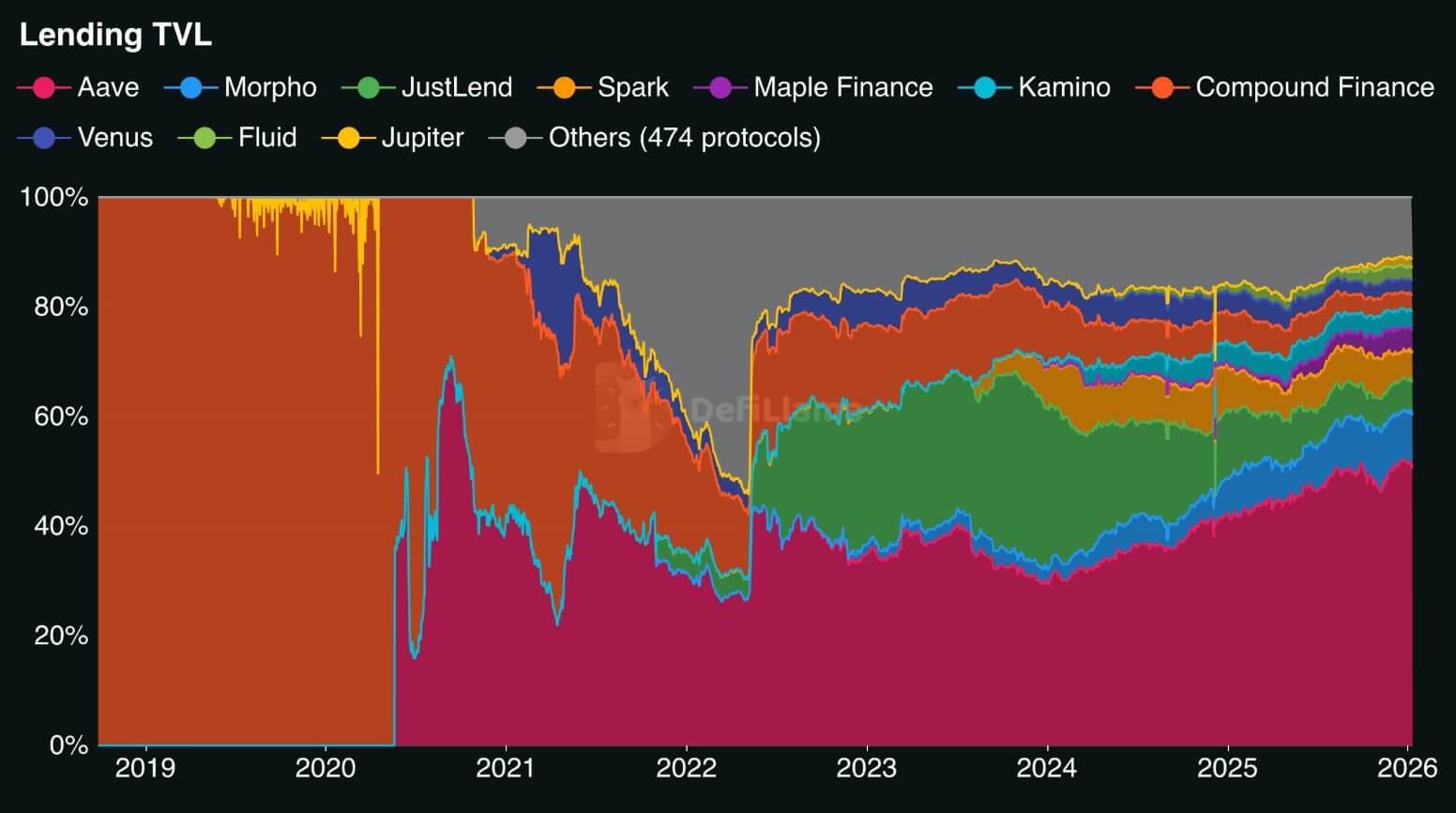

Aave now holds 51.5% of the DeFi lending market share, the first time since 2020 that a protocol has surpassed the 50% threshold.

The milestone is achieved not by the collapse of competition, but by steady accumulation: Aave’s total value of $33.37 billion sits atop a $64.83 billion credit class that has consolidated around a single liquidity hub.

The concentration raises a question that DeFi has been avoiding for years: When one protocol becomes the ecosystem’s primary margin driver, does efficiency create vulnerability?

The answer depends on the metric used.

Aave’s Total Value Locked (TVL) dominance reflects collateral retention and not credit exposure. DeFiLlama excludes borrowed money from TVL calculations for loans to avoid inflating the numbers due to cyclical lending.

