David Baileys

“Humankind cannot bear very much reality.” – T.S. Eliot

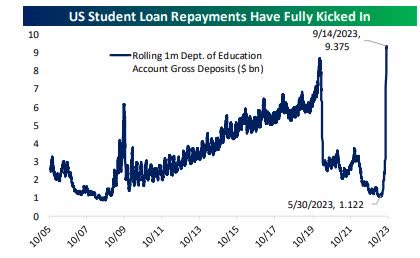

As the data continues to flow in, third-quarter GDP growth is ranging from the Atlanta GDP Now forecast of 4.9% to the St.Louis Fed Nowcast of 1.6% or the NY Fed Nowcast of 2.2%. Unless there is a change, Q3 GDP growth is going to surprise to the upside. October marks the date when student loan borrowers resume payments on their debt, as they haven’t had to make payments in over three years. So the pace of consumer spending is almost certain to slow.

Student Loans (www.bespokepremium.com)

Another factor, despite all the hype around wage increases and the all-is-rosy rhetoric, ” Real” wages have been declining for the past couple of years which means that consumer purchasing power has been eroded by the run-up in inflation. At the same time, workers at the Big Three automobile manufacturers are on strike. Nobody knows how long the strike might last, but it will harm GDP growth in the near term and it has a chance to improve both growth and inflation (assuming a large wage increase) once the strike ends.

Most economists believe Q4 GDP growth will not be nearly as solid as Q3. Then again we’ve heard this story before. It was not long ago that virtually every economist and market analyst (myself included) was convinced that the U.S. economy would be in recession in the second half of this year. That has not happened. Economics 101 says to never underestimate the strength and resilience of the U.S. economy. Perhaps of greater importance, never underestimate the unprecedented trillions of stimulus that was added to the economy. Add to that rule, the amount of time it will take to work its way out of the system. If anything I’m guilty of miscalculating the latter.

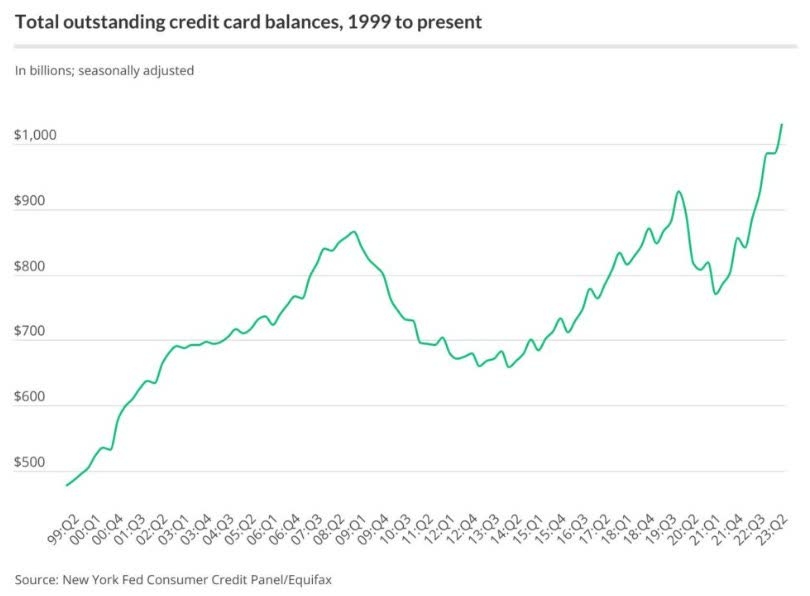

However, there are still storm clouds present which support the slowdown that is approaching. To maintain their pace of spending consumers have pulled out their credit cards. Outstanding credit card debt has risen 17% in the past year. That is not sustainable. Credit card borrowing is now “super-expensive”.

Consumer credit (www.newyorkfed.org)

While there may be an introductory rate of 0% for a year or so, the regular rate jumps to 20-25% thereafter. For all credit cards, the average APR in the second quarter of 2023 was 20.68%. No matter how we spin this, credit card borrowing is not a reliable source of spending over the longer term.

