damircudic

Investment Thesis

Primoris Services (NYSE:PRIM) sits at the intersection of legacy construction services, recurring revenue master service agreements, and a massive tailwind from the Inflation Reduction Act. With uncertainty around how the IRA will impact construction firms, especially those involved in solar installations, I believe Primoris is uniquely positioned to capitalize on the coming wave of green energy projects over the next few years. Its strong culture, talent programs, and substantial solar backlog provide competitive advantages and pricing power. Furthermore, management has yet to incorporate the full benefits of the IRA into financial projections, presenting a significant upside. With the stock trading at an attractive valuation, Primoris offers a compelling opportunity.

Introduction

Founded in 1960, Primoris is a construction and master services agreement provider focused on the industrial and corporate utility space. The company operates two main business lines:

1. Utility Construction

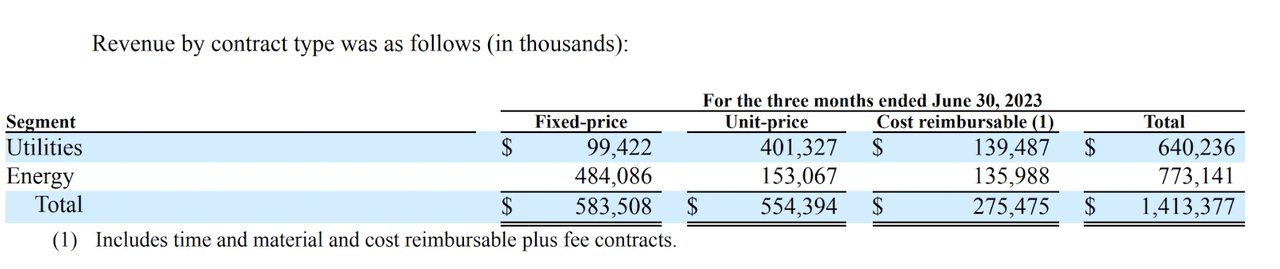

Building power generation and transmission facilities, mainly for utility customers in the southern United States. This includes master service agreements (MSAs) that provide recurring revenue streams, similar to SaaS models, and fixed-price contracts. MSAs made up $477 million of the $640.2 million in Utilities revenue in the quarter ended 6/30 (10-Q).

MSA Revenue Primoris (Primoris 2Q 2023 10-Q)

2. Energy Segment

Constructing energy facilities. A major revenue driver is solar facility construction, with over $1 billion in solar backlog as of last disclosure (likely higher now). Most of these contracts are fixed, representing $484 million of the $773.1 million in segment revenue in the quarter (10-Q).

Fixed Contract Revenue Breakdown (Primoris 2Q 2023 10-Q)

