Oil is making a comeback – even faster than I expected. Despite weak economic growth, poor consumer health, Chinese growth fears, and a hawkish Fed, WTI crude oil is back above $90.

Hence, in recent weeks, I have increased my coverage of oil and gas companies. On September 25, I wrote an article titled 18% Yield Potential At $100 Oil: Why Canadian Natural (CNQ) Is My Favorite Play.

Canadian Natural is one of my three largest oil holdings. The other two are Pioneer Natural Resources (PXD) and Chevron (CVX), which I bought because of merger expectations when oil was still subdued – and because it’s a fantastic oil major.

One stock that readers keep bringing up is Diamondback Energy (NASDAQ:FANG), a stock I have covered a number of times in the past. The only reason why I do not own it is that I’m not looking to own too many individual oil stocks in a portfolio consisting of fewer than 25 stocks.

However, I am considering buying it with the proceeds from a potential CVX sale at some point in the future. After all, FANG is one of my favorite oil companies.

In this article, I won’t just update my oil thesis after covering the stock in July, but I will also walk you through the updated bull thesis for FANG, which consists of deep inventories, very efficient operations that come with low breakeven prices, a solid balance sheet, and shareholder-friendly distribution plans.

I also expect that FANG will continue to do what it does best during bull markets: outperform its peers.

So, without further ado, let’s dive into yet another upstream giant I love!

$100 Oil?

As usual, I am starting these articles with an update on the oil situation.

Right now, a lot of people are scratching their heads. Why is oil so high if the economy is so bad?

Bloomberg

The answer is because of supply. Not only is U.S. shale production running out of steam, as I discussed in the aforementioned CNQ article (and almost every oil article I’ve written since 2020), but we’re also seeing OPEC production cuts.

On top of that, as Bloomberg reports, oil buyers worldwide are grappling with surging premiums for oil supplies, marking some of the highest prices seen in months or even years.

