bennymarty

Swiss premium confectionery company Lindt (OTCPK:LDSVF)(OTCPK:COCXF)(OTCPK:CHLSY) continues to impress on revenue and profit growth. While consumer spending and cost inflation pose an ongoing challenge, Lindt has thus far seen relatively modest pushback on higher prices, while EBIT margin in the first half of FY2023 came in at a record high.

Business performance has never been my concern here. Where I felt things came apart a little in past coverage was with the stock’s valuation. The company’s plan to grow revenues by 5-7% annualized while realizing 20-40bps per annum of EBIT margin expansion points to solid earnings growth ahead, but in recent years that has been reflected in a commensurately lofty valuation.

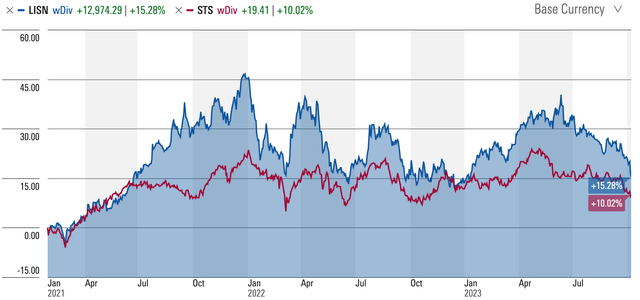

While valuation remains my chief concern, it hasn’t stopped these shares from registering around 500bps of outperformance versus the wider European staples space since my last piece, notwithstanding a pretty flat stock price these past two years.

Lindt total return versus SPDR MSCI Europe Consumer Staples ETF (Source: Morningstar)

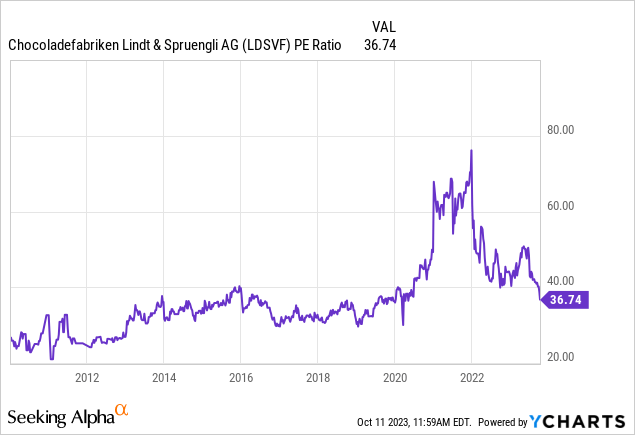

Looking ahead, management guidance for FY2023 is bullish, with upgrades delivered for both sales and margins. I would note, though, that the company’s battle against cost inflation could well drag on into FY2024, and I would worry about the willingness of consumers to absorb further steep price hikes should that be the case. With these shares trading for around 36x my FY2023 EPS estimate, I maintain a Hold rating.

Continuing To Deliver Strong Results

Many staples stocks found themselves in a sweet spot following the current bout of inflation, pulling off aggressive price hikes without seeing too much pushback from consumers. Even brands with less strength than Lindt’s surprised to the upside – with positive volume growth coming in despite double-digit moves in price. Lindt was no exception, with volume landing at positive 2-3% in FY2022 notwithstanding a positive 8-9% print from price.

2023 is seeing consumers starting to waver a little, but Lindt continues to deliver strong results. Though volumes were actually down a touch, positive contributions from channel and product mix led to a circa 1% total contribution from volume/mix. Price was up in the 9% area year-on-year, with that driving around 10% year-on-year organic sales growth.

Margin performance was also strong. H1 EBIT margin of 12.2% was a record, with that driven by a combination of higher revenue, the impact of commodity price hedges (mitigating input cost inflation), and efficiency gains in its North American business.

A Couple Of Near-Term Risks To Consider

Strong performance in H1 led management to upgrade its full-year FY2023 guidance, with organic growth now seen a point higher at 7-9% (was 6-8% previously) and EBIT margin expansion 10bps higher at 30-50bps (was 20-40bps previously).

