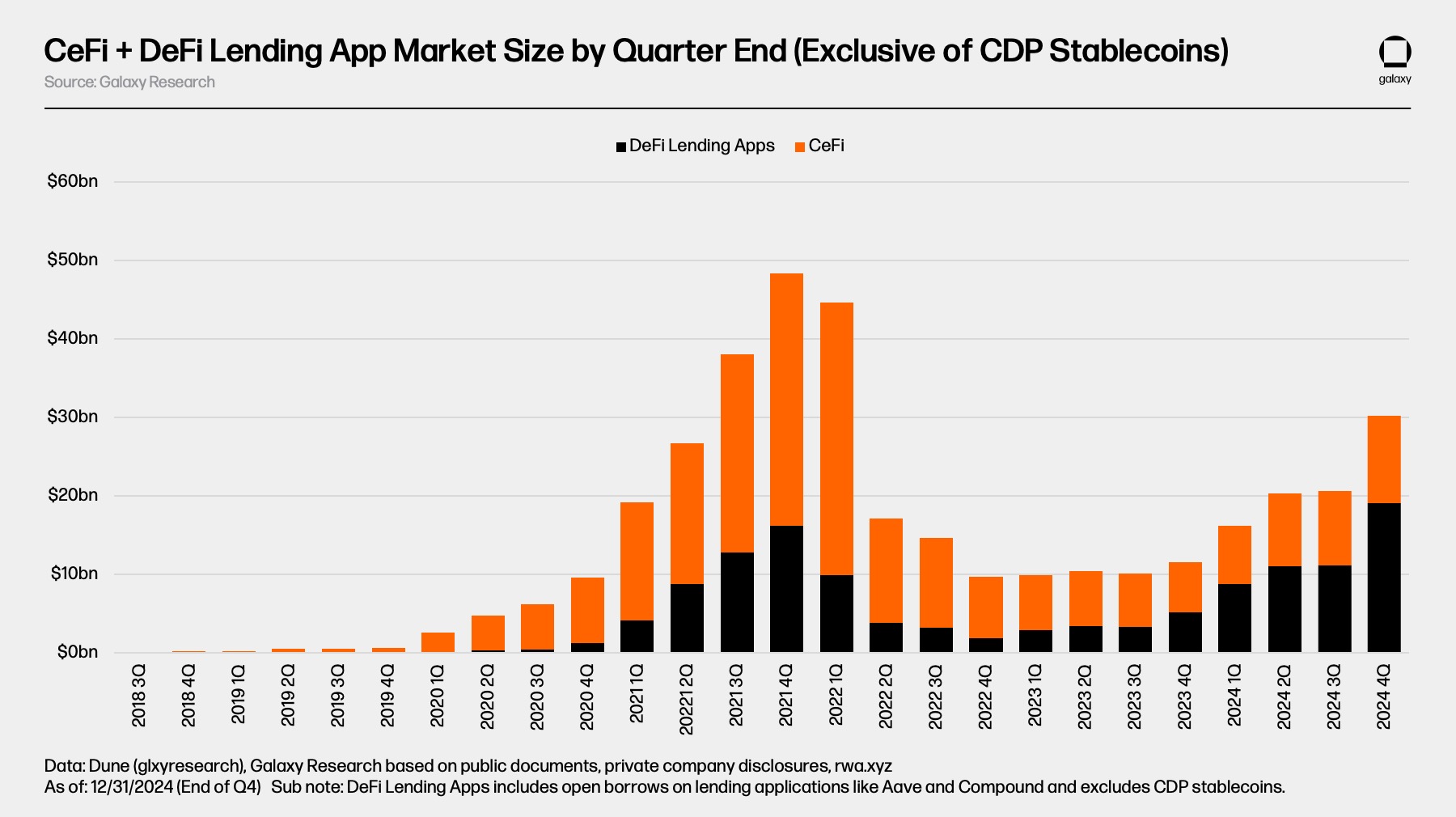

The crypto-credit market has fallen from its peak from the Bullmarkt and has fallen 43% from its highest to $ 36.5 billion in Q4 2024, according to a new report from Galaxy Research.

