Milan Markovic

Investment thesis

Our current investment thesis is:

- CWH has a fantastic business model, with much credit due to Management. CWH provides and range of products and services within the camping/outdoor industry, continually expanding as it looks to maximize its value extraction. Thus far, innovation has been relatively successful.

- Despite this, the business has been unable to reduce its cyclicality, with the current downturn contributing to a significant deterioration in financial performance. We suspect the business will further decline in the coming quarters, with several years required to recover margins.

- CWH is currently underperforming its current peer group while its valuation is seemingly underrepresenting the issues ahead.

Company description

Camping World Holdings (NYSE:CWH), headquartered in Lincolnshire, Illinois, is a leading retailer of recreational vehicles (RVs) and outdoor lifestyle products. The company operates under various brands, providing a comprehensive range of products and services to outdoor enthusiasts.

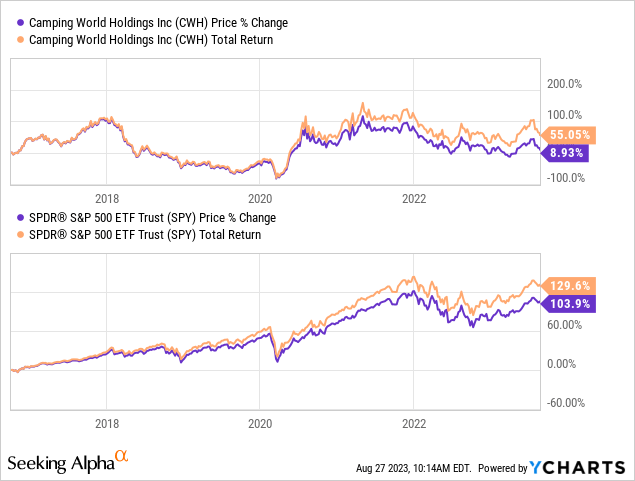

Share price

CWH’s share price performance has been disappointing since listing, with -18% returns compared to over 100% by the S&P. This is a reflection of its “good times” valuation for most of the period in conjunction with growth achieved.

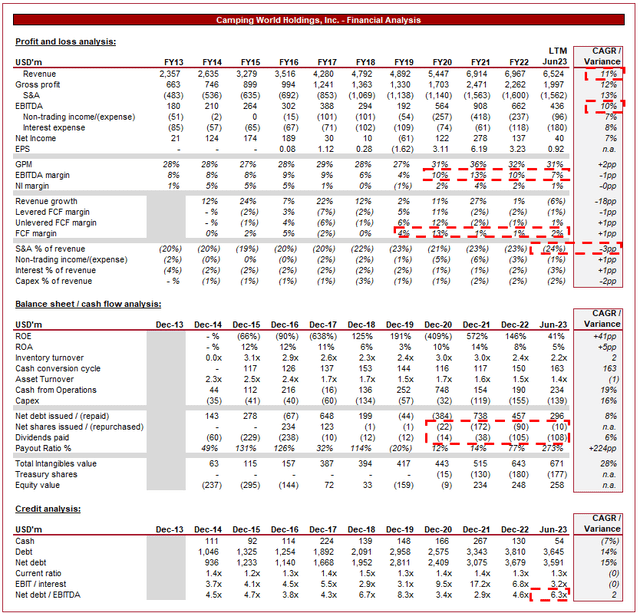

Financial analysis

Camping World Financials (Capital IQ)

Presented above are CWH’s financial results.

Revenue & Commercial Factors

CWH’s revenue has been strong during the last decade, with a CAGR of 11% into the LTM period. During this period, the growth has been incredibly consistent, with the first annualized decline occurring during the LTM.

