The recent peak of Ethena in collateral images raises important questions about the loan question of Aave and the potential impact on Aave’s future performance.

-

The profession of Ethena PT draws Defi Capital because of its remarkable yields, so that the traditional credit model of Aave is immediately challenged.

-

Signs of weakness in Aave prices indicate a fading bullish momentum in the midst of rising competition.

Ethena [ENA] Principal Tokens (PT), part of the innovative return-bearing Stablecoin system from Ethena Labs, have surpassed $ 1 billion in collateral in just one month. This impressive growth corresponds to their recent approval as collateral on an Aave, which effectively improves the usefulness of Ethena in the Defi -credit landscape.

For those who are unknown, PTs benefit from Delta-neutral strategies that produce considerably real returns, usually between 15-25% on Susde. In a climate where conventional Defi-credit rates remain low, these offers emerged as very attractive options for return-seeking investors.

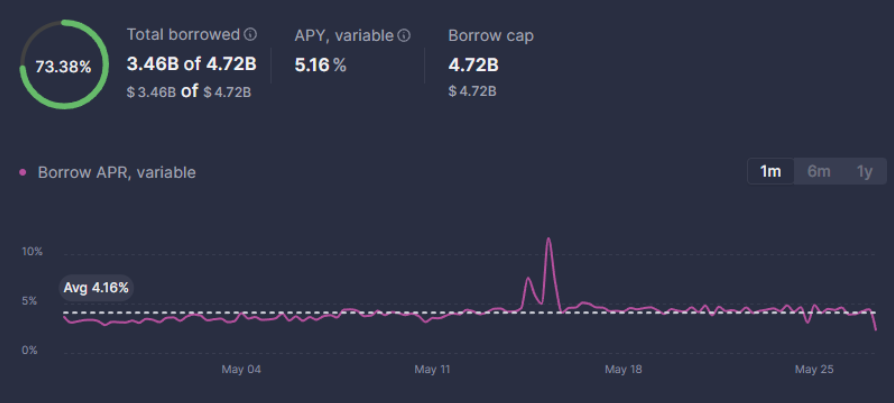

Aave’s falling loan interest: a relevant trend

In stark contrast, Aave has experienced a consistent decrease in loan rental rates. Currently, Stablecoin loan float between 2-4%, which is less attractive for lenders who strive for a higher return.

This decline can mean a wider trend: decreasing demand for leverage on chains and saturation of capital in the market. Interestingly, the rapid growth of Ethena could accelerate this trend, because the capital is increasingly being redirected to Susde instead of resting within Aave’s loan pools.