This is a segment of the Lightspeed newsletter. Subscribe to read full editions.

The Solana Ecosystem is all about the appropriate Jupiter protocol, and with good reason.

They are an ambitious team that Damn Damn Damn tries to do in Defi.

In 2021, Jupiter launched a Dex -Aaggregator on Solana, the dominant location today for routing order flows to Dexs and Prop -amms. In addition to the aggregator, Jupiter Founder Meow also launched Mercurial Dex, today as Meteora.

A Perps Dex followed in 2023, then a Memecoin Launchpad in 2024, and then a majority purchase acquisition in the Moonshot Memecoin Trading Platform earlier this year. There is also the coming Omnichain network ‘Jupnet’, which is planning to collect liquidity between chains.

But all eyes this week are on Jupiter Lend, the first formal trip of the SuperApp in the vertical lending.

Tweet drawing ..

Jupiter’s credit product is built on the Fluid liquidity/risk motor. If you have never heard of liquid, it is a protocol that the Ethereum world stormed in the past year.

To see the promise of Jupiter Lend, a baseline comprehension of how liquid actually works. It is not the simplest product, but here is the core.

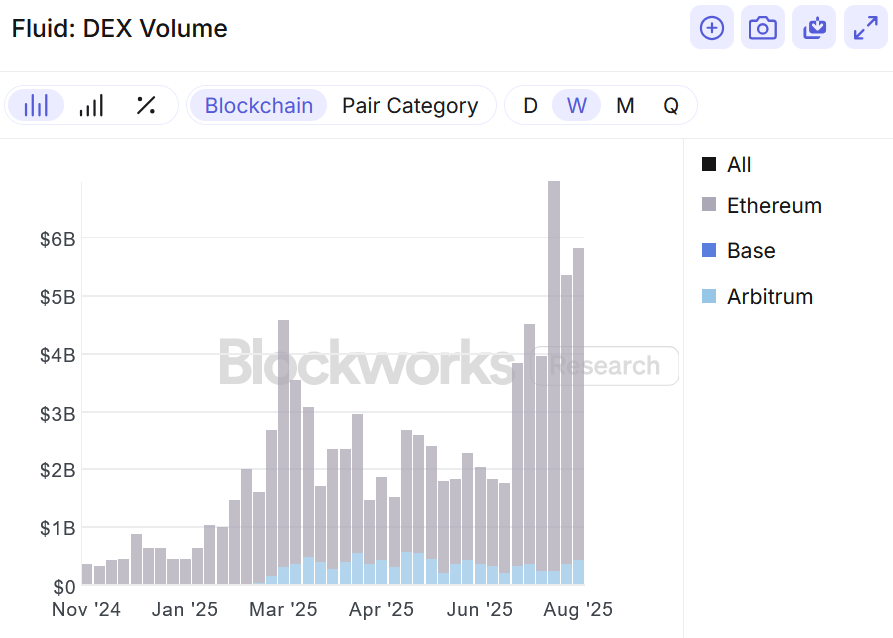

Liquid (formerly Instadapp) is an integrated application consisting of dex, loans and borrowing. All three wells from a uniform layer of liquidity, which makes unique functions possible that are simply not possible on other DEXs or loan protocols.

For example, a borrower on liquid can denominate their debt to serve as liquidity for Fluid Dex (which the team calls ‘smart debt’), instead of leaving it inactive as placed as collateral.

This actually sets the fault of a borrower to ‘work’. Since traders on the DEX side pay costs to act, borrowers can earn reimbursements to lower their debt. It is somewhat not -intuitive, because it reverses the logic of how we often regard debts as an unproductive active that must be paid.