Bloomberg

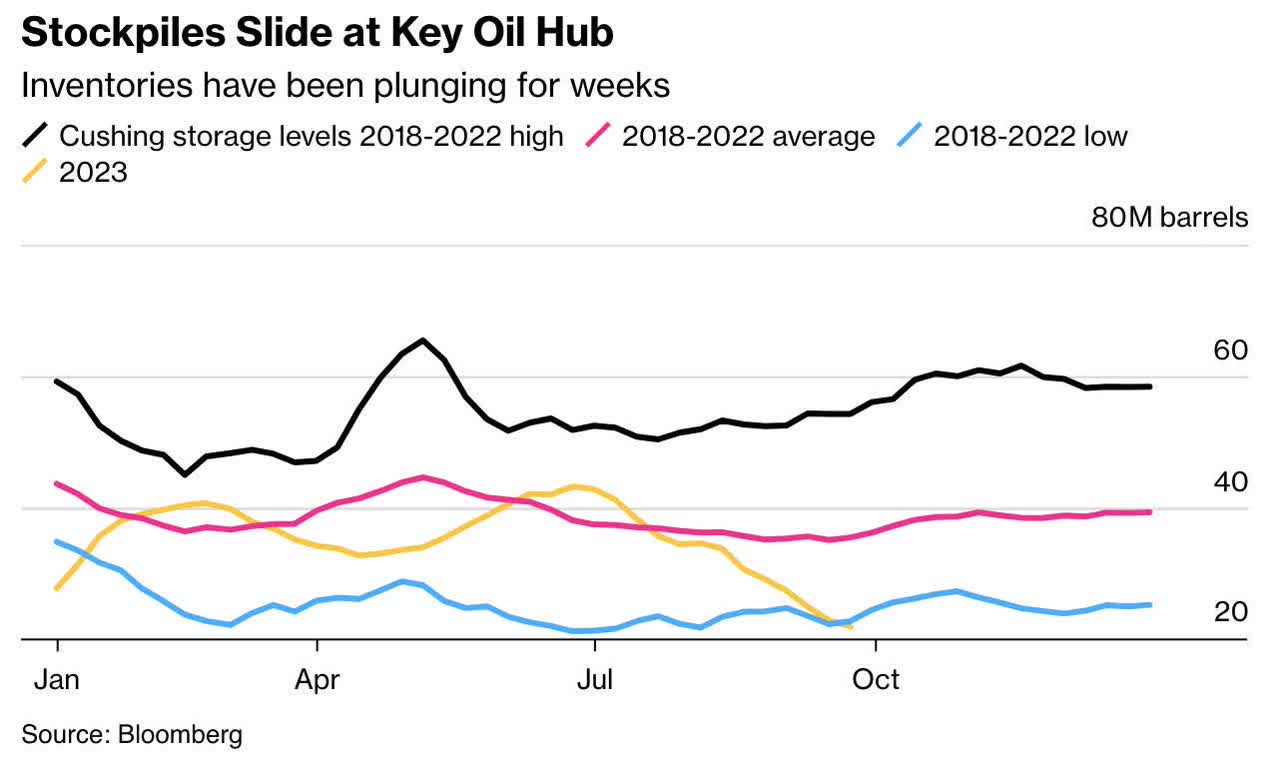

This spike in costs is a ripple effect of dwindling stockpiles at the largest U.S. storage hub in Cushing, Oklahoma. The ramifications of this situation are working their way through international markets, affecting Asia, the Middle East, and Europe.

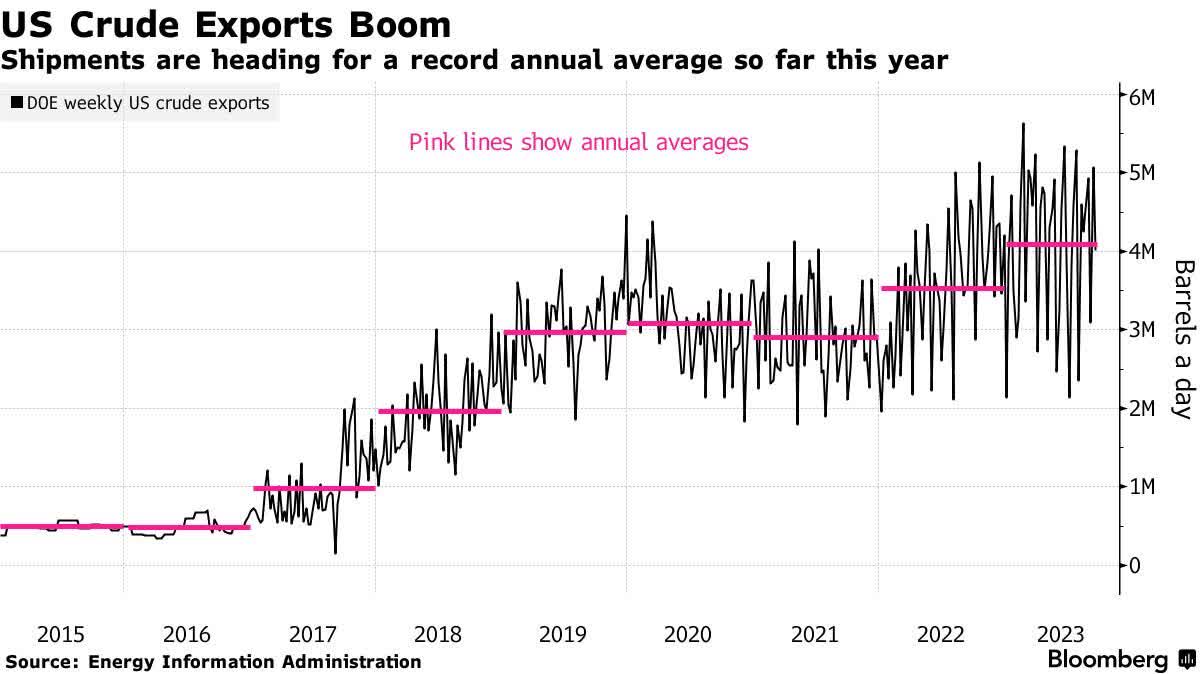

Furthermore, export demand remains high.

