A growing coalition of decentralized finance advocates is pushing for a new proposal that they say could help ease the financial burden faced by low-income households worldwide.

The initiative, backed by the DeFi Education Fund (DEF) and several influential crypto policy groups, argues that decentralized financial instruments could save people up to $30 billion a year in fees, money currently lost to what researchers describe as the “poverty premium.”

How long can the poor afford an expensive financial system?

The renewed momentum comes as global poverty rates remain stubbornly high. In 2025, a estimated According to updated global estimates, 808 million people live in extreme poverty on less than $3 a day.

An additional 887 million people are believed to live in multidimensional poverty. Many of these households face overlapping pressures, including climate-related disasters, political instability and increasing economic vulnerability.

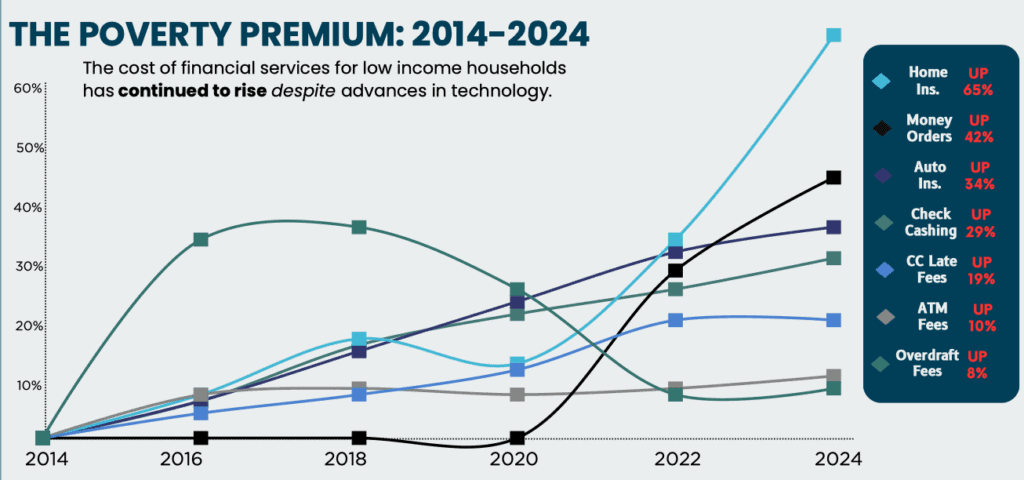

The DeFi Education Fund says the financial system itself is part of the problem. In new research published this year, the group highlighted the long-standing cost gap between rich and poor households in the United States.

About 5.6 million American households remain unbanked, and another 14.2% are unbanked, often forced to rely on expensive financial alternatives.

Collecting a paycheck can cost up to 5% of its value, and the cost eats up an average of 7.1% of annual income for low-income families, compared to just 0.2% for wealthier households.

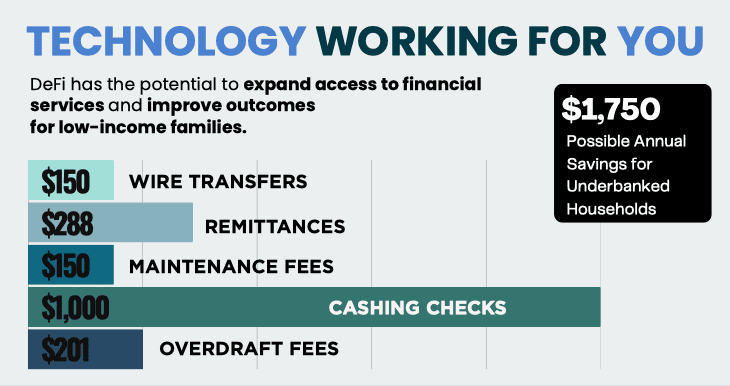

These costs are increasing. DEF argues that removing middlemen through decentralized finance rails could dramatically reduce basic expenses such as remittances, money transfers and bill payments.

One estimate in the group’s proposal suggests that DeFi infrastructure could reduce global money transfer costs by as much as 80%, potentially saving the world’s unbanked population $30 billion per year.

The initiative comes at a time when Americans appear increasingly open to alternatives. A DEF survey conducted with Ipsos found that 42% of Americans would likely try DeFi services if new legislation is passed clarifying crypto privacy protections.

Many respondents expressed frustrations about bank delays, unexpected fees and problems accessing their own money. In the sample, 56% of adults said they want full control over their money, and 54% said they want control over their financial data.

As DeFi’s role in the real world grows, DEF is accelerating its advocacy in Washington

In addition to its economic arguments, the DeFi Education Fund (DEF) has expanded its policy efforts in Washington.

In August, the organization launched the DeFi Education Foundation, a nonprofit designed to broaden its advocacy and deepen engagement with lawmakers.

Around the same period, DEF and Andreessen Horowitz (a16z) urged the U.S. Securities and Exchange Commission to create a regulatory “safe harbor” for blockchain applications.

They argued that neutral software interfaces should not be classified as brokers, warning that current interpretations risk forcing developers into unintended regulatory roles and discouraging innovation.

DEF also submitted a formal response to the Senate Banking Committee’s draft Responsible Financial Innovation Act of 2025.

In that filing, DEF and several major crypto companies, including Paradigm, Jump Crypto, Multicoin Capital, the Solana Policy Institute and the Uniswap Foundation, called for a clear regulatory separation between software builders and financial intermediaries.

@fund_defi has called on the US Senate Banking Committee to take a more measured approach to DeFi regulation.#Regulation #DeFihttps://t.co/9pZzvG6gkV

— Cryptonews.com (@cryptonews) August 2, 2025

As the debate over the long-term value of DeFi continues, proponents point to practical examples of how digital tools can increase access to financial services.

In Nigeria and parts of East Africa, crypto-based networks allow users to transact with or without smartphones.

In regions experiencing conflict or hyperinflation, including Venezuela, Zimbabwe and Argentina, digital currencies are used to move money and safeguard savings.

Some humanitarian groups have adopted blockchain systems to distribute aid with greater transparency.

Still, researchers note that DeFi faces limits. Collateral-heavy lending models, volatile token markets, smart contract vulnerabilities, and financial literacy barriers have slowed broader adoption.

Much of the current activity is still concentrated in speculative trading rather than real-world economic use. Even in El Salvador, where Bitcoin became legal tender in 2021, daily usage fell below expectations.

DEF argues that policymakers should protect the aspects of DeFi that directly reduce costs for consumers.

The group argues that open access, low-cost settlement and user control remain essential to reaching people living on the financial margins.

The post DeFi Advocates Propose $30 Billion Plan to Fight Global Poverty – Here’s the Plan appeared first on Cryptonews.