The decline came from the collapse of large credit platforms during the Berenmarkt from 2022-2023. Despite this overall contraction, the market recovered 157% compared to the quarter of $ 14.2 billion of Q3 2023.

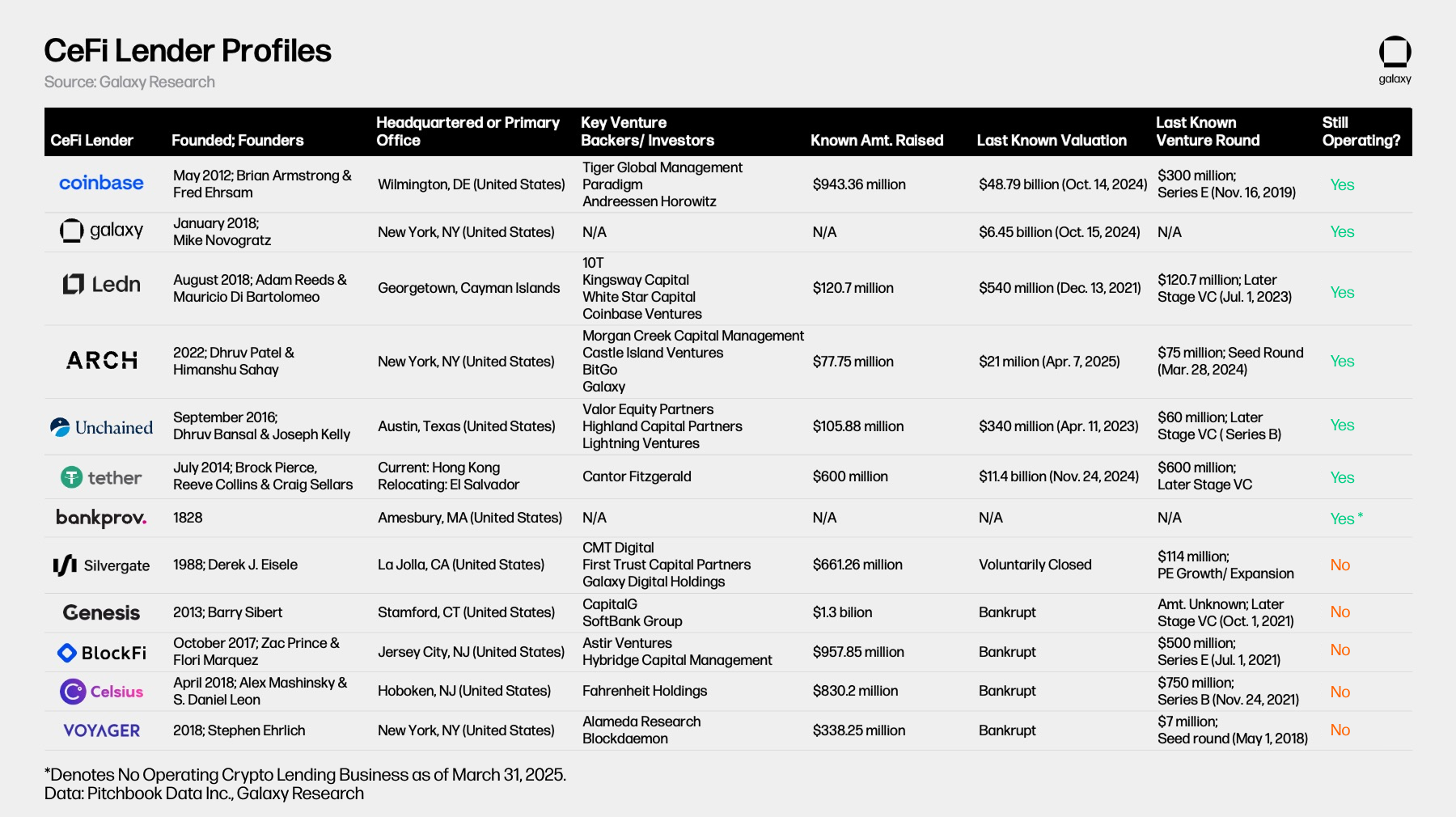

CEFI -Credit Lenders Consolidate after Market Inval

The CEFI credit market saw enormous disruption after bankruptcies of dominant players. The Cefi Crypto Lending Market peaked on an estimated $ 34.8 billion in outstanding loans before it dropped to $ 6.4 billion at the lowest point – a decrease of 82%.