While there’s been a lot of angst over the shrinking US inventories, there are yet to be any concrete signs of a slowdown in American exports.

“Waterborne exports in October are still likely to come in close to 4 million barrels a day,” said Matt Smith, oil analyst at Kpler. “The lagged impact of the tightening Brent-WTI spread means we may not see the full impact until November’s loadings.”

Bloomberg

For November and beyond, it’s still likely exports will hover around the 4 million barrels a day level, Smith said, citing strong domestic shale production. – Bloomberg

If we were in a normal situation, we would likely see a rapid surge in U.S. oil production. However, that is not happening now.

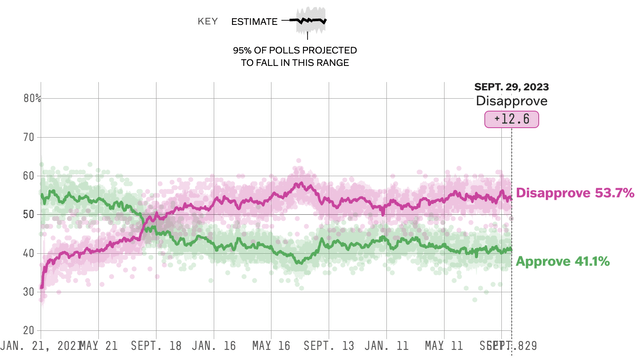

As reported by the Wall Street Journal, this reluctance to increase production is raising concerns about consumer fuel costs, challenging the fight against inflation, and posing new challenges for President Biden’s upcoming 2024 election campaign, which is going to be an uphill battle if the economy continues to develop like this.

Biden’s unfavorable rating is quite significant despite low unemployment.

FiveThirtyEight Interactives

Going back to the Wall Street Journal article, while some analysts predict oil prices may hit $100 a barrel soon, American frackers are cautious.

Unlike previous years when they flooded the market with crude to stabilize prices, this time, they seem to be holding back, potentially keeping oil prices elevated until external factors impact production or demand subsides.

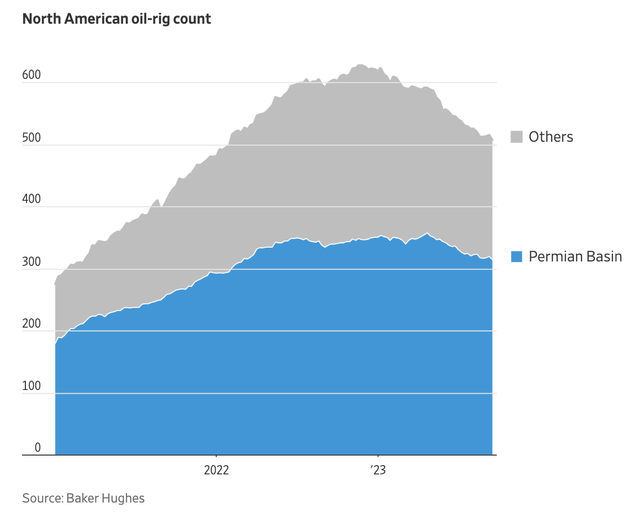

In the Permian Basin of New Mexico and West Texas, the most active oil field in the United States, the number of drilling rigs for crude has declined by approximately 12% to 314 since the end of April, even as U.S. oil prices increased by around $13 a barrel during the same period.

Wall Street Journal

Most shale companies have committed to rewarding investors with share buybacks and dividends rather than rapidly increasing drilling efforts in response to inflation and elevated interest rates.

Companies are also protecting reserves, as a lot of companies are running out of Tier 1 reserves. Even the Permian is expected to see peak production in 4Q24.