Business Model

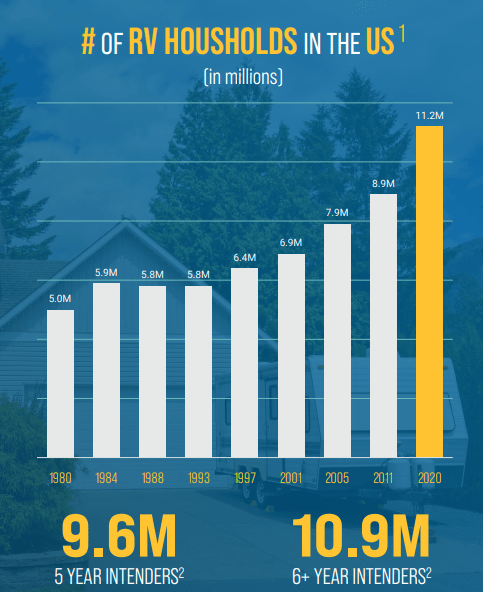

CHW is primarily known for its extensive selection of new and used RVs, ranging from motorhomes and travel trailers to pop-up campers and fifth wheels. The RV industry has experienced healthy growth in the last few decades, as American households increasingly seek domestic holidays and the flexibility over time that comes with RV ownership.

RV growth (CWH)

In conjunction with this, the company offers a wide range of camping gear, outdoor equipment, and accessories. This is a natural development for CWH, as it allows the business to expand its product offering, reducing reliance on RVs, while capturing the sale target market. This has contributed to a positive development in CWH’s brand and improved its growth trajectory.

Snapshot (CWH)

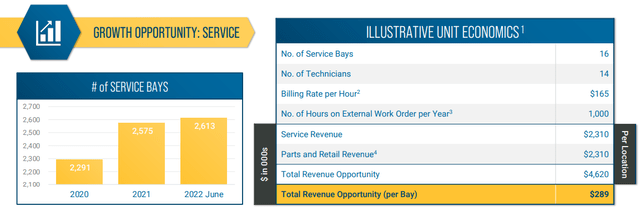

Furthermore, CWH provides maintenance, repair, and upgrade services for RVs, as well as financing optionality. This is critical for providing a seamless experience for its customers, contributing to an enhanced value proposition.

Management sees this as a growth opportunity for the business and we are not surprised. The economics with these types of services are generally higher and more recurring in nature, positively smoothing the revenue trajectory.

Services (CWH)

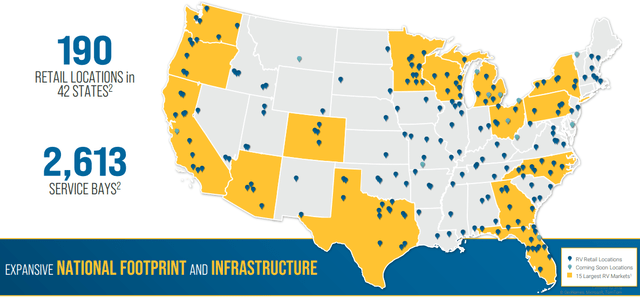

The company operates a network of dealerships across the United States, offering a one-stop shop for RV sales, service, and accessories. This is one of the company’s key competitive advantages, as it has an impressive reach in the country despite the relative niche of the product offered. This further enhances the value proposition as consumers are comforted by the fact Service Bays are relatively accessible.

National reach (CWH)