Against Q4 2024, the CEFI credit market is mid-$ 11.2 billion, 68% below the all time high but 73% higher than the Bear Market low. The rebound is accompanied by a greater concentration for fewer players.

The three largest CEFI lenders – LEDN, Galaxy and Tether – now dominate the market with a combined loan book value of $ 9.9 billion and a combined market share of 89%. This is a shift from the Q1 2022 Bull Market Top when the top three lenders (Genesis, Blockfi and Celsius) had 76% market share with $ 26.4 billion in loans.

Source: Galaxy Report.

The failure of these market leaders has changed the competitive landscape. Genesis, Celsius Network, Blockfi and Voyager all went bankrupt within a period of two years as the crypto-asset prices fell and the market liquidity evaporated.

Not all CEFI money shooters are the same, implies the Galaxy report. Some only offer specific types of loans, eg BTC-collateral products or cash loans minus stablecoins. Some offer their services to only specific types of customers or jurisdictions. With this heterogeneity, some lenders can become larger than others.

The report notes that potential double seconds between CEFI loan book size and Defi loans, since some CEFI entities use Defi-lending to service pressures to off-chain customers.

Defi -loan shows strong recovery

Defi loans through applications on the chain have brought strong growth in the soil of the Bear Market. There were $ 19.1 billion in open loans in 20 crypto credit applications and 12 block chains at the end of Q4 2024. This marks an increase of 959% in Open Defi loans over eight quarters since the soil was set.

From the Q4 2024 moment recording, the amount of outstanding loans by means of borrowing applications was 18% higher than the earlier peak of $ 16.2 billion during the Bull market of 2020-2021.

The borrowing of Defi has recovered stronger than CEFI loans. This can be attributed to the permissionless nature of Blockchain -based applications and the survival of borrowing applications via the Berenmarkt. In contrast to the largest CEFI lenders who went bankrupt, the most important loan applications continued to function during the recession.

According to the Galaxy report, this result emphasizes the strength of the design and risk management practices of large loan apps on chains and the benefits of algorithmic, overcollateral and demand/demand-based loans.

An important development in the Crypto credit market is the growing dominance of Defi -Lending Apps about CEFI locations. The share of Defi Lending Applications in the total emptiness of cryptocurrency (excluding CDP Stablecoins) only reached 34% during the bull’s cycle of 2020-2021. From Q4 2024 it is 63% of the market, which almost doubles its dominance.

The trend is more pronounced when they record CDP-StableCoins supported by Crypto. At the end of Q4 2024, Defi -Lenen -Apps and CDP Stablecoins conquered a combined 69% of the entire market.

The report notes that a decreasing dominance of CDP-StableCoins as a source of crypto-collateral leverage, partly due to the increased liquidity of stablecoins, improved parameters on credit applications and the introduction of Delta Neutral Stablecoins such as Ethena.

Venture capital financing slows down for the credit sector

CEFI and Defi-Loanen- and Credit applications raised a combined $ 1.63 billion by deals with known amounts between Q1 2022 and Q4 2024 over 89 deals. The sector saw its highest quarterfish finance in Q2 2022. It received $ 502 million in eight deals. The lowest point came in Q4 2023 with only $ 2.2 million in total financing.

Venture capital allocation to loans and credit applications has only made up for a small part of the total VC investments in the crypto economy. On average, the lending and credit applications only conquered 2.8% of all VC capital assigned to the space on a quarterly basis between Q1 2022 and Q4 2024.

The share of the crypto credit sector of the total quarterly financing reached a peak at 9.75% in Q4 2022. At Q4 2024, however, it fell to only 0.62% of the total crypto VC financing.

The Galaxy Report connects this decrease in financing with the market deposits of 2022-2023 in which large players such as Blockfi, Celsius, Genesis and Voyager have submitted bankruptcy. These four entities alone accounted for 40% of the entire crypto credit market and 82% of the CEFI credit market on their peak.

According to the report, the downfall of these lenders came mainly from the implosion of the general crypto market. However, it was exacerbated by maladministration of risks and acceptance of toxic collateral from borrowers.