However, I’m not ready to fall into the same trap and start declaring the consumer is dead just yet. First of all the employment scene is still robust. When people have jobs they will spend. Credit cards may well be a significant source of funds for consumers for a while longer because Consumers do not have a lot of debt outstanding. Monthly payments on all types of consumer debt – like rent or mortgage payments, car loans, credit card balances, and student loans – as a percent of income is very low. Household balance sheets were strong before the pandemic and were fortified with the trillions handed out in stimulus payments. They won’t deteriorate to a point that spells trouble overnight. Rest assured there are forces in place to change the consumer scene, especially when we review what is going on with inflation, but at the moment it’s not a dire situation.

INFLATION AND ENERGY COSTS

Inflation has been going in the right direction but an improvement from here to the “goal” is going to be difficult and that is where I have been correct since this issue hit the scene. That view was based on exactly what we are seeing today – Oil prices are back around the $90 level, a 28% increase since June. Given the war on fossil fuels backdrop in the US, this was one of the easiest calls I’ve ever had to make. Oil prices were going to remain resilient despite stunts like depleting the Strategic Petroleum Reserve. That was never going to make a difference, and it hasn’t. That exercise simply proved the point that the folks in charge of policy realize oil prices have to remain subdued to help foil inflation.

While energy prices are excluded from the calculation of the core rate of inflation, the reality is that they filter into other sectors of the economy. Heating and cooling costs, fuel for consumers, the airlines, and probably the biggest impact cost of moving goods around by truck and rail. Therefore the Fed’s job is challenged again, and higher rates may lie ahead. My call for a 6% Fed funds rate may yet come to fruition, as the Fed will be “fine-tuning” its stance to ensure inflation stays depressed. JP Morgan’s Jamie Dimon has increased his forecast for a Fed funds rate of 7%. The bulk of the Fed’s work may be done, but the “higher for longer” call remains, and the market is just now catching on to that concept.

In the near term, the Fed has enough “cover” to sit tight. It didn’t seem plausible to raise rates amid the auto workers’ strike, a potential government shutdown, and an uncertain economic environment. So the “expectation” for the Fed to do nothing at the last FOMC meeting came to fruition.

Once again, the FED made their stance VERY clear, and one would think by this time investors should be realizing it. Then again, we saw many of the gurus calling for rate cuts ALL during this year. There is a contingent that remains in a state of denial when it comes to this inflation/interest rate situation, and they’ve played a part in keeping stocks resilient. Depending on the data, the door remains open for more rate hikes. While the “market” is having trouble digesting that, none of this should surprise anyone.

The idea that the Fed is done with just one more hike is something I can’t agree with today. Earlier this year I floated the notion that despite the Fed’s hiking program, it was still not restrictive enough to get the desired effect. At that time I argued that a Fed funds rate of 6+% could be in our future. Months have gone by and if the Q3 GDP forecast of 4% comes to fruition, it sure looks like the Fed needs to remain aggressive. Not only that but rest assured the Fed won’t leave this inflation fight until they hit the target and that is going to be one issue to contend with as we enter Q4.

THE PULLBACK

Now that the market has consolidated the big rally from late spring through early summer, several major indices and sectors are forming sideways patterns as investors try to weigh the pros of stronger economic data against the trajectory of corporate earnings and the nagging inversion of the yield curve. Regarding earnings, the BULLS and BEARS can each make a good case, as it remains a fluid situation as rates rise. Regarding the yield curve, there isn’t much positive to say. Historically, inverted yield curves and deeply inverted yield curves haven’t been particularly positive for equity prices (or ultimately the economy), so it’s hard to dismiss or play down their importance. Covid has caused a rewrite of all the playbooks, and maybe it will end up rewriting the yield curve script, but it shouldn’t be dismissed.

In essence, there is little change to the MACRO scene, the issues are there and they are firmly embedded in the backdrop. Storm clouds are present and it’s a tossup if they dissipate or accumulate to form a severe storm in the near term. There could be a period of blue skies, but the potential for turbulence will continue to hover over this investment scene for quite a while.

The Week On Wall Street

After three straight weeks of declines for the S&P 500, the final week of trading in September began with a modest bounce on Monday. Tuesday brought one of the worst days for all of the indices as every major index lost more than 1%. It was across-the-board selling as all eleven sectors were lower.

The indices stabilized on Wednesday posting a ‘flat” session for the major indices. However, the most oversold index, the Russell 20000 (IWM) finally bounced posting a gain of 1%. Market participants took that “mixed” session and turned it into a winner on Thursday. that adds more to the view that a bottoming process is underway.