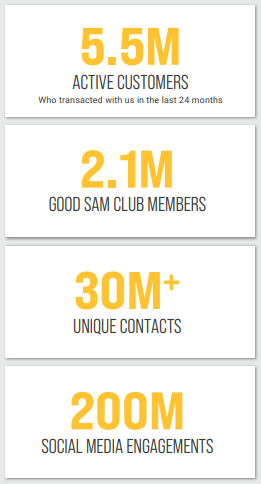

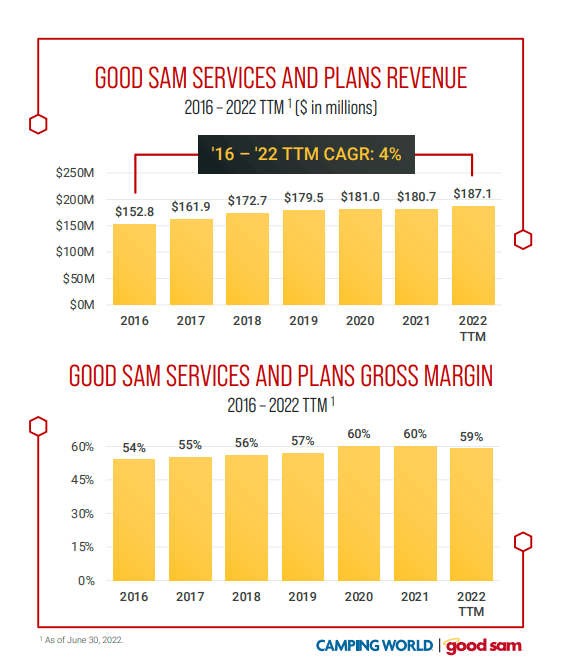

CWH owns and operates the Good Sam Club, a membership program that offers benefits such as discounts on camping sites, fuel, and products, fostering customer loyalty. This business is highly accretive for the business in margins, while growing at a respectable level. There are significant cross-selling opportunities with this brand with minimal incremental opportunity costs.

Good Sam (CWH)

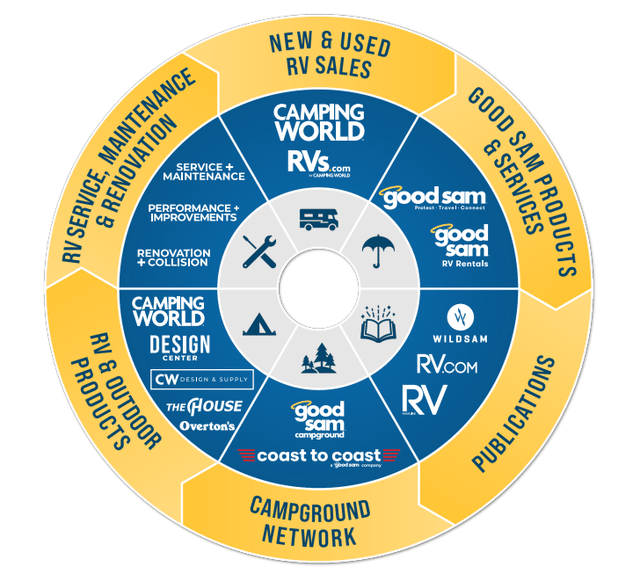

Across these services, CWH has managed to build an outdoors/camping mega-business, with a range of brands that provide related services, within its sphere of expertise.

Brands (CWH)

This has contributed to significant diversification benefits, while also broadening its TAM. This is the primary reason for its good growth trajectory and why maintaining HSD is a reasonable expectation in the long term. The ability to develop these existing brands further, while also discovering new avenues for growth, will be critical to its long-term success.

360 reach (CWH)

The current growth opportunities we see are:

- E-commerce. CWH has an e-commerce platform that allows customers to shop for RVs, camping gear, and accessories online, providing convenience and access to a broader customer base. Further development of this will support enhanced growth as retail spending increasingly moves online.

- Expansion. The business has the optionality of GF or M&A, with scope for synergies and the development of dealership relationships.

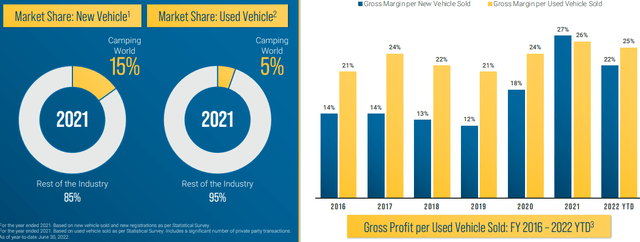

- Increasing Used vehicle business. Margins within this segment are superior and more robust. Expanding its market share here has the potential to create a closed-loop around the RV buying and selling lifecycle.

New vs. Used (CWH)

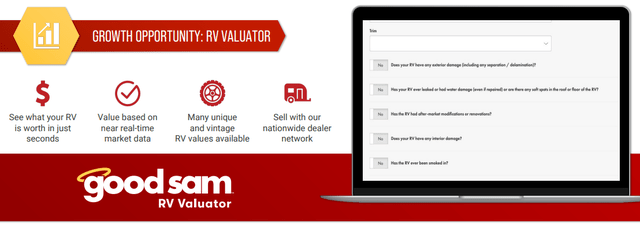

- RV valuator. As if CWH has not already maximized the value extraction from this camping universe, the business is also expanding its valuation services. With strong data capabilities (that CWH should invest in), this can be a highly lucrative expansion, even if it does not reach a substantial absolute scale. This is another example of a small development in the business model that incrementally improves the company.

