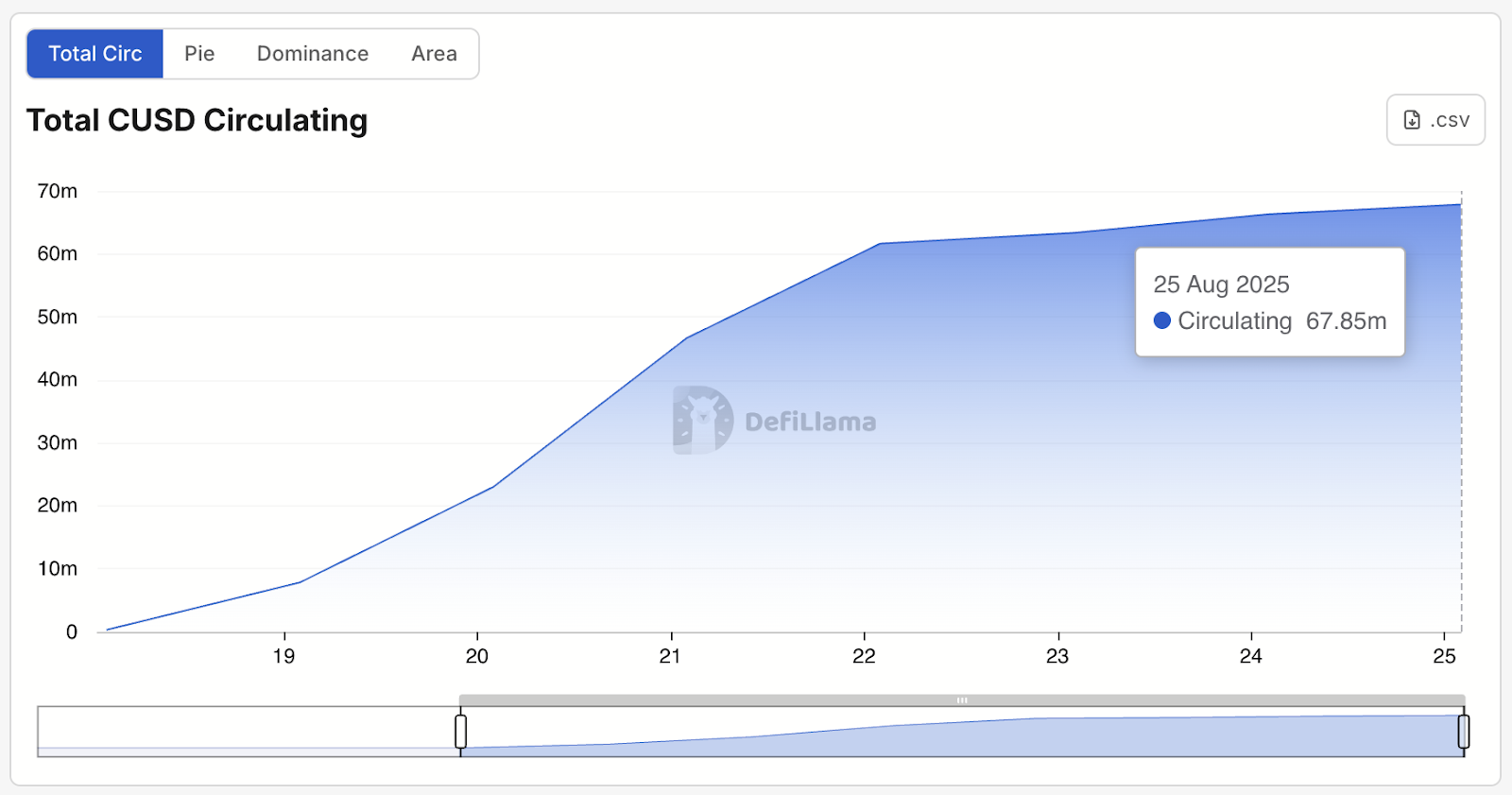

The new Stablecoin CUSD from Cap Labs has seen rapid adoption since the launch and, according to Defillama, climbs to $ 67.85 million in circulation last week.