The last day of the week, month, and quarter resulted in “window dressing” that left the indices searching for direction. Like the month and quarter itself, the day ended on a weak note.

THE ECONOMY

GOVERNMENT SHUTDOWN

Senate action on a continuing resolution and the House voting to start debate on four government funding bills this week represents incremental progress. Still, Congress remains far from an off-ramp that avoids a government shutdown.

Recent signals, including the policy details of the Senate’s CR (With no border funding, it will be DOA in the House) and the House moving forward on consideration of its own spending bills that establish a negotiating position, indicate Congress is trending toward a shutdown. That sets up a battle over policy priorities. More spending vs. less spending and border security vs. the status quo at the southern border. While headlines are likely to remain focused on process volatility, I suggest investors should expect limited market impact from a shutdown scenario.

According to Wikipedia, since 1990, there have been six prior partial or full Federal Government shutdowns in the United States. The length and depth of these shutdowns have varied widely from two shutdowns that lasted just 3 days to the most recent in late 2018 and early 2019 which lasted over a month.

Bespoke Investment Group;

The S&P 500’s median performance from a month before the shutdown started to one month after it ended was a gain of 5.5% with positive returns five out of six times.”

Past shutdowns have been a lot of noise signifying nothing.

GDP

U.S. real GDP growth was unrevised at 2.1% in the final version versus the second look and slower than 2.4% in the advance release. After the annual revisions, Q1 growth was bumped up to 2.2% from 2.0% and Q4 was left at 2.6%. The core PCE rate was unchanged at 3.7%. Real final sales growth slipped to 1.8% (2.0%) and is down from 2.2% in Q2 and 4.2% in Q1.

INFLATION

The PCE deflator rose 0.4%, double the prior 0.2% gain. It’s the hottest since January’s 0.6% jump. However, the core rate was up just 0.1%, half of the 0.2% previously. It is the slowest going back to November 2020. Meanwhile, the 12-month headline pace accelerated slightly to 3.5% y/y from 3.4% (was 3.3%) y/y. The annual core rate slowed to 3.9% y/y, still hotter than the 2% goal, from 4.3% (was 4.2%) y/y. Nevertheless, the trajectory remains southbound, good news for the Fed, and is the slowest since May 2021.

MANUFACTURING

The Chicago Fed National Activity Index was –0.16 in August, down from +0.07 in July, an indication of slower economic growth.

Richmond Fed manufacturing index bounced to 5 in September after edging up to -7 in August. This breaks a string of 16 straight months in negative territory (contraction) and is the highest since April 2022.

Dallas Fed’s manufacturing index slipped 0.9 points to -18.1 in September after edging up 2.8 ticks to -17.2 in August. This is the 17th consecutive negative print with the -29.1 in May being the weakest since the -48.5 in May 2020. The components were mixed.

CONSUMERS

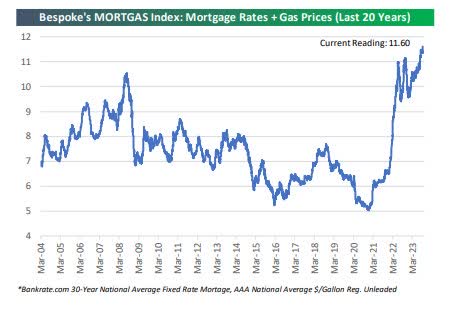

The MORTGAS index was unveiled a couple of weeks ago by Bespoke Investment Group. This is a sum of the 30-year average national fixed mortgage rate and the average national price for a gallon of gas. With mortgage rates hitting new multi-decade highs of 7.75% this week and gas prices closing in on $4/gallon, our MORTGAS index is also ticking to new highs daily. We’re going to need to see some relief on both of these fronts or else the consumer is eventually going to break.

MORTGAS (www.bespokepremium.com)

The U.S. consumer confidence dropped to a 4-month low of 103.0 in September from 108.7 in August. Today’s consumer confidence drop joins a Michigan sentiment decline to 67.7 from 69.5 in August.

Consumer Confidence (www.conference-board.org/topics/consumer-confidence)

Consumer confidence has remained well below pre-pandemic levels highlighting the issues that are present in the economy today.

