Low 1 Blockchain Sonic, previously known as Fantom, struggles with a steep fall in the total value locked in his ecosystem, causing questions about the sustainability of his growth strategy.

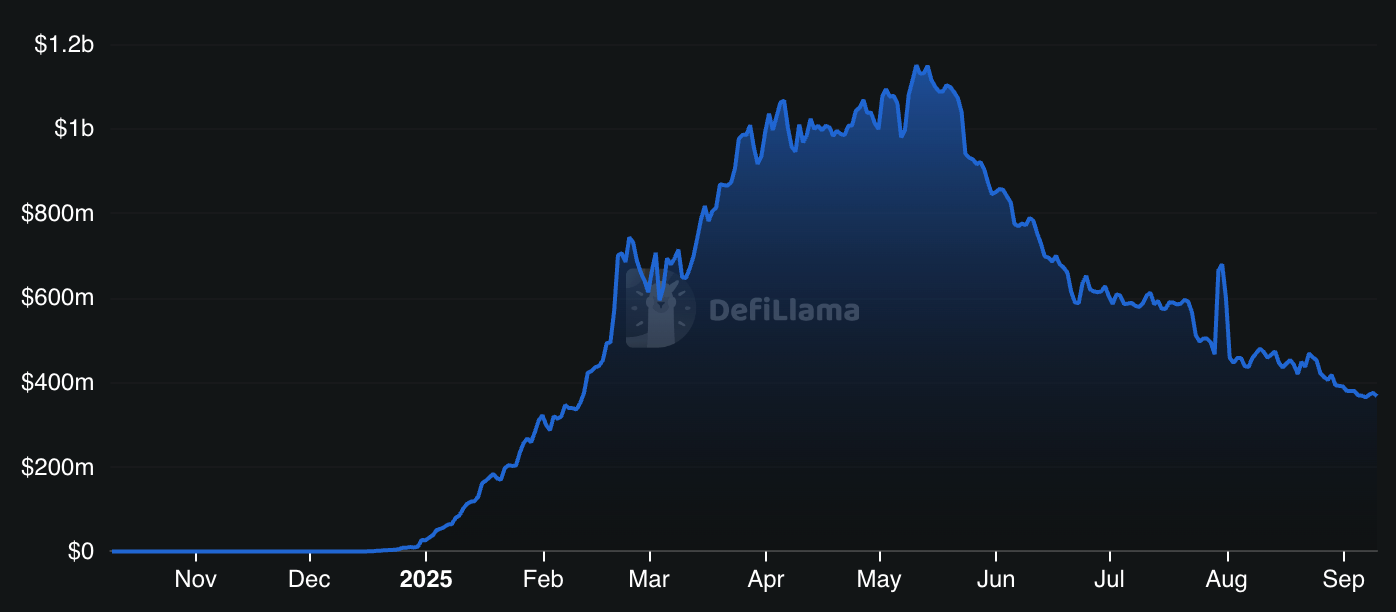

Sonic’s TVL has fallen from $ 1.1 billion in May to $ 367 million from today, a decrease of around 67%, according to Defillama. For the context, Fantom had reached a TVL height of around $ 9 billion earlier in the early 2022.

Sonic TVL

The drop coincided with the end of Sonic’s 5-year-old deal with market maker Wintermute, which underlines how difficult it can be for new block chains to keep users and funds active on their networks. At the time, Sonic’s Chief Strategy Officer wrote on X: “This is what we need for our ecosystem projects to thrive. CEX support is simply no longer enough.”

Sonic CEO Michael Kong said in reactions shared with the Defiant that although TVL is an important statistics, “it doesn’t always tell the whole story.” He added that Sonic wants to reach to reach the same TVL as Fantom ever had.

“Given the volatile nature of crypto, it is obvious that TVLs fluctuate over time,” said Kong. “We are also laser -oriented on building institutional scale, with plans to create a US ETF and a Nasdaq [digital asset treasury]. “

Earlier this month, Sonic approved a proposal to form Sonic USA, which will use $ 150 million in S -Tokens to finance an ETF and that.

‘Dual sword’

However, other experts say that the network is confronted with strategic choices. “Sonic TVL has fallen almost 70% since May, largely because they end their market agreement with winter mute,” said Mike Maloney, CEO and founder of Incyt. “New [Layer 1s] Looking for Defi cannot compete with the organic volume of Ethereum (and Solana) and must bring the ‘lead’ of makers of the private market. “

Ethereum is currently the world’s largest blockchain from TVL in Decentralized Finance (Defi), with almost $ 110 billion currently deposited in Ethereum-based protocols, according to Defillama. In the meantime, Solana has a TVL of $ 14 billion.

Maloney called it a ‘double -edged sword’, and noted that although market makers bring more volume and tighter spreads, they also record reimbursements that would otherwise go to users and ‘remove large parts of liquidity and transaction volume after their term has been terminated’.

“Sonic is now at a crossroads and has to make a difficult choice: trust professional market makers to create an efficient market, or suffer through the misery of adoption with long tail to create something really decentralized,” concluded Maloney.

‘Proceeds seekers are mercenaries’

In the meantime, Brian Huang, co-founder and CEO of Glider, emphasized the challenge to rely on revenue-controlled capital.

“Proceeds seekers are mercenaries. We have seen this time and again, where a new chain (although Sonic was a rebrand) launches heavy stimuli, but fails to maintain one of those TVL when the stimuli ran out. When the stimuli have disappeared, the returns, the returns, capital, Huang said.

He noted that the Sonic changes are closely tailored to the price of its native token, $ S, currently traded at $ 0.30, a decrease of approximately 69% compared to the launch price of $ 0.98 earlier this year, according to the Pricelage of the Defiant.

“Sonic paid incentives with the $ S -Token – for example, earns an extra 10% APY in $ S on deposits,” Huang explained. “As the price of $ S drops, however, that 10% APY starts more at 5% APY and then 2% APY.”

He noted that this return no longer makes it attractive. At the same time, people who sell $ S rewards they receive, which pushes the price of the token even further.

“TVL is only useful if you have borrowers who can generate that proceeds for lenders,” said Huang. “We will have to see whether Sonic can stimulate more loans in his ecosystem instead of just relying on ephemer stimuli.”