ljubaphoto

Given our extensive coverage of Exor (OTCPK:EXXRF), today we decided to look at Koninklijke Philips NV (NYSE:PHG). In mid-August, Exor, the Agnelli Holding company, acquired a 15% equity stake in Philips for a total consideration of €2.6 billion. Looking at the press release, the investment holding company does not intend to purchase additional Philips stocks in the short-term horizon; however, the deal provides an optionality to increase its stake up to the maximum limit of 20%. Excluding Juventus SpA, Koninklijke Philips NV is the only listed company not covered by the Mare Evidence Lab team; however, we deep-dived into Philips in our recent publication called ‘A Supportive Healthcare Acquisition.’

In detail, Philips is a Netherlands-based health technology company that engages its activities in three segments: 1) Diagnosis and Treatment (delivers precision medicine treatment and therapy), 2) Connected Care (provides consumers and clinicians digital solutions), and 3) Personal Health (which engages in chronic disease solutions). In 2021, Philips was involved in a respiratory scandal, and the company was forced to recall millions of defective ventilators, which the FDA had placed in the highest risk class. In the last two years, Philips suffered economic and image damage harshly, losing over two-thirds of its market valuation. At first sight, we viewed Exor’s recent investment as an opportunistic momentum; however, last week, the FDA Center for Devices and Radiological Health (CDRH) provided a follow-up on the Philips apnea device product recall with the following statements:

- “The FDA does not believe that the testing and analysis Philips has shared to date are adequate to fully evaluate the risks posed to users from the recalled devices.”

- “Although Philips concluded that the exposure to foam particles and VOCs from these devices is unlikely to result in an appreciable harm to patient health, the FDA believes additional testing is necessary.”

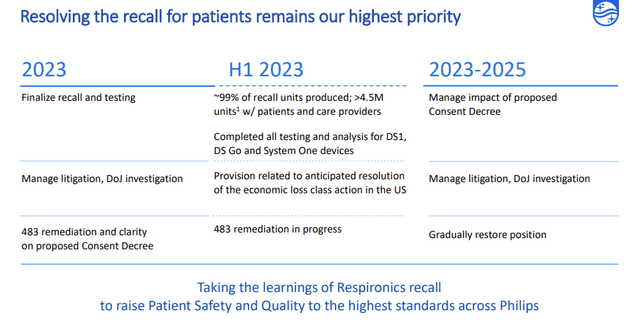

In addition, the FDA also reported that it “remains unsatisfied with the status of this recall, and we continue to take steps to protect the health and safety of individuals using these devices.” Looking back, in numbers, the recalled devices used foam that could degrade if exposed to cleaning chemicals, causing damage to the respiratory tract or cancer, which recorded 100,000 reports of complaints and 385 deaths. Philips already tested its device in five independent labs but agreed with the FDA to carry out additional testing. Following his predecessor’s resignation in October 2022, the new CEO, Roy Jakobs, confirmed that product recall and litigation are at the top of Philips’ priority list (Fig 1). Having taken the company’s reins, Jakobs set up a transformation plan to revive the company. Last month, the company settled a legal claim for which it had previously made a provision of €575 million. However, the company still faces personal injury claims and a U.S. Department of Justice investigation. The company is negotiating with the FDA for a “consent decree” (i.e., a settlement to resolve a dispute without admission of fault or liability).

Philips product recall timeline

Fig 1

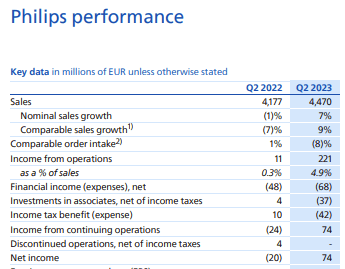

Before the scandal broke out in the USA, Philips was trading at a peak valuation of €48 per share, while today, the company’s share price is below €20 per share. What is crucial to report is that Phillips aims to “improve 2.5 billion lives a year by 2030, including 400 million people in communities with poor access to services.” Looking at the H1 results, the company returned to a slight profit of €74 million (Fig 2).