For the analysts and skeptics who weren’t buying the shrinkage (theft) arguments that major retailers were reporting, they may want to buy into the reality of the situation. Target (TGT) has announced it will close nine stores in major US cities due to theft and violence.

This is a real problem that continues to be ‘dismissed’. The economic impacts of the out-of-control crime spree in major cities are going to have a major impact on consumers.

The Sign of the Times.

62% of students say they will boycott payment on their debt. The good news, consumer spending doesn’t take a big hit, the bad news inflation stays stubbornly high. The other news – it’s a sign of the times, and I’ll leave everyone to decide what is ‘right’ and what is ‘wrong’ with this picture.

HOUSING

This month’s data is quite sobering.

New home sales continue to bounce around, with an 8.7% August drop to 675k after 31k in revisions that left a 17-month high pace of 739k in July. The median price fell 1.4% to $430,300 in August. Prices remain well above the pre-pandemic all-time high of just $343,400 in November of 2017. Home inventories rose to 436k, leaving this gauge still below the 13-year high of 466k in October, while the month’s supply of homes rose to 7.8.

The new home sales and median price data reflect what continues to be a remarkably limited hit to the sector from elevated mortgage rates that have disqualified many buyers. Sales are supported by the climb in new home completions from the housing starts report to a 16-year high in February.

Pending home sales plunged 7.1% to 71.8 in August, much weaker than expected and matching the all-time low seen in April 2020. This is the biggest monthly drop since September and follows a downwardly revised 0.5% bounce in July to 77.3. Sales declines were seen across all four regions, though led by a 9.1% drop in the South and a 7.7% decline in the West. The 12-month pace of decline accelerated to 18.8% y/y from 14.1% y/y.

EARNINGS

Starting with Q3 ’23, the SP 500 faces weaker comparisons from a year ago: the SP 500 EPS and revenue estimates started to fall off in Q3 and Q4 of 2022.

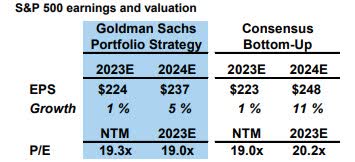

Goldman Sachs came out with their updated EPS view last week. Notably, they see next year’s earnings growth at about half (+5%) of the consensus view (+11%).

Earnings Forecast (www.goldmansachs.com/what-we-do/research/)

We’ll get a much better feel for how ’24 is going to shape up during and after the Q3 reporting season.

FOOD FOR THOUGHT

Another government shutdown looms with a deadline set for October 1st. There is little need for panic, the government has been shut down 21 times before this new deadline arrives.

There will be plenty of rhetoric from both sides, but what this boils down to is an attempt at securing the border and taking a bite out of spending. All else reported is pure noise. No matter what side of the argument you are on regarding these two issues, they are going to have a HUGE economic impact. The trend on both is unsustainable.

Illegal border crossings have been ~ 8 million since January 2021. The situation is getting worse by the day for many mayors who can no longer provide basic services.

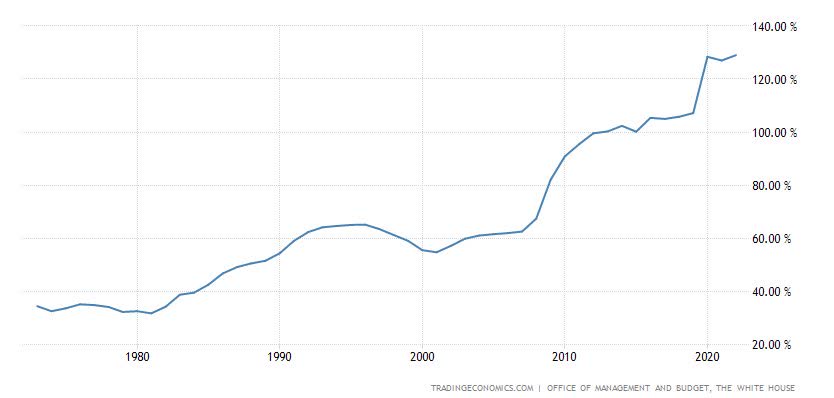

I covered the debt issue in detail recently, and here is yet another alarming statistic. The Debt to GDP ratio stands at 123% in 2023. Before the Financial crisis that ratio ran about half (60%) of what it is today.

