")

Reimphoto/iStock Editorial via Getty Images

Here at the Lab, this year, we already followed up on Yara International ASA (OTCPK:YARIY, OTCPK:YRAIF), and today, the company released its nine monthly accounts. In our last publication, we were pricing an adverse scenario on Yara called ‘Too Much Short-Term Turbulence, A Pass At This Price.’ Since then, Yara’s stock price has declined by more than 30%, signing a minus 16.45%, including the dividend payment. Our underperforming rating was due to a potential inability to offset inflationary pressure cost increase. Our estimates indicated that for “each dollar increase in Nat Gas prices, this will translate to a negative $16 million EBITDA impact” for the company, valuing the Norwegian corporation at NOK 350 per share. Post Q3 results, the company is now trading at NOK 360 per share.

Mare Past Analysis

At the Lab, we believe that Q3 results conclude a difficult momentum. The company suffered from unfavorable circumstances such as adverse weather conditions, gas price movements, geopolitical events, and supply & demand imbalance. However, we are confident in the company’s passing this time and see light at the end of the tunnel.

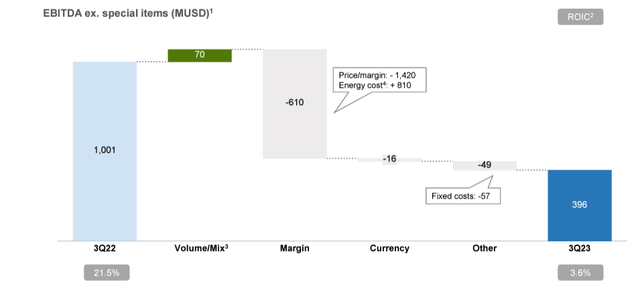

Looking at the numbers, the quarter EBITDA (excluding special items) stood at $396 million vs. $1 billion achieved last year (Fig 1). As a percentage, Yara’s EBITDA was down by 62%, mainly due to lower margins. Looking at the EBITDA waterfall, Yara was impacted primarily by higher energy costs (as expected and lower commodity prices). Consequently, the company’s net income reached $2 million compared to positive results of $402 million in 2022 Q3. These negative results were also emphasized by the CEO, who explained how Yara was “impacted by strong price declines compared to last year, as the nitrogen industry continues to operate in a lower margin environment.”

Yara Q3 Financials in a Snap

Fig 1

While cutting our earnings projections, we moved our rating from a Sell to a Buy valuation. The company is Europe’s largest nitrogen producer, and as a chemical business, you buy it when you hate it.

Why are we overweighting Yara at this time?

These are our key findings and forward-thinking estimates:

- Agricultural commodity prices such as nitrogen-intensive wheat suggest a positive momentum from here. During the analyst call, this was explained by the Yara management team, confirming that Agricultural fundamentals are supportive;

- With the ongoing Russian conflict, European food security is a priority, and Yara plays a strategic role in safeguarding Europe’s autonomy within fertilizer and food (Fig 2);

-

Looking back to the Q3 results, the summer season started with several weeks’ delay in many regions, and critical Yara products suffered from a shortened application window;

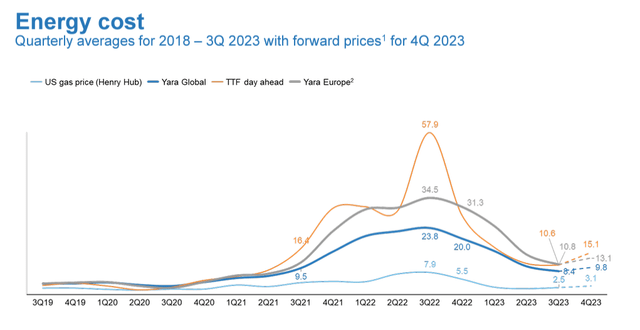

- For this reason, we believe that Yara’s Q4 margins will gradually improve. Year to date, Yara’s EBITDA reached $1.14 billion, and we anticipate a 2023 EBITDA of $1.58 billion (we are at -20% vs consensus expectation). In addition, we expect a demand normalization moving into 2024 with better supply-demand market conditions. Brazilian fertilizer inventories will be supportive in Q4, and we see no additional production capacity announcements. On the upside, the adverse geopolitical conditions cater to quite the opposite. Therefore, Yara might be a long-term beneficiary of this hostile environment. Over our one-year visible period, we project better 2024 numbers with an EBITDA estimate of $2.6 billion based on top-line sales at $17.5 billion. This is mainly based on nitrogen price of $500/tonne and unchanged Nat Gas price development (Fig 3);

- We know that lower gas prices might lead to higher margins; however, we prefer to remain cautious given the geopolitical situations (with more information, Yara did non-disclose an estimate both for Q4 and also for the entire 2024);

- Last but not least, here at the Lab, we have good coverage of the fertilizer industry (Fig 4), and we believe companies such as Yara and Corteva are long-term winners due to population growth estimates and improving living conditions (especially in emerging markets).

Yara’s strategic role in the EU food

Fig 2

Yara gas price evolution

Fig 3

Mare Past Analysis

Fig 4

Conclusion and valuation

We believe Yara will accelerate its EBITDA profitability in Q4. With a forecasted normalization in 2024 supported by farmers’ profitability and a long-term upside, the company needs to be more discounted. We were the first to report a short-term downside, and we believe that an adverse scenario is priced in. Our overweight target is based on nitrogen fertilizer prices that should support the company’s profitability and a solid balance sheet with a positive working capital inflow. Our 12-month target price is set at NOK 450 (from a neutral valuation of NOK 350 per share) and is based on a 4.5 EV/EBITDA multiple, well below the company’s 10-year median multiple (6.25x). Downside risks include changes in the key raw material prices such as the Natural Gas input, changes in currency rates, and competitors’ actions that might influence prices of NPK premium, Urea, and Nitrates fertilizers.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.