As a result, Aave’s $24 billion in outstanding loans translates to a 71% borrowed/TVL ratio, meaning the protocol has meaningful leverage on top of its collateral base.

That makes Aave less of a passive vault and more of an active leverage machine, with systemic risks manifesting not in size, but in the speed and violence of forced deleveraging when markets turn.

DeFi liquidation engine at scale

The October 10 washout offered a preview.

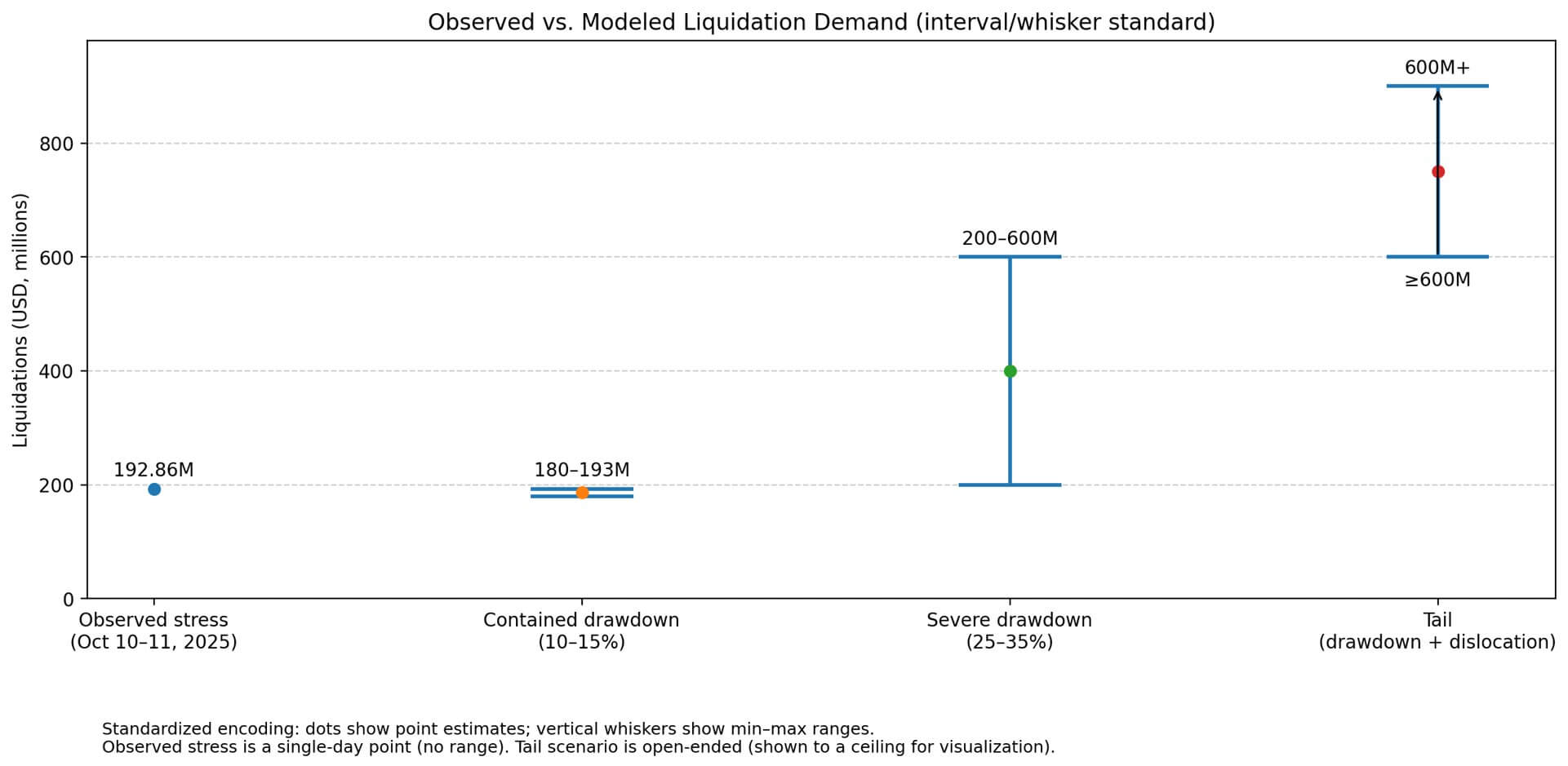

Over two days, Aave on Ethereum processed $192.86 million in liquidations, with wrapped Bitcoin accounting for $82.17 million of the total.

The episode marked the third largest liquidation day in the protocol’s history. Liquidators collected about $10 million in bonuses, while Aave’s coffers collected $1 million in fees.

The system worked: collateral moved from underwater lenders to liquidators with no observable accumulation of bad debts or failing oracles.