Ovintiv, for example, purchased three private Permian operators in April for a combined $4.3 billion and has since idled five of the rigs those companies had been using. – Wall Street Journal

Furthermore:

Despite rising oil prices, investors have continued to signal they won’t pour money into companies seeking to increase drilling, as they did in years past. “We tried to tempt our respondents by asking, ‘What if oil is $90 [a barrel]?’” the firm said. “Most, but not all, claimed activity will not change.” – Wall Street Journal

While I do not rule out another oil price decline to the $75 to $80 area if economic growth weakens further, my longer-term thesis remains unchanged.

I believe that rebounding economic growth in the future will more than likely lead to a situation of prolonged triple-digit dollar oil prices. I do not believe in $200 to $300 oil, but $100 to $130/$140 is definitely possible.

This brings me to Diamondback Energy, which is one of the best places to be when betting on elevated oil prices – or just buying great long-term oil exposure.

What’s Diamondback?

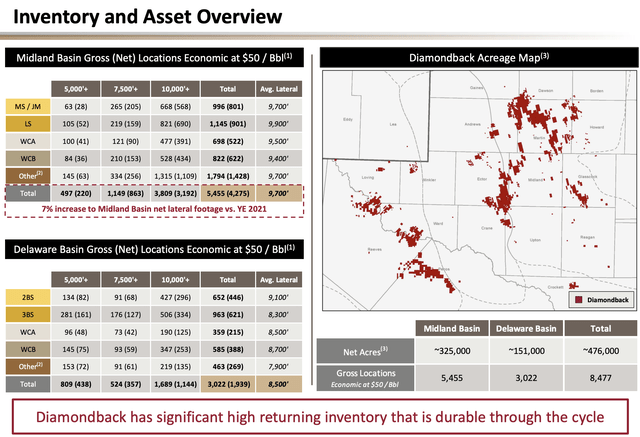

FANG is an independent oil and natural gas company primarily focused on unconventional, onshore oil and natural gas reserves in the Permian Basin in West Texas.

As of December 31, 2022, FANG held a substantial acreage position in the Permian Basin, with approximately 615,348 gross acres.

The majority of this acreage is located in the Midland Basin and the Delaware Basin, known for their high concentration of oil and liquids-rich natural gas.

Please note that the numbers in the overview below are NET acres.

Diamondback Energy

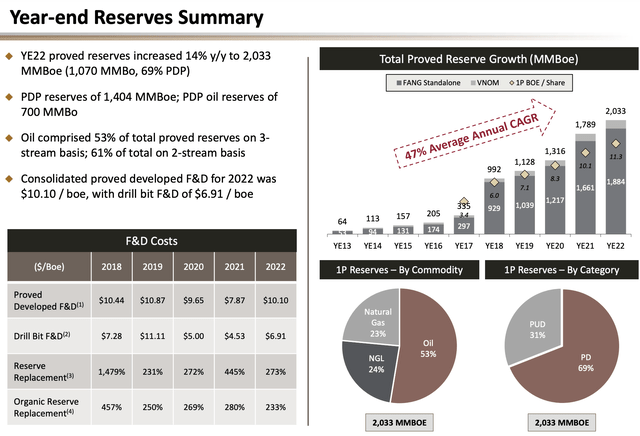

The estimated proved oil and natural gas reserves as of this date were approximately 2,032,971 MBOE, with a significant portion being proved developed producing reserves.

Diamondback Energy

This gives the company at least 12 years’ worth of production at current rates, excluding any future discoveries.

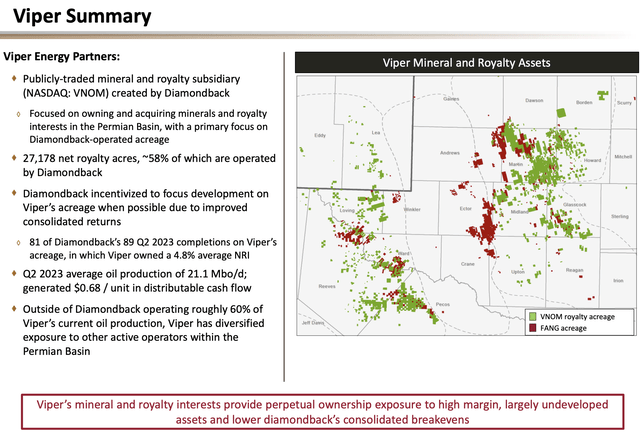

Furthermore, the company has substantial midstream (pipelines and related) investments. It owns the General Partner of Viper Energy Partners LP (VNOM) and 56% of the limited partner interest.