Good Sam RV Valuator (CWH)

Competitive Positioning

We see the following as key competitive advantages:

- One-Stop Shopping. CWH provides a comprehensive range of products and services under one roof that appeals to customers who want a convenient and comprehensive solution for their outdoor needs.

-

Brand Recognition. CWH’s brand recognition and presence in the outdoor industry contribute to its ability to attract new customers and retain loyal ones.

-

Strategic Acquisitions. Management’s willingness to acquire smaller businesses within the industry can help to maintain its current competitive position.

-

Cross-Selling Opportunities. CWH has a strong ability to cross-sell products and services across its many brands, maximizing the value generation from the industry.

- Growing Interest in Outdoor Activities. The overarching increase in popularity of outdoor activities, camping, and road trips will drive demand for RVs and camping gear, benefiting Camping World.

Economic & External Consideration

Current economic conditions have been highly problematic for the company. With elevated interest rates and high inflation, consumers are experiencing an attack on finances, with living costs souring. This has contributed to reduced discretionary spending, particularly on large ticket purchases. Even those who are less impacted will inevitably soften spending / be more hesitant, given the uncertain economic outlook.

Given the discretionary nature of RVs, and more broadly the activities associated with them, the concern is that consumers will be far less willing and (with rates where they are) able to purchase RVs. This is the primary reason for the decline in financial performance we feel.

The following are key takeaways from CWH’s most recent quarter:

- Top-line revenue declined (12.7)%, driven by a decline in New vehicles and Financing activities.

- New vehicle sales declined (26)% YoY, reflecting the inability to finance and the inherent reduced demand.

- Used vehicles remained impressively robust, with growth of +12%. This is likely due to consumers trading down. Although the New vehicles are the bigger ticket item, we are not overly concerned in the near term due to the superior Used vehicle margins.

- Other services, such as products and services, have also declined but to a reduced level. This is a reflection of the underlying softening in the market.

Our expectation is for this to continue, at least in the coming 2 quarters, as rates must remain high to bring inflation under control.

Compounding this cyclicality is seasonality, as the company is dependent on seasonal demand for outdoor products and RV travel. This can contribute to a financial crunch in particular quarters, given the belief that struggles with continue.

Margins

CWH’s margins had been on an upward trajectory, owing to operational cost leverage and its expanding business model. This has reversed significantly in the last 12-24 months, primarily due to economic conditions. With reduced demand, the company has been forced to increase discounting to drive sales, while also facing inflationary pressures.

We suspect there is more room to fall, particularly given both GM% is declining and S&A spending is not sufficiently offsetting the revenue decline.

Balance sheet & Cash Flows

CWH’s ND/EBITDA ratio is uncomfortably high, although should be noted relatives primarily to long-term leases. With interest payments representing 3% of revenue and interest coverage of 3.2x, we are wary but not overly concerned.

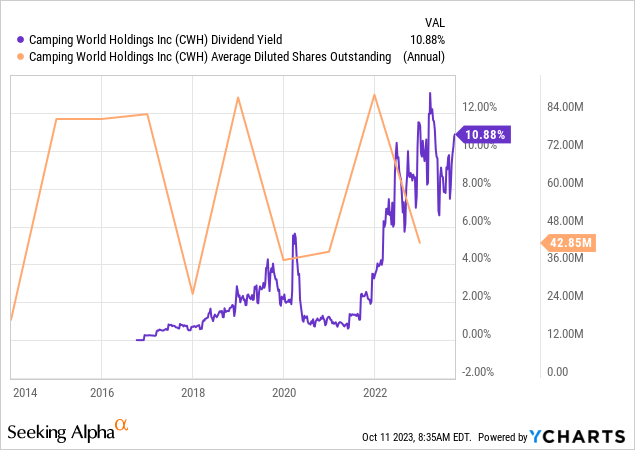

Management has been aggressive with raising debt and utilizing cash flows to fund dividends, boasting a substantial yield. We are very concerned about the sustainability of this, given the current payout represents over 100% of the LTM FCF. Assuming its performance continues to remain weak into FY24, Management will likely need to soften this or raise more debt (which we would suggest against).

