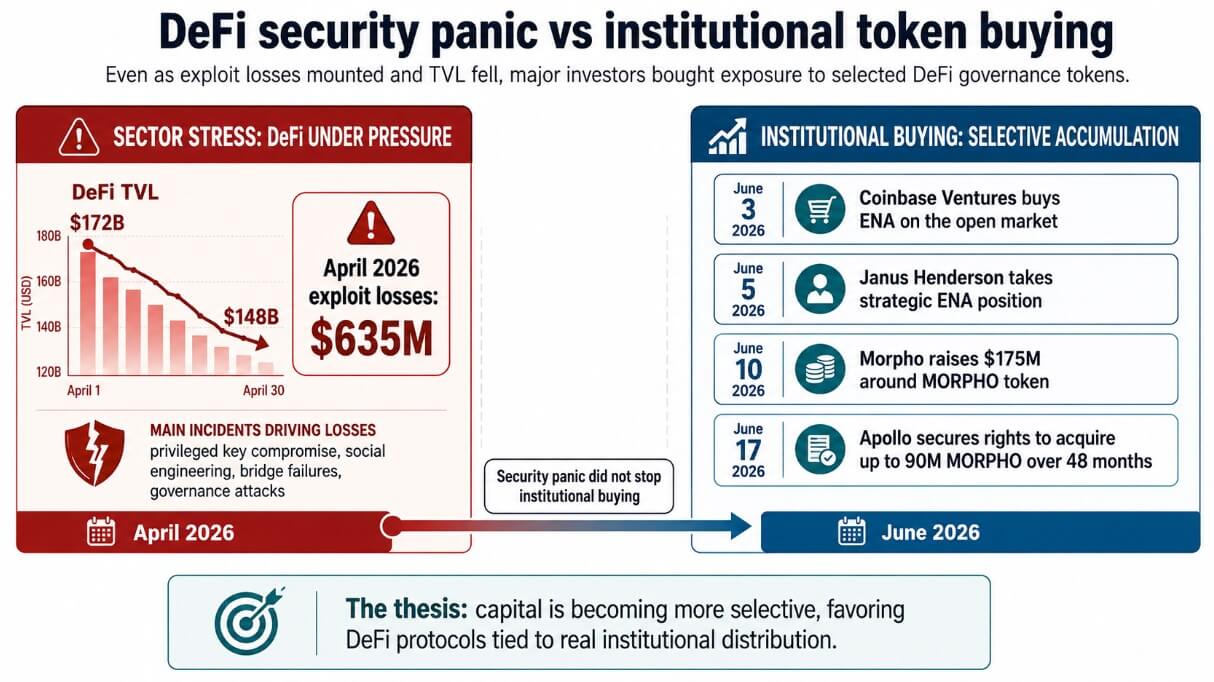

Total value (TVL) on DeFi fell from $172 billion to $148 billion as the sector posted $635 million in operating losses in April alone. Coinbase Ventures bought Ethena’s $ENA In a sign of the open market, Janus Henderson took his own strategy $ENA position, and Morpho closed a $175 million round that was entirely around the $MORPHO sign.

Apollo separately secured the rights to acquire up to 90 million $MORPHO tokens for 48 months.

The bet these investors are making is that governance tokens tied to DeFi protocols with true institutional distribution will appreciate as financial infrastructure, and that the security panic will accelerate that outcome by flushing weaker protocols from trading.

The infrastructure bet

Morpho reports over $11 billion in deposits and counts Bitwise, Galaxy, Anchorage Digital, Coinbase, Kraken and Binance among its institutional users.

Apollo’s token acquisition deal was limited to 90 million $MORPHO for 48 months with transfer and trading restrictions, structured by open market purchases, OTC transactions or other contractual arrangements.

Fortune reported that the $175 million increase valued the protocol at up to $2 billion, a figure derived entirely from the token’s market value.

$ENA sits at the governance layer of a synthetic dollar protocol routed through Coinbase’s more than 100 million users, with Coinbase already serving as Ethena’s primary custodian, wallet provider, and perpetuals location.

Meanwhile, Janus hooks up with Henderson $ENA position with plans for use $USDe to manage treasury cash and explore tokenized CLO collateral through Centrifuge’s infrastructure.

With 10-year Treasury yields hovering around 4.55% and a Fed target range of 3.50%-3.75% that most economists expect to hold through the remainder of 2026, yields on stablecoins, tokenized Treasuries, and on-chain credit markets have the kind of economic relevance that makes these positions legible for traditional asset managers.

$USDeThe company’s market capitalization was approximately $4.5 billion, up 13% in thirty days $ENA itself was trading around $0.08 with a market cap of around $750 million.

Why security panic tightens the position

The April incident wave included compromised privileged keys, social engineering, bridge failures, superficial attacks on governance and external dependencies.

Protocols with institutional distribution, professional integration of custody, transparent collateral structures and real demand from exchanges and asset managers bring a different risk profile.

If capital continues to drive down DeFi’s weakest level, the protocols already embedded in institutional workflows will absorb the flows and leave behind weaker venues.

Janus Henderson, Apollo, Circle Ventures and VanEck each built positions in DeFi infrastructure tokens as security fears accelerated the separation between protocols tied to real institutional demand and the DeFi TVL numbers that have historically followed, with capital becoming more selective about which rails it trusts.

$ENA And $MORPHO give holders governance rights over the protocols, with ownership of Ethena Labs or the Morpho Association, legal claims on cash flows, and control over assets, all beyond what either token conveys.

Betting on these tokens only works if adoption translates into demand for tokens, the relevance of the board or the credible capture of value.

DefiLlama shows that Morpho Blue generated approximately $39 million in gross protocol revenue in the second quarter, with $3.43 billion in active loans, while $6.43 billion in TVL flowed to liquidity providers and vault operators.

Coinbase and Janus Henderson provide Ethena with a distribution that most DeFi protocols cannot access $USDeThe company’s market cap grew roughly 13% in 30 days to about $4.49 billion.

Yet $ENA was trading down around 10% in value on the day of the Janus announcement, with a token at almost $0.08 and a market cap of around $750 million.

Buyers from $ENA take a position on a convergence between institutional adoption and symbolic value that the market has yet to price.

The shape of the next cycle

As Coinbase, Janus Henderson, Apollo, Circle and VanEck normalize DeFi-backed cash and credit products through their existing channels and the security panic continues to concentrate capital in top protocols, $ENA And $MORPHO repurposing as governance assets over infrastructure that handles real institutional volume.

$USDe would then retest a significantly larger supply base, and Morpho deposits would head towards $18 billion and $25 billion, with both tokens trading as strategic assets with a claim on the rails underneath.

If another major exploit, depeg event, or regulatory restriction interrupts institutional distribution, ownership of governance tokens proves that this was always decoupled from the protocol economy.

In this scenario $USDe supply would drop by 30% to 50%, $MORPHO would sell despite continued use of the protocol, and the discrepancy between owning governance rights and capturing the value of the protocol would remain large.

Apollo, Paradigm, a16z, Janus Henderson, and Coinbase Ventures each separately gambled that their chosen rails would have enough institutional volume to make managing those rails worthwhile.

Whether token ownership bridges the gap with the economic value flowing through the underlying protocols is the actual open question of the cycle.