Etherscan has so far shown 2,735 holders of token. The jump gives a strong demand for CAP’s yield-layered digital dollar model, which combines regulated reserve activa with self-layer-driven credit insurance policies.

CUSD is built on top of the newly launched Cap Stablecoin Network (CSN) and is designed as a 1: 1-insert stablecoin supported by assets such as Pypal’s Pyusd, BlackRock-managed Buidl and Franklin Templeton’s Benji. The proceeds-bearing version STCUSD-slammed by using CUSD made possible by a threefold system of money lenders, operators and restakers.

CAP’s core innovation lies in its structure: Operators borrow Stablecoins to use return strategies, Restakers endorses the credit risk of the operator and money lenders (STCUSD holders) earn a floating efficiency, currently around 12%, depending on the market demand and operator performance. While Restaker Collateral offers protection against the standard of operator, STCUSD holders are still exposed to fluctuating efficiency dynamics.

Cusd’s impressive growth; Source: Defillama

Cusd’s impressive growth; Source: Defillama

In contrast to much past, Stablecoin launches, the CAP model is carefully coordinated to comply with the Genius Act, the sweeping American stablecoin legislation that prohibits interest rates. Speaking at the Stablecoin -top in Cannes in June, was the founder of Cap Labs Benjamin Lens Bot:

“They said no yield, and it is pretty clear – there is no way around it. They don’t want Stablecoins to give retail investors,” Lens said.

STCUSD is therefore a separate ERC-4626 Vault token that users can mine by using CUSD. The yield is generated via a marketplace of borrowing and recovering, not directly from Cap -Laboratories.

“Genius Act includes companies that generate returns on behalf of users and give them to users,” said Lens in Cannes, while Cap “is an unchanged open protocol such as Ethereum, such as Bitcoin.”

Combined with the fact that the percentage of a stablecoin -support -scusd is limited to 40%, Lens thinks they have a conform of mechanism. “This is the standard that we have agreed with Templeton and BlackRock for our integration with them,” Lens Blockworks told and noted that it is the same arrangement that USTB (from Ethena) made in collaboration with BlackRock.

Restring evolution

Cap’s design corresponds to a trend that comes up on your own layer: the financialization of actively validated services (AVSS). Traditionally, AVSS offered infrastructure services – such as oracles or bridges – with risks limited to uptime or correctness. But a new wave of AVSS uses self -layer to endorse financial guarantees.

CAP is an example marked by Zoetlaerer founder Sereeram Kannan. “A striker can use and promise an operator [like Susquehanna] Is going to make Apr 10, “Kannan told Blockworks.” You can endorse the financial risk with Owlayer, which is a whole new type of risk, that requires much, much more active curation and monitoring, “he said.

What makes this possible is the recent rollout of a new position of self -layer, complementary to Slashing, who went live in April.

Although Slashing enables Restakers to be punished for supporting sub -performing operators, redistribution, being launched at the end of July, cut -cut funds to be diverted to the affected AVS – such as Cap’s Lending Vault – instead of burned.

That change turns self -layer into a programmable risk distribution layer, which is able to maintain structured financing contracts completely onchain.

“With financial AVSS, Slashing is the core logic,” said Kannan. “A liquidation is an example – if the obstacle that is not paid is not met – switch and move the money.” That is easier than cutting some infrastructure -AVSS, such as a ZK or T -shirtcoprocessor, where it is more difficult to adequately express the oblique logic onchain, he added.

According to a research memorandum from Serenity Research and Catalysis published on Sunday, the CAP model looks like a CDS-like structure: Restakers Drawing Off-Chain Legal Agreements to cover the standard values of the operator, post-underpand Onchain and are liquidated if their guarantee fails. CAP currently mentions market makers such as Fasanara, GSR and Amber as operators, with Gauntlet and Symbiotic Restakers that offer credit protection.