Debt/GDp (www.tradingeconomics.com)

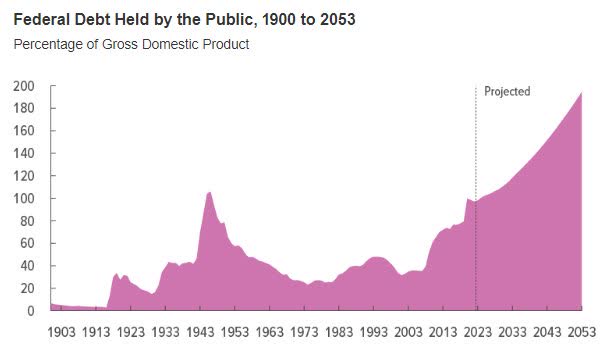

The Congressional Budget Office projects this debt-to-GDP ratio to only get worse. Debt is projected to rise in relation to GDP, mainly because of increasing interest costs and the growth of spending.

Debt/GDP forecast (Outlook for the Budget and the Economy)

Nobody wants to hear me say it again, but here goes — the fact is there is no room to spend trillions on “climate change issues”.

The Senate has done plenty of complaining about what the “House” has or has not done regarding the funding issue. In the interim, they offered no solutions of their own and finally decided to get involved yesterday.

In addition to what is absolutely “needed,” there are other legislative riders unrelated to fiscal 2024 appropriations that were in the mix for the Senate’s interim funding bill. Before we get to the ‘riders” there is more aid to Ukraine, An extension of the expiring National Flood Insurance Program, a three-month extension of expiring Federal Aviation Administration spending and revenue-collection authority.

A package of health care “extenders,” although the details weren’t clear. Lawmakers in both chambers at minimum want to renew expiring mandatory funding for community health centers and teaching hospitals as well as cash benefits for low-income households under the Temporary Assistance for Needy Families program.

Also in play was a renewal of the Compacts of Free Association, known as COFA, that govern U.S. relations with Palau, the Federated States of Micronesia, and the Marshall Islands. Economic aid to Micronesia and the Marshall Islands expires after Sept. 30, and the White House wants an extension of those provisions as well as aid to Palau, which lapses a year later, plus a bump in federal assistance.

Negotiations on a new compact with the Marshall Islands were still ongoing as of Monday, though a senior administration official reported “substantial progress” in those talks, which are occurring this week in Washington as part of the U.S.-Pacific Island Forum Summit.

There is no will to slow down spending nor address the border issue, both of which will eventually strangle the US economy.

In the short term, do not worry. This turns out to be a counterintuitive situation. The stock market has done relatively well during these events, and after a resolution, the following 30 days have been very BULLISH.

That’s the near-term outlook. However, if progress isn’t made soon, the MACRO economic situation gets worse by the day. According to Bloomberg chief US economist Anna Wong, each week of a shutdown would cut 0.2 percentage points from quarterly GDP.

The FTC vs. Amazon

They have had their share of failures in high-profile cases, and now the FTC is going after “BIG- game” in targeting Amazon (AMZN). That’s not an opinion, here is the FTC Chief’s track record of failed attempts. The FTC’s chief spent a good portion of her adult life targeting big business, with Amazon her prized target. Her claim to fame at law school was a paper entitled “Amazon’s Antitrust Paradox,” in which she argued that;

“Amazon was too successful to go on without government obstruction”.

This isn’t law school, it’s the real world with real people and real consequences. Somehow we are to believe that lower prices and faster delivery times that are unprecedented are bad for consumers. Not to mention the company provides a platform for 9.5 million sellers and employs 1.5 million people. Amazon’s groundbreaking innovation has made the largest US retailer, Walmart (WMT), a better retailer with a much improved online experience for consumers. United Parcel (UPS) has also been a huge beneficiary of the evolution of “Amazon”.

“Proving” that someone has been harmed by Amazon’s existence won’t be so easy. The FTC will now spend a fortune in taxpayers’ money and three-quarters of an eternity to prove her assertions. The blatant attack on business and capitalism has far-reaching effects than just this case. Cripple big business and you cripple the economy. Attacking an enterprise because in HER words “they are too successful” is the “hallmark and signature” of anti-capitalism.