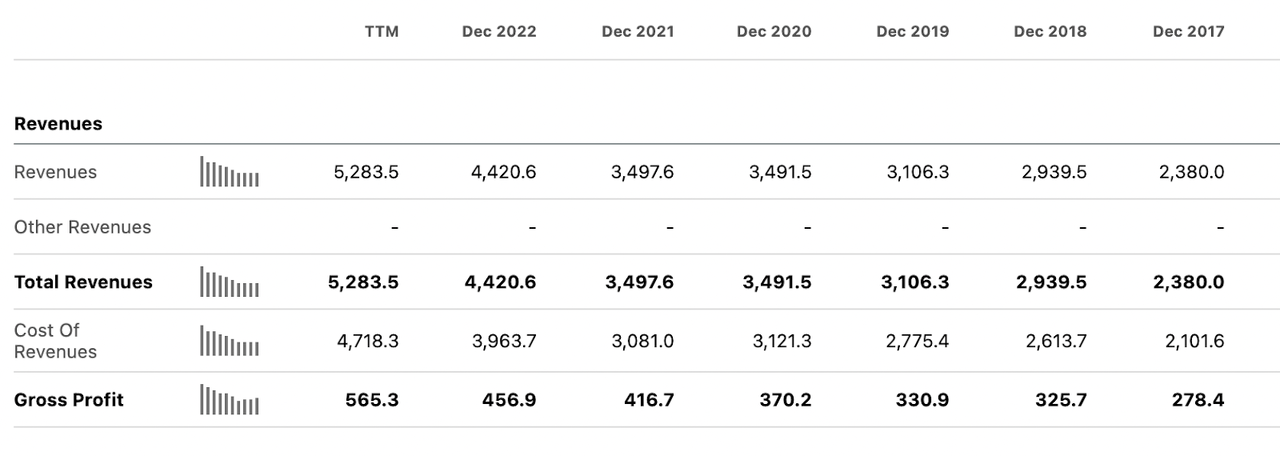

Primoris has seen tremendous growth, with revenue more than doubling since 2017. It also currently sports an “A” rating from Seeking Alpha’s quant metrics for growth. The company has used leverage to fund acquisitions and consolidate smaller players into its unique business model – one that is positioned to benefit enormously from the Inflation Reduction Act.

PRIM Revenue History (Seeking Alpha)

Management Commentary

In May 2023, we spoke with Primoris’ investor relations team, who explained the lack of IRA discussion on earnings calls. At the time, the Treasury Department was still finalizing implementation details meaning they could not begin to price in the magnitude of benefit that the IRA would have on their customers and their backlog (the rule ended up being released on 8/30/2023).

However, management believes the IRA will be massively beneficial, especially given Primoris’ substantial solar backlog stretching to 2025 (even without the IRA). This represents alone nearly $1bn in backlog of the $6.5 billion (10-Q) in total project backlog they have (note: solar backlog figures are slightly outdated, but these numbers have likely increased according to every indication).

In their Q2 2023 earnings call, management noted that customers are already complying with IRA labor requirements sooner than expected. Labor requirements are key in order to get IRA funding:

We are also seeing our customers comply with IRA labor requirements sooner than we expected, following further clarity on the IRA incentives that were made known in May of this year. This means that our apprenticeship and prevailing wage programs are now in place, and we have plans to execute on our first project using this program, beginning in Q3. -PRIM Q2 2023 Earnings call

This demonstrates the IRA is driving real customer behavior changes now. Additionally, management highlighted continued strong tailwinds:

Market for renewables remains strong and we aren’t anticipating a slowdown within the next few years. Solar module delays are appearing to be less of a concern for delivery in 2024. To support this, we are seeing billions of dollars of investments in domestic solar module manufacturing, to help the industry capture the benefits of the Inflation Reduction Act. -PRIM Q2 2023 Earnings call

Furthermore, Primoris focuses on smaller utility-scale solar projects that bigger competitors overlook (they look at Megawatt projects to bid on while bigger firms like Quanta Services (PWR) bid on Gigawatt projects). To be specific, Primoris typically bids on projects under 50 MWh in order to have lower permitting requirements (Investor Relations Call, May 22, 2023).

This allows them to win contracts with limited competition at attractive margins. The IRA incentives will only accelerate this trend as smaller projects become viable. Primoris is positioned perfectly to capitalize.

Financials

Primoris has achieved SaaS-like revenue growth in recent years. Revenue has more than doubled since 2017, and book value has also doubled. Long-term debt sits around $1.04 billion against a modest $1.65 billion market cap. While leverage has increased, Primoris is using it to fund acquisitions and increase competitiveness.

