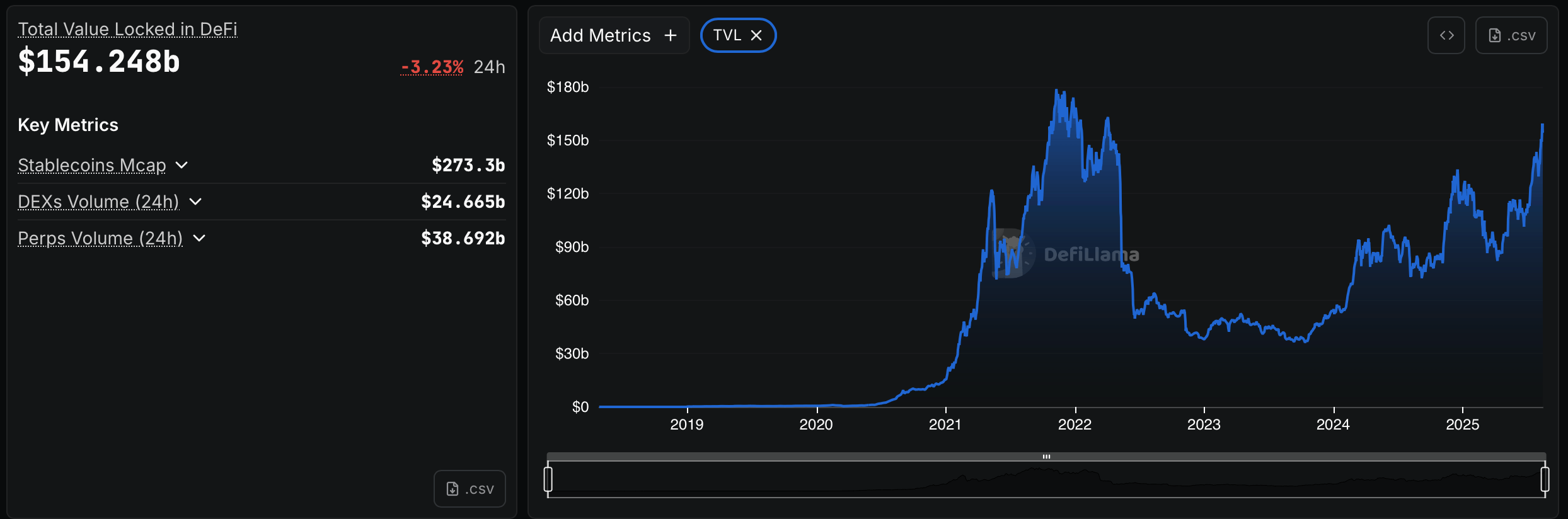

The total value of the decentralized financing (Defi) sector has climbed to $ 154,248 billion, with liquid Stakgigant -Lido and credit platform Aave with dominant positions maintained.

Lido, Aave takes top spots while Defi TVL $ 150 billion surpasses

Data from Defillama.com shows that TV has fallen 3.23% in the last 24 hours, but the figure remains well above the threshold of $ 150 billion, with the scale of the sector. Stablecoins in Omloop have a combined market capitalization of $ 273.3 billion, with decentralized Exchange (DEX) platforms that handle $ 24,665 billion in daily trade volume. Perpetuals -markets processed $ 38.692 billion in the same period, while network participants paid $ 121.27 million in transaction costs.

Source: Defillama.com

Lido leads all protocols by $ 40,065 billion locked over five chains, mainly through its liquid reinforcement services for Ethereum and other proof-of-stake assets. Aave follows closely with $ 38.018 billion in assets spread over 17 chains, which confirms its role as the cornerstone of Defi -credit and loan markets. Owlayer, a repeated protocol, is in third place with a locked $ 21,116 billion, which emphasizes the rising fame of repeated mechanisms in the Defi Ecosystem.

Other major players include Binance’s Stutet ETH offer ($ 14,551 billion), Ether.fi ($ 12,109 billion) and Ethena ($ 11,147 billion). The Pendle revenue protocol has $ 8.681 billion in ten chains, while Spark, Sky and Morpho control every check between $ 6.3 billion and $ 8.3 billion in assets. Uniswap remains the best DEX protocol, with $ 6,234 billion locked over 38 chains.

The current TVL is near historical highlights, as can be seen on long-term graphs, which show a recovery of the sharp drawings of 2022 and early 2023. Defi has since entered a renewed growth phase, with steady intake that push TV levels close to their peak levels from the end of 2021.

Daily Dex -Handelsvolumes have been consistently increased, with recent activity that is trending to the higher end of the monthly range. Distribution data of the reimbursement indicate a concentration of income under the largest Defi protocols, with Lido, Uniswap and various stablecoin emissioners who lead the reimbursement for generating the reimbursement.

The combination of high TVL, significant stablecoin -readiness and consistent transaction costs emphasizes the continuous integration of Defi in the broader market for digital assets and traditional finances (Tradfi). With protocols such as Lido and Aave anchoring the sector, the competition for liquidity and user activity remains intense about deployment, loan and revenue generation platforms.

While Defi approaches new TVL records, protocol innovation and expansion of cross-chain seem to be important motives of growth, even in the midst of daily market fluctuations.