But the October stress test took place under favorable conditions: stablecoins held up, on-chain liquidity remained high, and the decline was limited to large asset moves at high rates.

The real systemic question arises when these assumptions break.

When a 25-35% drop coincides with dislocations of stablecoins or liquidity-sensitive tokens such as liquid staking derivatives trading well outside their theoretical value, the landscape changes quickly.

Aave governance documents explicitly recognize this tail risk: a January 2026 proposal lowered supply and borrowing limits for USDtb while finalizing oracle adjustments, citing the need to “increase liquidation profitability and reduce the likelihood of bad debt” during potential depegs.

Aave’s concentration creates a feedback loop. Because it is the dominant location, it attracts more collateral, and as collateral grows, liquidation events scale proportionately. As the size of the liquidation increases, the protocol’s ability to absorb stress without moving prices becomes the system’s main shock absorber.

Traditional financial institutions would classify this as a systemically important financial institution, but with automatic liquidations replacing human margin calls and no lender of last resort beyond a government-controlled backstop of $460.5 million.

Backstop arithmetic and asset-centric coverage

The Safety Module’s $460.5 million represents approximately 2% of Aave’s outstanding loans.

The board is transitioning to umbrella modules, which provide asset-based deficit coverage instead of blanket guarantees. USDC covers are used in this module $USDC shortages, for example.

The design choice reflects a trade-off: capital efficiency versus system coverage.

A general reserve large enough to cover the tail losses of all borrowed assets would require the immobilization of capital on a large scale. Instead, asset-scoped modules distribute coverage but leave contamination scenarios between different assets partially uncovered.

The protocol’s risk controls work via active parameter adjustment instead of static buffers.

Recent board actions include interest rate changes on Base as liquidity mining incentives expire and oracle design choices that prioritize the profitability of liquidations during stress.

This approach mirrors the way a prime broker manages margins in traditional markets, with continuous monitoring, dynamic risk limits and proactive deleveraging before positions become unrecoverable.

However, prime brokers work with credit teams, discretionary margin calls and access to central bank facilities during liquidity crises. Aave runs on immutable smart contracts, deterministic oracles, and curatorial incentives.

When these mechanisms work, the protocol is phased out smoothly. If they don’t, or if external liquidity evaporates faster than the trustees can execute, bad debts pile up.

Modeling DeFi stress without wild assumptions

Three DeFi scenarios frame the range of plausible outcomes, each anchored in perceived liquidation sizes rather than speculative projections.

With a limited decline of 10-15%, movements in key assets with stable stablecoin pegs and normal on-chain liquidity, liquidation volumes are likely to mirror October’s range of $180-193 million.

In this case, Aave acts as a shock absorber, the liquidators benefit and the system is rebalanced. The systemic risk remains low because the protocol is designed exactly for this scenario.

A severe decline of 25-35%, with widening spreads and tighter liquidity, could push liquidations one to three times higher than recent stress days, or roughly $200-600 million during the peak period.

Contagion depends on whether forced sales move collateral prices enough to trigger liquidations in other protocols. This is where concentration matters: if multiple locations use similar collateral sets and Aave handles the bulk of the deleveraging, the price effects spread more quickly than if liquidations were spread across competing protocols.

The tail scenario involves a major collateral withdrawal or disruption of lending assets, such as a liquid derivatives strike trading significantly below its fixed value, or a stablecoin breaking its dollar anchor during a spike in liquidation demand.

Here, liquidation volumes could exceed $600 million as oracle adjustments lag price movements and liquidity providers take a step back.

This is the case when Aave’s role as a primary margin driver creates real systemic exposure: correlated collateral, concentrated liquidation demand, and disrupted execution infrastructure coming together at the same time.

What 51.5% actually means

Crossing the majority threshold is likely a signal that DeFi lending has entered a natural monopoly phase, where liquidity generates liquidity faster than competitors can match.

The systemic risk implications depend less on static market share and more on whether Aave’s liquidation mechanism, oracle design, and backstop capacity increase proportionately with growing exposure.

Recent board actions indicate that risk management is keeping pace with growth. The protocol has processed multiple liquidation days of $180-193 million with no observable bad debt spiral.

Nevertheless, these stress tests took place under relatively favorable conditions. The tail scenario in which systemic risks materialize involves correlated collateral shocks, liquidity dislocations, and forced deleveraging at rates beyond the capacity of the trustee or the responsiveness of the oracle.

Aave’s dominance makes it the most important margin driver in DeFi.

Whether that leads to vulnerability or resilience will not be determined by market share, but by the protocol’s ability to handle liquidations under conditions it has not yet experienced, and whether the ecosystem has viable alternatives if it cannot.