This is a segment from the 0xResearch newsletter. To read the full editions, subscribe.

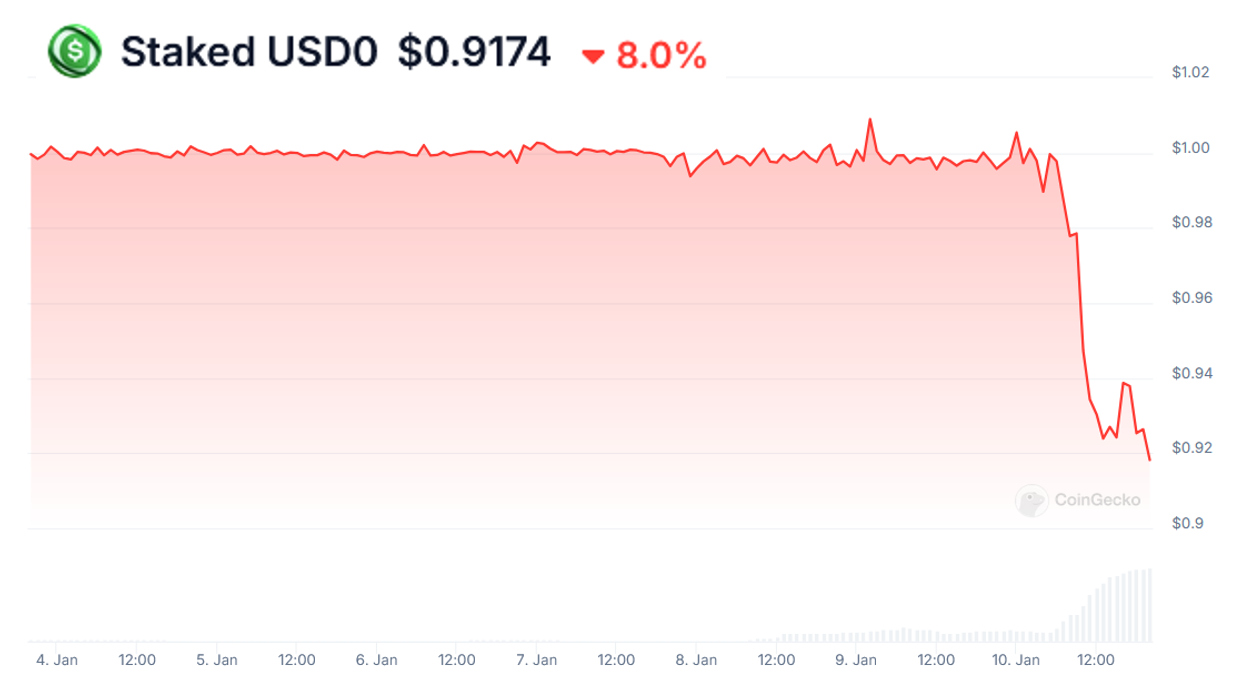

The usual protocol, the shiny new stablecoin on offer, sees its USD0++ “stablecoin” (a popular misconception) lose parity by USD0 as of 17 hours ago. It now trades at around $0.92.

But USD0++ is of course not a stablecoin. It is a liquid derivative of the USD0 stablecoin, a bit like Lido’s stETH compared to ETH. (The USD peg of USD0 is fine, and the underlying T-bills have no support problem.)

Usual’s business model is based on the idea of an “onchain Tether” that rewards users. By staking USD0 for USD0++, you will receive the underlying government bond yields and rewards in the protocol’s native token, USUAL.

Should USD0++ stakers change their mind before the expiration date, they can exit by forgoing rewards and reset their stake to USD0 at a 1:1 exchange rate. This first exit option will be available from next week.

This explains why the “depeg” between USD0 and USD0++ is not exactly an error. Consider USD0++ as a four-year bond. That bond should technically trade at a discounted interest rate to reflect a risk premium if you hold the bond for four years. Economists call this the ‘time value of money’.

Recall that in June 2022, Lido’s sETH also broke away from ETH amid financial issues surrounding the now-defunct Celsius.

Market panic led LPs to pull sETH liquidity from Curve pools, causing massive liquidity imbalances and a sETH:ETH depeg. Just as sETH does not necessarily have to trade at parity with ETH, USD0++ does not have to trade at parity with USD0.

However, what is causing the USD0++ haircut today is Usual’s announcement of an alternative exit option from USD0++ to USD0. The feature was spotted in a blog post published yesterday.

Based on updated documents, the new exit option would allow users to exchange USD0++ for USD0 at a manually set minimum price of 0.87 USD0 per USD0++, while retaining the rewards in USUAL issues (unlike the original 1:1 exit option).

Why $0.87? Because it is the discounted interest rate at fair value. As @mytwogweis from Treehouse Finance explains:

If you expect 4% annually over four years, the fair value of USD0++ today should be around $0.855. This means you buy it for $0.855, hold it for four years, and exchange it for $1 for a risk-free return of 4%.

Simply put, the new exit option more accurately reflects USD0++ for what it is: a long-term bond.

The problem is that Usual’s go-to-market strategy was already based on several assumptions.

Pendle PT-USD0++ farmers who entered into fixed return transactions are now suddenly discovering that they “overpaid” for a bond at face value (at maturity, 1 PT USD0++ is equal to 1 USD0++).

For example, the USD0++ Pendle pool (with an expiration date of January 30, 2025) sees a dump.

Source: Pendel

To make matters worse, vault operators in the Morpho loan markets have hardcoded prices in USD0++:USDC markets at a parity of 1:1, rather than basing assets on a free-floating market rate.

The result: Risk trustee Gauntlet and other LPs immediately reallocated the USD0++ vault inventory liquidity from Morpho vaults above the current market rate of $0.91 in anticipation of the news, sparking public rumors of insider trading.

In an email to Blockworks, Tarun Chitra, founder and CEO of Gauntlet, said of the company’s operations: “However, we were not aware of any prior notice as evidenced by the time stamp of these transactions (the Usual team updated their repayment documents before this). We wanted to ensure that our users were not exposed, and we automatically rebalanced out of the markets when risk or concentration limits were exceeded.”

MEV Capital issued a public statement denying that it received any inside information from Usual, although it did not say from whom the company received the information.

USUAL, the protocol’s native token, has settled -18.7% over the past 24 hours, as of 11:45 AM ET.

Macauley Peterson contributed reporting.