")

Adam Berry

Shares of Vietnamese electric vehicle company VinFast (NASDAQ:VFS) have been on a rollercoaster since it listed its shares on the NASDAQ in August which at the time created major buzz. While shares initially soared on investor excitement, VinFast’s valuation has dropped massively: since reaching a high at $93, shares of the EV maker have crashed 92% and also dropped below their $22 listing price.

The EV manufacturer disclosed last week a strong increase in revenues for the third-quarter and improving gross margins, indicating that an investment in VinFast is starting to look more attractive now than it did in August. I am up-grading my rating on VinFast to hold in light of the firm’s delivery accomplishments in Q3 and I am looking forward to starting a speculative buy position in the EV company at around $5!

Previous rating

After VinFast’s listing on the NASDAQ I warned investors of the high risks associated with the Vietnamese electric vehicle company. My concerns chiefly related to the company’s excessive valuation: Sell The Hype. However, the EV maker recently reported preliminary third-quarter results which, together with a much more reasonable valuation, justify a rating upgrade to hold. The risk profile has rather significantly improved, in my opinion, and I can see myself establishing a speculative long position in the near term.

VinFast’s Q3’23 delivery accomplishments

Hype stocks like VinFast can become interesting for investors once excessively bullish sentiment deteriorates and investors are offered a more reasonable valuation.

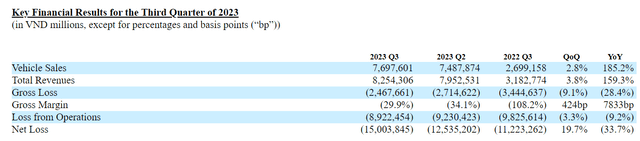

In a regulatory filing from last week, the Vietnamese company released preliminary Q3’23 results and said that it made 10,027 electric vehicle deliveries in the third-quarter compared to just 153 in the year-earlier period and compared to 9,535 electric vehicles in the previous quarter. The company also confirmed its delivery target 40,000 to 50,000 EVs in FY 2023.

Revenues associated with EV sales soared to 7,697,601M Vietnamese Dong ($319.5M), showing a year over year increase of 185.2% year over year. Total revenues across business divisions (which include VinFast’s sizable e-Scooter business) totaled 8,254,306M Vietnamese Dong ($342.7M), showing an increase of 159.3% year over year.

VinFast is making rapid progress in moving its enterprise towards profitability and scaling its footprint, especially in North America. While the EV maker still lost a ton of money in the third-quarter, VinFast is seeing positive gross margin momentum as well: between Q2’23 and Q3’23, VinFast’s gross margin improved 4.2 PP to (29.9%).

While the firm’s gross margins are still negative and VinFast needs to grow into a larger delivery volume in order to run its EV operations profitably, all major performance metrics point in the right direction (revenues increased at triple-digits, gross margins are improving, operating losses are declining).

VinFast generated 8,922,454M ($370.4 million) in operating losses in Q3’23, putting the company on a path toward annualized losses well above $1.0B, but the good news is that losses are narrowing. Going forward, I expect the EV maker to continue to report sequential improvements in its gross margins as the company ramps up production and deliveries.

Source: VinFast

Liquidity and cash burn

According to VinFast’s disclosure of Q3’23 financials, the EV firm had 3,154,673M Vietnamese Dong ($131.0M) in cash at the end of the third-quarter. Considering that VinFast is still losing money on each vehicle it produces and sells, there is a risk that, going forward, VinFast would have to either sell more equity or issue new debt in order to finance its operations. In the third-quarter, the EV maker said it lost 2,467,661M Vietnamese Dong ($102.4M) on its EV operations so the cash burn is still high. Since the company just listed its shares on the NASDAQ successfully, investors should expect that VinFast will raise more cash through equity sales.

Why I will buy VinFast at $5

VinFast’s valuation, as I said in the introduction, has seen a serious drawdown since August… they are down more than 90% and an entry becomes increasingly attractive.

VinFast now has a market cap of $17B… which is a huge difference to the $70B that the company achieved when I last covered the electric vehicle business.

VinFast just disclosed $342.7M in Q3’23 revenues in its preliminary disclosure, meaning the EV maker is, on an annualized basis, looking at $1.4B in revenues. Assuming that the EV can increase its revenues between 100-110% next year, which I believe is reasonable considering that the company is launching new EV models, such as the VinFast VF 6 — which is a subcompact crossover sport utility vehicle — and seeing considerable delivery momentum, I estimate that VinFast could generate between $2.8B and $2.9B in full-year revenues next year.

This means that the EV maker is currently valued at 6.1X estimated forward revenues which is still a premium multiplier factor, but not as outrageous as the August valuation. U.S.-based EV companies also sell at high premiums, based off of sales.

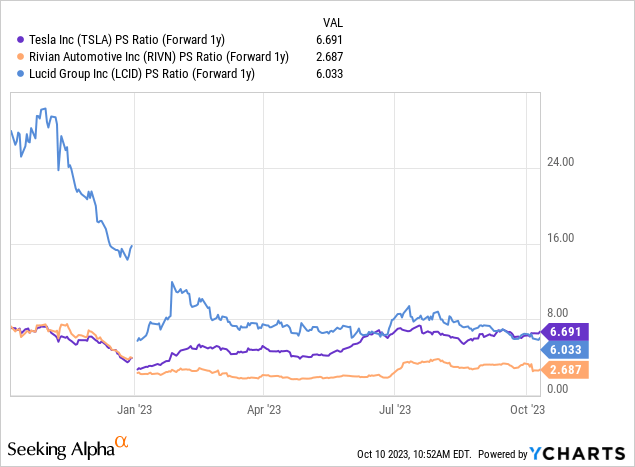

VinFast would become interesting to me at the $5 price level which implies a revenue multiplier factor of 4.2X… which would make VinFast cheaper than Lucid Group (LCID). The U.S.-based EV company is currently trading at a P/S ratio of 6.0X. While VinFast is not on the same level as Tesla (TSLA), the Vietnamese EV maker nonetheless demonstrated with its Q3’23 release that it maintains considerable delivery and top line momentum that is worthy of a premium valuation.

Risks with VinFast

VinFast is still a highly-valued electric vehicle enterprise and there are still certain risks associated with the company’s high valuation factor. Additionally, VinFast’s electric vehicle operations are still not profitable and the company loses money on every electric vehicle that it sells to customers. Due to VinFast’s triple-digit Y/Y top line growth in Q3’23 as well as an improving risk profile, I actually believe that we are nearing a potentially attractive buy point.

Final thoughts

The investment situation at VinFast has greatly improved since August and I am looking to establish a position in the Vietnamese EV company if the share price drops toward $5. Undoubtedly, the risk profile has become much more favorable after VinFast experienced a massive decline in its valuation and the company’s preliminary results for its third-quarter showed that key metrics for the EV company are on a good trajectory. VinFast has considerable EV delivery momentum and although its gross margins are still negative, the broader trend indicates narrowing losses and solid top line growth. I am up-grading VinFast to hold given the improved valuation situation and Q3’23 results. At ~$5, I would raise my recommendation from hold to buy!