From an investment perspective, I am not a seller of AMZN. However, I will admit it makes a very positive situation a problematic one. The technical picture shows the stock is in “no man’s land”, but if this week’s low holds then there is a decent probability the damage from this announcement is done.

The fundamental story is sound and the longer-term uptrend is decidedly bullish. I’ve issued a special ALERT to members of the SAVVY service that outlines the various ways to take advantage of this situation.

At the end of the day, plenty of time and money will be spent debating both sides of the case but hopefully, for the sake of consumers, and small businesses, nothing will change.

Investing in a stock market where successful companies are targeted using a self-proclaimed anti-business “agenda” makes investing in general much more difficult. Investors who are avoiding China because of its recent mindset toward business might want to take a look at what is happening here in the U.S. as well. China is a communist regime that marches to the government’s agenda so its stance on business is somewhat understandable. Not so in what is still a Capitalist environment, and therein lies the real issue.

The Daily chart of the S&P 500 (SPY)

The S&P 500 snapped out of its 10-day funk this week and finally showed some signs of stabilizing just above the all-important 200-day moving average.

S&P 500 (www.tc2000.com)

Just about every market technician has that as their “line in the sand”. When everyone is thinking the same way, we usually find out no one is thinking. My thoughts led me to believe one of two scenarios might play out. Either the S&P never gets to the “target”, stabilizes, and goes higher, OR the index falls right through the so-called support level, and scares a majority of traders out of the market before stabilizing.

Given the price action this week, the first scenario might be playing out. The problem with going all in on that notion, the market can easily reverse from here and head lower. What we could be witnessing is nothing more than an oversold bounce that will fall apart quickly.

That falls into the category of what I’ve come to call a “50-50 market”. There is not much conviction to SELL, nor is there enough conviction to BUY. Certainly, not enough of a push either way to give an investor enough reason to do much of anything. One thing that is now very apparent – the intermediate top on July 28th that was posted on the chart at the beginning of August is now in fact a correct call.

FINAL THOUGHTS

If you want to boil the current market down to three key variables, the 10-year Treasury yield, the price of crude oil, and the US dollar are a great start. If the uptrends in crude oil and the dollar start to weaken, it might bring the 10-year Treasury yield back under 4.3%, so the chart to watch is the 10-year Treasury note. As of the close on Friday that has yet to occur, and unless the market adjusts to this new rate environment, equities are going to struggle.

The opening quote should remind investors to deal with reality and avoid the everyday noise of the headlines. Trade the market that is in front of us and not the one that we want. We’ve seen a perfect example of that lately. It sure seems like the bulk of the investment world just couldn’t come to grips with interest rates at these levels and have a hard time believing they will stay there (or higher) for a while. While the dates of any cuts have been pushed back (finally), some are still calling for rate cuts in 2024.

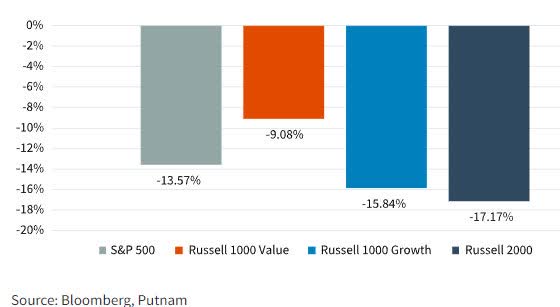

The more time that goes by with the evidence in front of me, I’m not so sure they will be correct. Investors also better be careful what they wish for. Given this economic backdrop, a rate cut could signal a disaster has hit the economy. In the six and 12 months after the Fed increased rates for the final time in a cycle, equity indexes on average had positive returns, in line with historical averages. Still, while equity markets finished higher, there was often volatility. The following chart shows the average maximum drawdown for the indexes in the 12 months after the last hike.

Fed Rate Cut Perf. (www.bloomberg.com/professional/product/research/)

The S&P 500 exhibited an average maximum drawdown of 13.57% in the 12 months after the last rate hike. Market participants have witnessed how this rate “cycle” has been different and that leaves the door open for more uncertainty. The REALITY is when the Fed is done there may not be the “smooth sailing ” many anticipate.

THANKS to all of the readers that contribute to this forum to make these articles a better experience for everyone.

Best of Luck to Everyone!