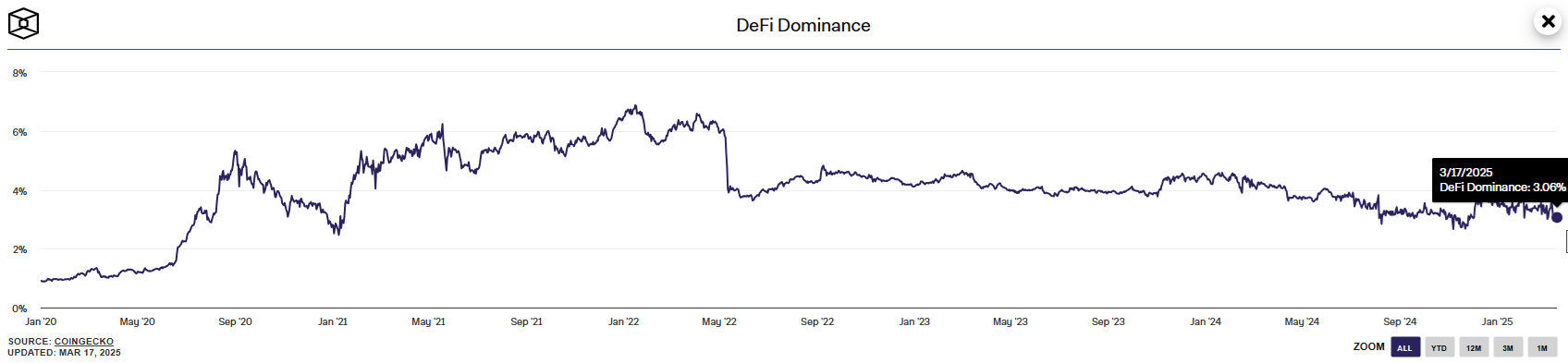

Defi -assets and locked value show Bearish signals, despite the recent recovery from the cryptomarket. Defi Dominance, a metric of the performance of Defi -Tokens, has fallen to levels that are no longer seen since the Bullmarkt 2021.

Defi -Tokens remain in their performance and reach the lowest dominant levels since the beginning of 2021. The Defi -Dominance has fallen to 3%, before the 2021 rally for Dex and Loan projects. During this market cycle Defi -Dominance had a small increase, up to 3.71%, far from the values of about 5.9% during the bull cycle of 2021. In 2024 Defi was widely used, but this was not immediately reflected in token prices.

Defi -Dominance fell to around 3%, a level that is no longer seen since before the Bull market of 2021. | Source: Theblock -data

Even top tokens such as Uniswap (Uni) and Aave (Aave) have not fulfilled their expected meetings. The current low dominance can be seen as a shopping option, but the market continues to stagnate, without signs of recovery after months of sideways trade.

The low performance of Defi -Tokens follows the overall weakness of all altcoins, because Bitcoin (BTC) has included the majority of liquidity. Defi -tokens are also not used that much for their usefulness or safety, because the sector is dependent on Stablecoins, BTC and Ethereum (ETH) collateral.

The total value locked in Defi also decreased to $ 90 billionLevels that are no longer seen since 2021. Traders will notice the downward shift in TVL, with a general Bearish Trend. Lending has also locked a sharp decline in value, to $ 39 billion From a recent peak of $ 51 billion.

Defi -Tokens acting near their lower reach, although traders remain careful in expecting a bouncy. The interest in Altcoins remains almost profound deep and Defi is no exception. Even leaders like Aave acted weakly, at around $ 176.90. The expectations for Aave were for a walk up to $ 400 or higher, based on the recent growth of loans.

The sector usually suffered from the reduced price of Ethereum (ETH) and cuts the value of collateral. Defi is seen as a proxy for the bullmarkt and shows trust in constant appreciation. Most protocols rely on a bullmarkt to reach the desired yields or to resort to restructuring their loans and interest rates.

Defi responds to the delay of the market

Defi has responded to several market cycles and revived after the Bull market from 2022-2023. However, TVL has never been restored to the peak of 2021. Most of the liquidity has moved to an Aave and Sky protocol, with similar apps on Solana and other networks. Defi was one of the tools to tap the value of altcoins, which were sometimes accepted as collateral.

Lending and yield of agriculture remain risky, although it has been used to tap and live value by keeping stablecoins. Despite the record Stablecoin offer of more than 227 billion tokens, Defi shows signs of delay. Synthetic assets also reduces their offer as a response to Bearish market conditions.

The current list of Defi -Tokens contains different stories. Dex -Tokens perform differently, compared to loan assets. As a whole, the appreciation of the sector fell to $ 88.5bWith more than $ 6 billion a total of 24-hour volume.

The attitudes of the Berenmarkt and the delay of ETH have the most influence on the loans and delivering the most of agriculture. Supporting liquidity savings remain risky, despite the high yields. Recently, liquidity providers on the Hyperliquid market had a loss of $ 4 million after the liquidation of a large ETH short position.

Different tokens stand out for their usefulness or expectations for growth. RWA is also included as a subset of Defi, with growth from Ondo Finance (ONDO) and Mantra (OM). Ethena (ENA) recently announced that it would be running to provide L1 services for a special settlement chain for traditional finances.

The Defi sector also added activity and liquidity of the newly connected hyperliquid (hype). The decentralized perpetual futures market is widely used during periods of market turbulence, whereby whales take risky positions with a maximum of 40x leverage.