Last week, S&P Global admitted a “B-” publisher with a stable prospect of Sky-Protocol-Voorn known as a maker-a decentralized credit platform that the USDS Stablecoin issues.

The creditworthiness agency mentioned centralization problems, including a “high concentration of deposits”, “centralized administration”, “high regulatory risk of uncertainty about regulatory frameworks for decentralized protocols” and “weak risk-adjusted capitalization” in its decision.

In its rating report published on 7 August, S&P Global Ratings said that these risks are “partially compensated by the good track record of the protocol of limited credit losses since 2020 and modest income.” The report indicates that a better assessment “is very unlikely in the coming 12 months, and would require significant improvements in governance and capital position”, while a downward scenario can find out in liquidity, high loan losses or unfavorable regulatory movements.

When coming to the B-rating, the credit agency said it was the creditworthiness of Sky’s token obligations, including USDs, as well as his DAI Stablecoin rated, the protocol said that it will eventually be phased out during his rebrand and replaced by USDS. Other obligations include related savings, Suss or Sdai. In the report, the analysts assessed the risk that Sky is in default on the tokens, whereby a standard in this case is defined as a hairstyle – which means a reduction in value – for token holders.

The report of S&P Global noted that the most important risks that can lead to such a standard on its tokens, “recordings of the storage more than the available liquidity in the PEG stability module (currently held in USDC, a centralized Stablecain) and credit losses that would border the available capital.”

Important risks

Speaking of Sky Protocol, Andrew O’Neill, director and analytical lead for digital assets at S&P Global Ratings, The Defiant said that, after the general pace of change in Defi, the project undergoes “a period of significant change through his end game roadmap, which is undergoing his administration and capitalization. “

He said that S&P used data on chains and governance transparency to check the developments that are relevant to the assessment analysis.

O’Neill also explained that the analysis takes into account both the current board and the operational framework, as well as the strategic direction of the route map. Every major shift would cause an assessment. If a fork has been made to take the protocol in a new direction, he emphasized that “the existing rating only applies to the existing protocol.”

O’Neill told The Defiant that the assessments of S&P are assessed annually, and “on ad hocbasis when we observe developments that influence credit quality.”

Centralization concern

The S&P Global Report said that the Sky protocol board is effectively checked by co-founder Rune Christensen because of the low rise of voters, and warned of strategic disruption risks, despite the fact that Christensen owns only 9% of the drivers.

The analysis of S&P showed that the capital ratio of Sky from the end of July 0.4% at 0.4%, with 35% of the assets in Tokenized Real-World assets, namely American treasury drawings and USDC. The report noted that the SKY liquidity reserves, including tokenized money market funds, yielded a buffer, but could be tested in a run scenario.

Stablecoin reports

This was not the first trip of S&P in Crypto reviews. In December 2023 it launched a 1-5 rating of Stablecoin stability that looked at reserve quality, custody and market or credit risk, plus mitigants such as collateralization, silverness, liquidation rules and operational controls.

Under that framework, S&P at the time eight stablecoins: Sky’s DAI, First Digital USD (FDUSD), Legacy Frax Dollar (Frax), Gemini Dollar (GUSD), Pax Dollar (USDP), Tether (USDT) and CircleD (Tusd.

The market capitalization of Sky’s USDS Stablecoin – which was launched after these ratings were released in September 2024 – is currently at $ 7.9 billion, and ranks the fourth under Stablecoins, behind Tether’s USDT, Circle’s USDC and Ethena’s Usde.

At the time, Frax and Tusd received the weakest score – a 5, which defines the company as ‘weak’. S&P marked under collateralization, heavy dependence on collateral and uncertainty about future collateral plans.

Tether’s USDT was assessed on 4, or ‘limited’, for limited clarity about where and with whom reserves are held, investments in riskier assets and limits for direct repayment options. USDC, Gusd and USDP, on the other hand, scored 2, or ‘strong’, which show more clarity about reserve cake, including safer assets in the short term and more transparency, according to S&P Global.

It is unclear how S&P determines which stablecoins to assess, because it has not shared formal selection rules. Since the end of January, when it published a report on Ethena’s Usde, the creditworthiness agency has not issued a new Stablecoin-specific assessments.

When asked whether S&P had stopped assessing Stablecoins, O’Neill clarified in comments to the Defiant: “The most recent new stable stability evaluation we have assigned was indeed in January 2025, but we will continue to follow all 12 of the assessments we have published on a current basis.”

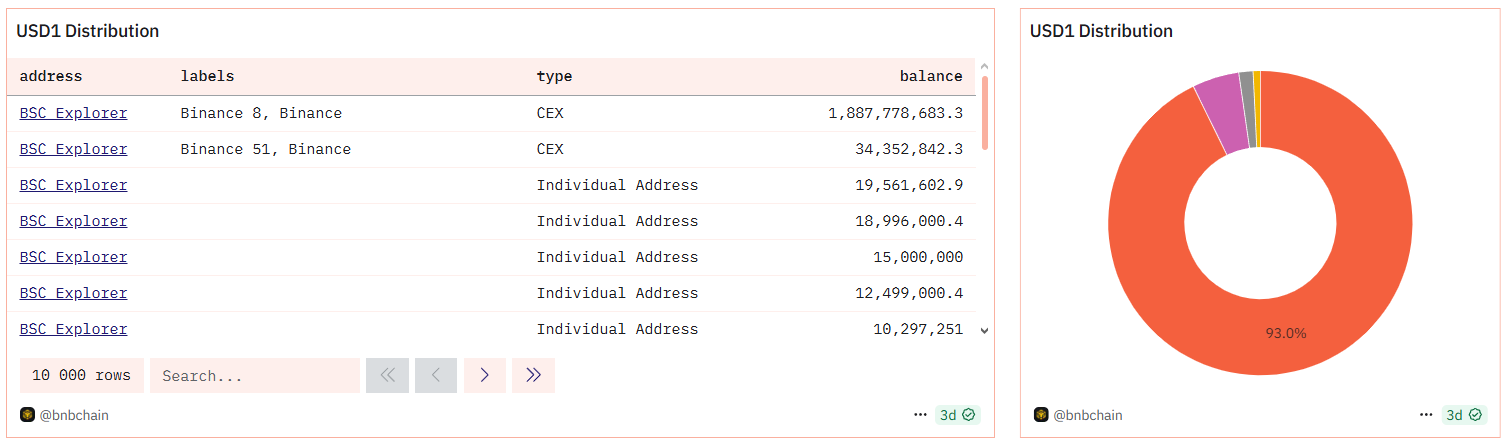

The break has left a number of relatively large stablecoines without an assessment. Under the Stablecoins still to be assessed, USD1 was, earlier this year, launched by World Liberty Financial, the Defi -company closely linked to President Donald Trump. USD1 is currently the seventh largest stablecoin per market capitalization, with around $ 2.2 billion at the time of the press.

USD1 distribution. Source: Dune Analytics

USD1 was launched on the BNB chain and has more than 90% of its stock on one stock market, which seems to be Binance according to data from Dune Analytics.

When asked for plans to assess new Stablecoins, including USD1, O’Neill said that the company “cannot comment on possible future publications of new assessments.”