Outlook

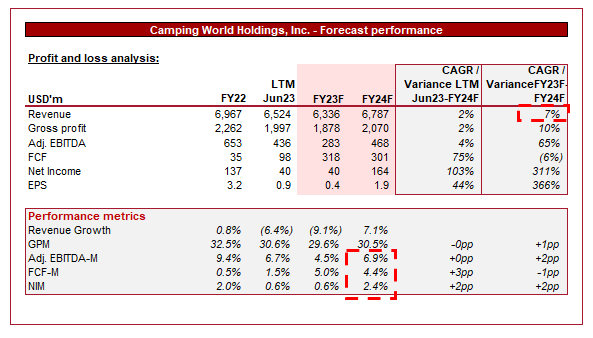

Forecast (Capital IQ)

Presented above is Wall Street’s consensus view on the coming 2 years.

Analysts are forecasting a difficult FY23, expecting CWH’s performance to worsen in the coming quarters. This looks to be a reasonable assessment given the macro conditions and the LTM performance thus far.

Further, a similar development in margins is expected, with a (2.1)% EBITDA-M decline from the current LTM level, only slightly improving in FY24F. This is likely a reflection of demand-driven adverse pricing. The concern is that once demand picks up, CWH will not be positioned to immediately win back the margin it has lost.

Industry analysis

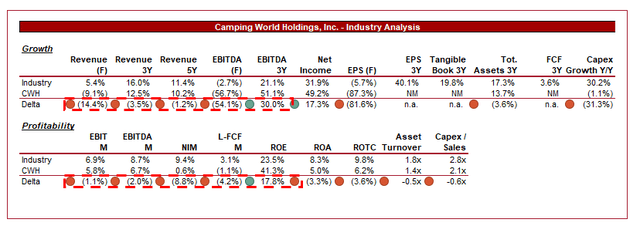

Automotive Retail Stocks (Seeking Alpha)

Presented above is a comparison of CWH’s growth and profitability to the average of its industry, as defined by Seeking Alpha (19 companies).

CWH underwhelms relative to this peer group, with lower growth and margins. The company’s exposure to what is a niche industry, despite its strong market share, is the primary reason for this. The scope for growth is limited and due to the discretionary nature of purchases, its margins are highly exposed to a downturn.

Valuation

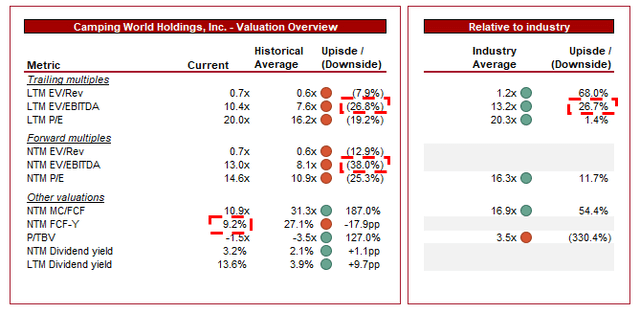

Valuation (Capital IQ)

CWH is currently trading at 10x LTM EBITDA and 13x NTM EBITDA. This is a premium to its historical average.

A premium to the company’s historical average looks difficult to justify today, primarily given the deterioration in margins. A slowdown/decline in growth is expected but it will be far easier to improve this than margins, leaving the business damaged in the medium term. We are positive about the commercial improvements achieved but this is not sufficient to offset the weakness.

Further, CWH is trading at a 26% discount to its peers on an LTM basis. Given the degree to which the company’s financial performance has suffered, and the likely continuation of this (while the wider industry is forecast to grow), a discount is undoubtedly correct. This said, we are hesitant to suggest it is sufficient given the discount is only +12% on a NTM P/E basis.

Final thoughts

CWH is a solid business, with a shrewd Management team that understands its niche. The eagerness to expand beyond RVs into related services is the correct decision and will support diversifying its business model. This said, the company is still highly exposed as the quarterly data suggests, making it uninvestable in our view, relative to its valuation.