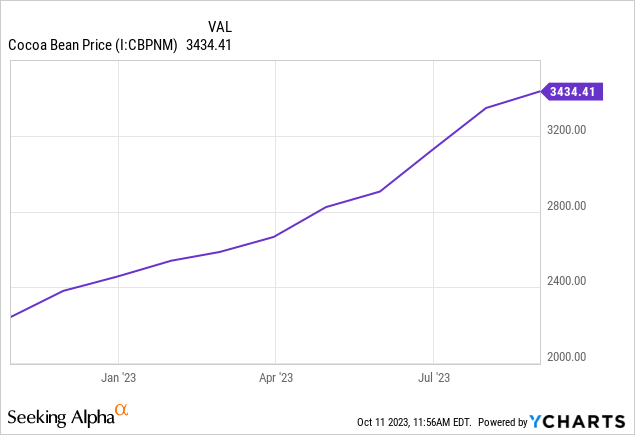

Without wishing to overdo it in terms of negativity, I would note a couple of potential headwinds to consider in the near term. Firstly, cocoa is obviously a key input for Lindt and its hedging program has been one driver of its strong EBIT performance. Those hedges rolling off will naturally have the opposite impact. Now, this is obviously already reflected in the above guidance, but what I would note is that cocoa futures prices have continued to head higher post-H1 results. This is perhaps something to be mindful of in the context of results in H2 and FY2024.

Secondly, the impact of the above would likely result in further price hikes across the industry. As I mentioned above, consumers are already responding more earnestly to price hikes as their own finances come under strain. This is by no means Lindt-specific; indeed, the company actually outperformed the wider chocolate market in H1, with a circa 1.5% volume decline in the wholesale channel versus circa 2.5% for the market. However, the potential for further softening of volumes is again something to bear in mind.

Also, worth noting is the possibility that Lindt’s business has become even more seasonal as a result of the current economic climate, with management noting in H1 that its nonseasonal volumes were relatively weak:

But definitely, in the first half, we saw what I said, right? I mean you saw that permanent products like tablets, they did a little bit less well on volume. I mean we also increased prices. So overall value was positive, but in Nielsen, it was negative, and we saw this kind of trade-up towards seasons and towards Lindor.

Martin Hug, CFO Chocoladefabriken Lindt & Sprüngli AG, H1 Earnings Call

Again, this is not something that needs to be overemphasized, but if you are an investor that is sensitive to Lindt’s near-term earnings then this would be another point to chew on.

Finally, and more longer-term, I would note that management expects the company’s realized tax rate to head a touch higher into the 23-25% area. That’s around 6ppt higher than it will land this year.

With that, my FY2023 EPS estimate is CHF 2,670, with that based on management’s (updated) organic sales and EBIT guidance, plus expectations for a slightly lower tax rate this year (sub-20%) and slightly worse net financial expenses compared to FY2022.

Valuation Remains The Main Concern

While the above could introduce a little more volatility/risk into Lindt’s short-term earnings outlook, my concern remains primarily valuation-based. The company’s growth formula (5-7% organic sales growth plus 20-40bps of EBIT margin expansion) would see it grow EBIT by around 8% annualized over the medium term on a currency-neutral basis, with net income likely trailing due to expectations of a slightly higher tax rate. The registered shares trade for CHF 98,800 at the time of writing, putting them at around 36x my FY2023 EPS estimate above.

That kind of multiple and growth outlook introduces a lot of sensitivity to valuation changes over the next few years. Although Lindt has typically commanded a high EPS multiple, it’s not like it has never traded sub-30x earnings before. Even a contraction into the 28-29x EPS area would be enough to undo around 3-4 years of EPS and DPS growth here. With European staples peers like Heineken trading for less than half that multiple with only modestly lower medium-term growth ambitions, I continue to view Lindt’s valuation as being a bit too rich. As such, I maintain a Hold rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.