Diamondback Energy

Having said that, there’s a lot more to discuss.

What Makes Diamondback So Special

In addition to having deep reserves and a well-diversified focus on America’s go-to basin, it also has top-tier production.

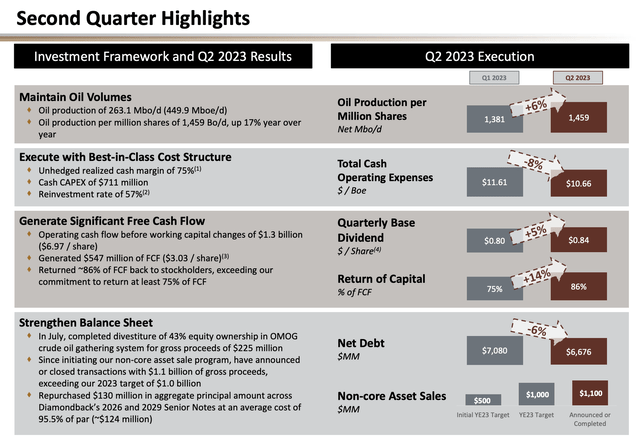

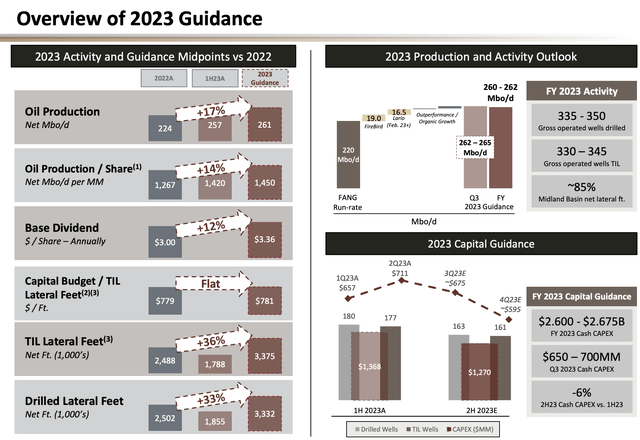

In the second quarter of 2023, Diamondback Energy achieved volume outperformance, with both oil and total production exceeding the high end of their respective guidance ranges.

Notably, oil realizations stood at an impressive 97% of WTI pricing. This strong performance was accompanied by a robust hedging program, providing a vital insurance policy to mitigate downside risks and protect the dividend.

Diamondback Energy

Looking ahead, the company anticipated a 5% reduction in cash capital expenditures for the third quarter, projecting a range of $650 – $700 million. This reduction is attributed to lower well costs, decreased drilling activity, and a slower completion cadence. For the full-year 2023, the company set a revised cash capex guidance of $2,600 – $2,675 million, reflecting a slight increase at the midpoint.

Diamondback Energy

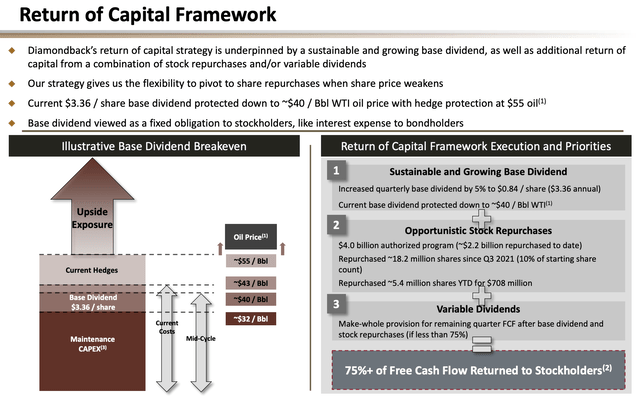

As some of these numbers may be vague, let me give you a few other numbers that are very impressive. FANG’s operations are so efficient that it is able to protect its base dividend at $40 WTI! This would protect free cash flow in the high-$30 WTI range, making FANG one of North America’s most efficient drillers.