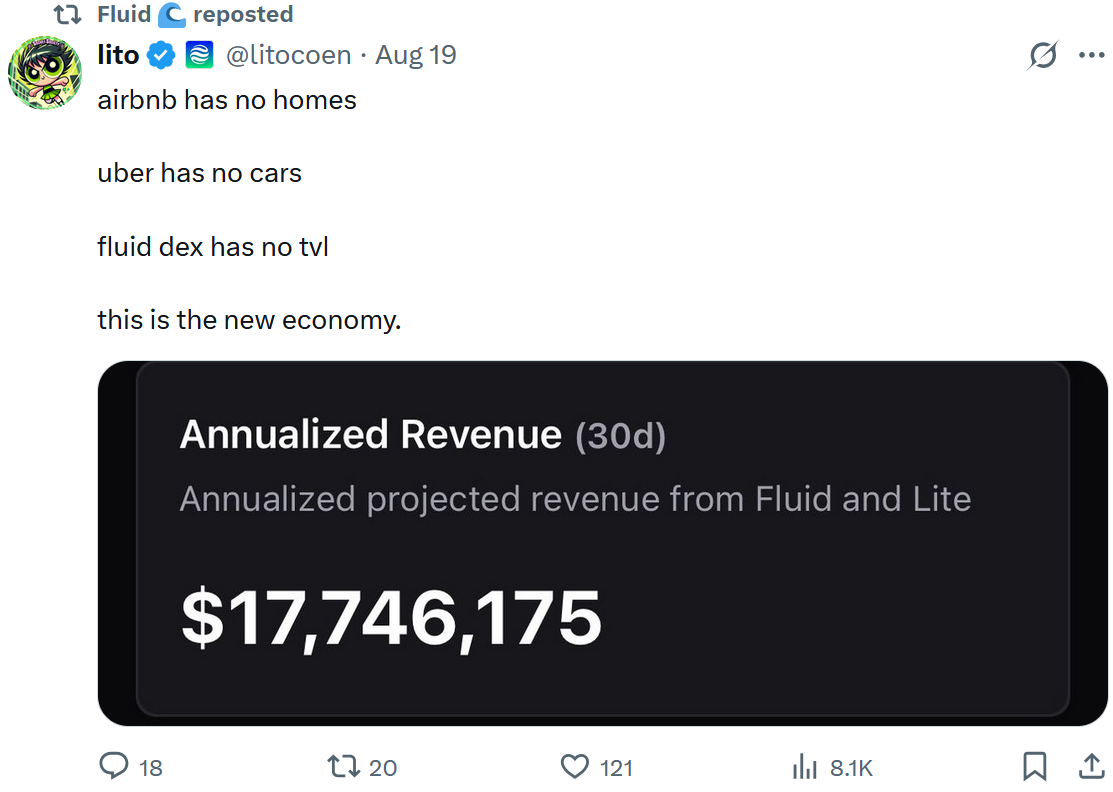

This is how fluid opens billions of dollars in “TVL” that is not really TVL, at least not in the conventional Defi sentence. What leads to memes like this:

Liquid may also have one of the most advanced liquidation engines in Defi. The loaning safes -bucket positions in “ticking”, which partially liquidates positions as the markets move, rather than fell into one.

Again, the tight integration of Fluid ensures that liquidations can easily settle as regular swaps on his own Dex.

This combination reduces drastic slip and punishments (~ 0.1%). And the end result is that the abnormally high loan value (LTV) makes relationships of 90-95% on its credit product. For context, even very liquid assets such as WBTC/Weth LTVs of 70-85% have on Aave.

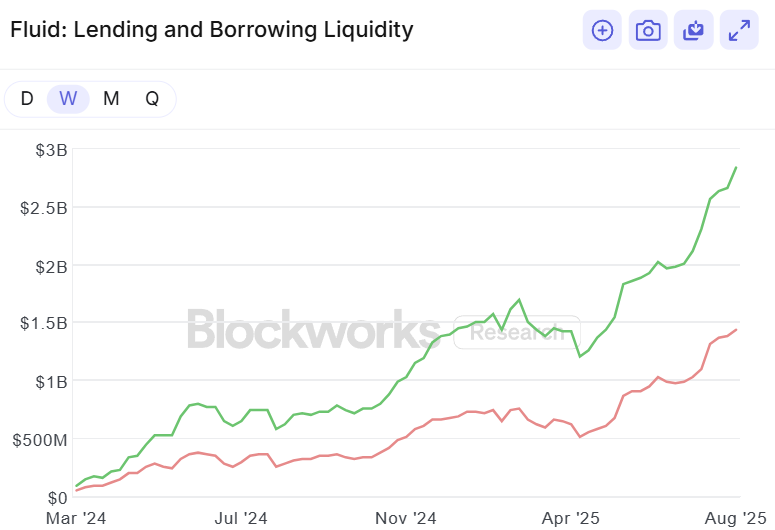

As a proof of Fluid’s success, the lending has $ 1.4 billion in active loans since the launch on Ethereum less than a year ago, according to research data from Blockworks.