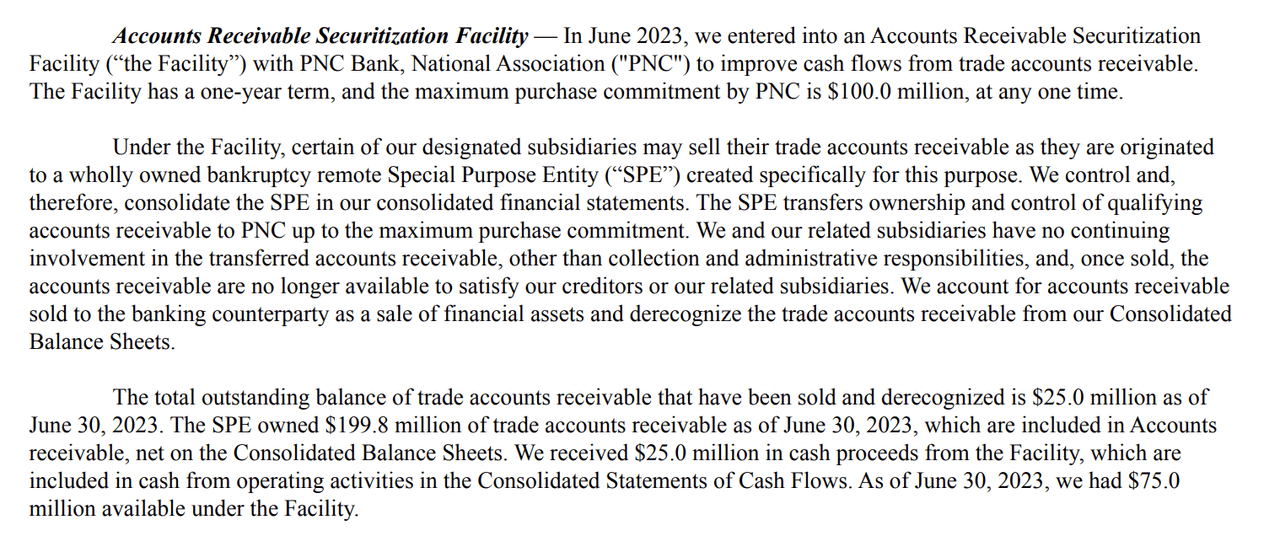

To offset rising interest costs from higher debt loads, the company has purchased interest rate hedges, an interesting tactic in the industry (10-Q). Primoris also carries a large accounts receivable balance. To improve working capital efficiency, management initiated an accounts receivable financing agreement with PNC Bank last quarter (10-Q). This provides immediate liquidity from completed projects to fund continued growth.

Accounts Receivable Facility (Primoris 2Q 2023 10-Q)

Valuation

Primoris’ valuation appears cheap (11.82x fwd valuation), and currently sports an A- sector relative grade valuation from Seeking Alpha for its trailing 12-month PE.

The firm has a PEG ratio of 0.92 and sports (compared to comps) an industry-low forward EV/Sales ratio of 0.52. Primoris presents potentially a deep value opportunity, given the unique opportunity for them to ride a powerful industry tailwind. In fact, Primoris sports a lower forward PE than Quanta Services and the sector median as well. Note: Quanta Services has diversified business lines, but bids on contracts in a similar space as Primoris but on a larger scale. Primoris contract bidding strategy produces higher margins on these contracts due to less competition, yet the street has given them a lower valuation multiple.

| Company | Primoris (PRIM) | Quanta Services (PWR) | Sector Median |

|

Forward P/E Ratio (Non-GAAP) |

11.82 | 24.93 | 17.43 |

In addition, Primoris also has a slightly higher ROE (11.27%) than Quanta Services (10.62%) even though it trades at less than 1/2 the forward earnings multiple. Significantly lower forward earnings multiple for a higher ROE and an industry-low EV/Sales ratio?

Amazing.

Risks

Any investing comes with risks, Primoris is no different. Primoris’ high use of debt increases interest rate sensitivity. They are currently exposed to an additional $6 million in interest payments annually for every 100 bps increase in interest rates (10-Q). However, management is mitigating this risk through interest rate hedges. The large accounts receivable balance also exposes the company to customer payment risk. The PNC financing agreement helps reduce this risk and improve working capital efficiency.

Catalysts

As a potential long-term buy-and-hold, investing in Primoris means buying and expecting them to continue executing their strong growth strategy. The IRA provides a multi-year tailwind for utility construction spending. Primoris’ focus on smaller construction projects uniquely positions it to capture outsized benefits. Continued revenue growth, margin expansion through scale and acquisitions, and prudent balance sheet management should drive shareholder value creation.

The Bottom Line

With its smart business model and substantial backlog, Primoris is poised to be a winner from the IRA’s impact. Trading at an attractive valuation despite its strong growth trajectory, Primoris offers a compelling opportunity. I believe the company’s upside is still under-appreciated by the market.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Best Value Idea investment competition, which runs through October 25. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!