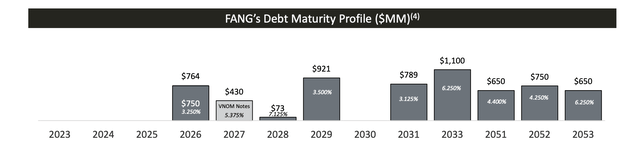

The company also has a BBB-rated balance sheet with zero maturities until 2026. It has a net leverage ratio of roughly 1x EBITDA and uses the proceeds of non-core asset sales for further debt reduction.

Diamondback Energy

I’m bringing this up because, in combination with low breakevens, the company is in a great spot to accelerate shareholder distributions.

Thanks to low debt levels, debt reduction is NOT a capital priority of the company.

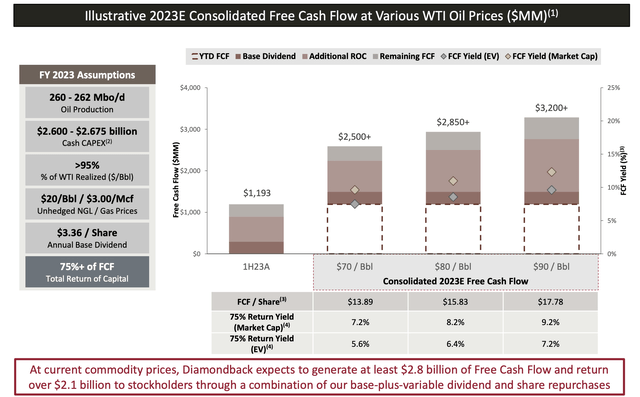

It has other priorities (as seen in the overview below, which also shows its hedges and breakeven point):

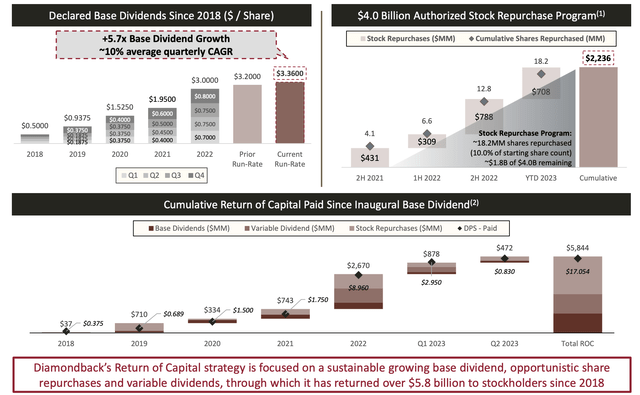

Protecting and growing its base dividend. After hiking its dividend by 5% on August 1, it now pays a base dividend of $0.84 per share per quarter, which translates to a yield of 2.2%.

Opportunistic share buybacks. Since the second half of 2021, the company has bought back $2.2 billion in stock, which translates to 8% of the current $28 billion market cap.

Variable/special dividends. The company aims to distribute 75% of its free cash flow. This means that at elevated oil prices, it will use special dividends to reward investors.

Since 2018, the company’s special dividends have roughly matched its base dividend. Buybacks were larger than both of these items. 2022 saw much higher special dividends than base dividends. Special dividends even exceeded buybacks, which is something I like, as I prefer special dividends.

Diamondback Energy

To give you an idea of how much FANG can distribute, it made the free cash flow sensitivity chart below.

Please note that FANG is now trading 7% higher compared to the date when data was collected for this chart. This means that expected returns at current levels are slightly lower. The market cap used for these calculations was measured on July 28.

Having said that, at $90 WTI, the company is able to generate $17.78 in FCF per share. This translates to an FCF yield of 11.5% using the CURRENT market cap/stock price.

75% of that is 8.6%.