Philips Q2 Financials in a Snap

Fig 2

Looking ahead, Q3 will be supportive for the company. In our forward-thinking analysis, we think Diagnosis and Treatment will continue a positive growth momentum, benefitting from re-entering the US markets after the product recall. We estimate that Philips will gradually regain market share penetration with a ramp-up in sales of sleep devices. For Q3, we forecast a plus 9% growth from this division, signing an acceleration compared to Q2. Despite the tougher competition, we also view the Personal Health segment positively and imply top-line sales growth of a plus 4%. The segment margin improvement was due to pricing power that offsets inflationary cost pressure. Already in Q2, the company’s adj. EBITDA margin reached a 16%.

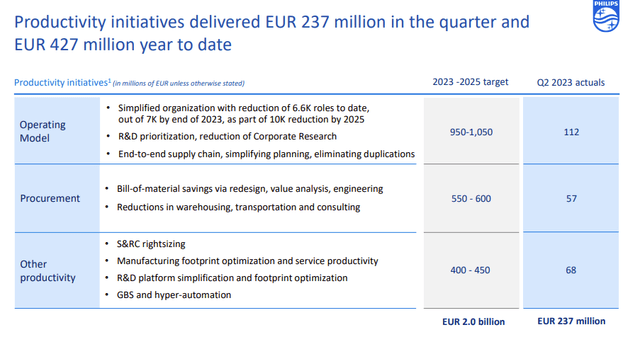

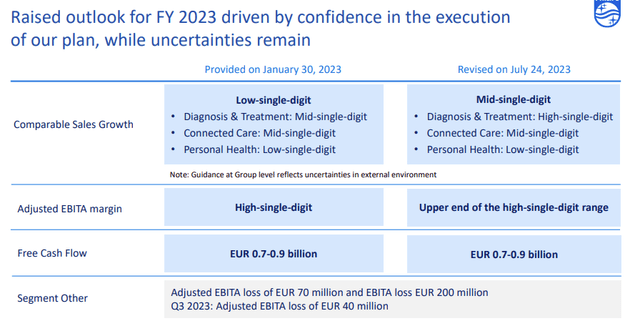

Therefore, the Fiscal Year 2023 outlook is well underpinned here at the Lab. In our estimates, we are confident that the company might surprise Wall Street analysts to the upside, helped by margin recovery in H2 thanks to easing logistics and pricing power benefits (Fig 3). Our 2023 estimates project a plus 6% organic growth (lower than consensus at 6.2%), but our EBITDA margin is set at a double-digit rate (10.5% compared to a Wall Street average of 9.9%). To support our analysis, we also recall that Philips has a solid order book and recently increased its yearly guidance (and we are in the company’s upper-end estimates – Fig 4).

Philips cost saving initiatives

Fig 3

Philips 2023 Guidance

Fig 4

Valuation and Risks Section

Our target price is mainly influenced by two main uncertainties: Philips order book growth, which might be impacted by the Chinese anti-corruption slowdown, and litigation payout. Here at the Lab, we decided to have a prudent approach in valuing Philips, and we decided to have a neutral valuation, given the potential future pressure related to the Respironics recall. The financial impact is difficult to quantify; however, last year, our internal team already performed this exercise to assess this exercise in assessing Sanofi’s implication in Zantac’s potential litigation.

Speaking of numbers, today there are less than 2,000 claims, but this might increase as the litigation moves forward. If we are looking at past drug settlements, we are ranging from $30k to $270k per person.“

Therefore, taking the current 100,000 complaints and multiplying to the low-end litigation cost, we end up with a €3 billion lawsuit. This should be included in an equity value bridge calculation. Excluding this potential impact, our team forecast an EPS of €1.4 for the current year. For the above reason, we are not including a DCF approach due to many variables, and looking at Philips P/E, the company is trading at a 50% discount vs. its closest peers, such as Siemens Healthineers. With a P/E of 14x, we arrive at a valuation of €19.6 per share, in line with Exor’s acquisition price and Philips’s current market valuation. Thus, we initiated coverage with an equal-weight valuation.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.