In other words, at $90 WTI, investors can expect to get a total distribution yield of 8.6%. Even at $70 WTI, that number is still 6.7%!

Diamondback Energy

Furthermore, one of the reasons I’m buying energy on dips is the enhanced free cash flow. If investors were to buy FANG after a 10% decline, the distribution yield at $90 WTI would rise to 10%.

When combining everything I’ve said so far about FANG, we get very fertile ground for outperformance.

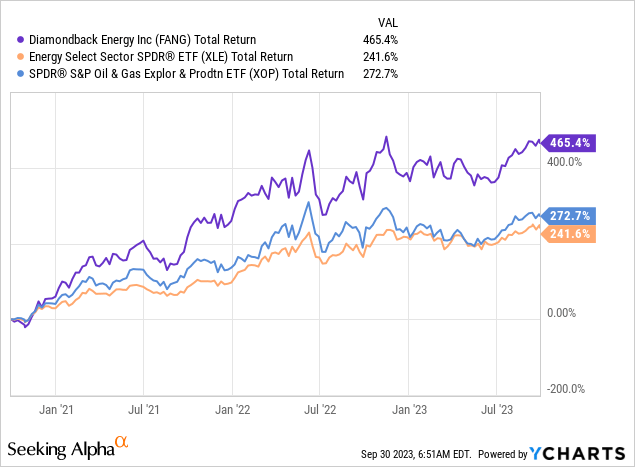

Over the past three years, FANG has returned close to 470%, including dividends. This has beaten the Energy ETF (XLE) and SPDR S&P Oil & Gas Exploration & Production ETF (XOP).

The company has been performing significantly better than its peers, partly due to the poor performance of shale companies before the pandemic. While I do not anticipate the company maintaining a consistent outperformance of nearly 200 points every three years, I do believe that it will continue to outperform its competitors for many years to come.

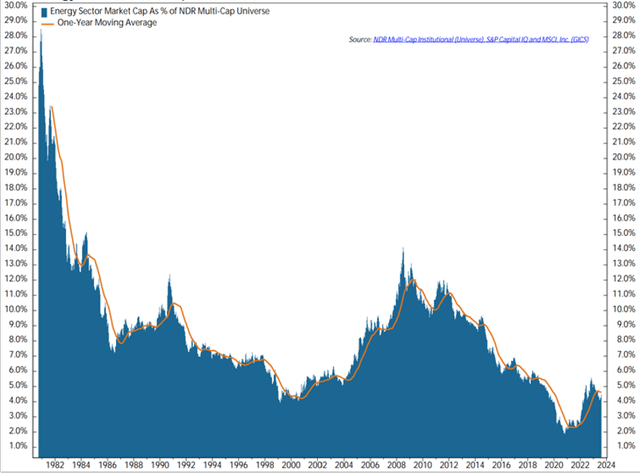

Valuation-wise, I believe that energy companies are attractively valued.

Not only is FANG in a great spot to distribute double-digit dividends and buybacks, but energy, in general, is still undervalued compared to the market.

Ned Davis Research

I believe that if the market starts to bet on an economic recovery and prolonged elevated energy prices, we could see a massive flow into energy, including FANG.

While it’s hard to put a price target on a stock that is highly correlated to a commodity, I expect FANG to deliver strong, double-digit annual returns for as long as we’re in this favorable energy market.

Hence, I continue to buy energy stocks on weakness. Right now, I’m preparing for a potential oil price decline to $80 if the economy keeps weakening. I have close to 20% energy exposure.

Takeaway

FANG has a major position in the Permian Basin, deep reserves, and efficient operations with low breakeven prices. Their BBB-rated balance sheet, low debt levels, and shareholder-friendly distribution plans make them a compelling choice for long-term oil exposure.

With the potential for oil prices to remain elevated, FANG offers an enticing combination of dividends, buybacks, and special dividends, presenting investors with the prospect of substantial returns.

In a market where energy remains undervalued, FANG’s outlook is bright, making it a top pick for those seeking strong returns and high income in the energy sector.