benedek

Broadstone Net Lease, Inc. (NYSE:BNL) jumped on my radar again lately as the stock price plummeted over 10% in just a few days. I actually already rated the stock as a Buy in my previous article published on July 24, however since then the stock dropped an even more astounding 15%. I believe the market sold the stock primarily in light of recent events happening to W. P. Carey Inc. (WPC), a similar company that has announced a surprising dividend cut and that has clearly scared income-oriented investors (more about this below).

In my opinion, the price movement has created a much more intriguing investment as nothing fundamentally changed for the business, while the dividend yield jumped to a very high 7.8%.

Great, diversified portfolio

I am going to provide a succinct analysis of what makes Broadstone Net Lease an intriguing proposition, while for a more detailed review I invite the reader to visit my previous article. BNL is a net-lease REIT focused on single-tenant commercial real estate properties that has managed over the years to build a very valuable portfolio of 801 properties, primarily spread over 44 U.S. states and a few also in Canada.

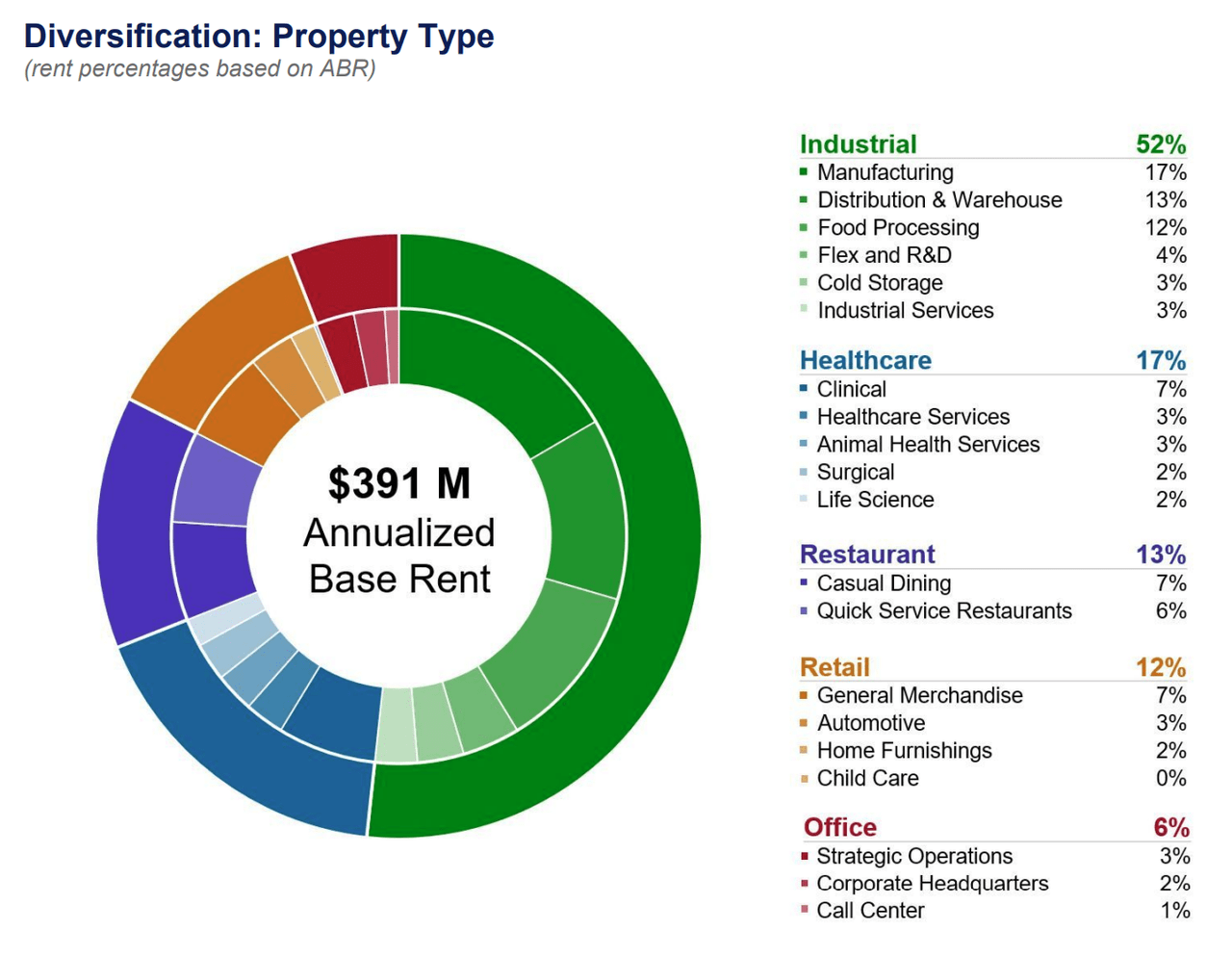

One of the main benefits of BNL is the great diversification it offers in relation to its tenant base. The company generates about $391 million of Annualized Base Rent from tenants operating in the industrial (52%), healthcare (17%), restaurant (13%), retail (12%) and office (6%) sectors. BNL is also not particularly exposed to any single tenant given that its biggest customer (Roskam Baking Company) only represents about 4% of ABR, while the top 10 and top 20 tenants increase the concentration share respectively to about 19.4% and 32.1%.

Although only 15.3% of BNL’s tenants are actually Investment Grade, any metric provided by the company actually suggests a very high quality portfolio. As per the latest results, BNL enjoys 99.9% rent collection and 99.4% occupancy rate (only 2 out of 801 properties are currently vacant).

BNL Investor Presentation Q2 2023

BNL also focuses on net-lease contracts, which are generally very stable thanks to their very long duration. The Weighted Average Remaining Lease Term of the entire portfolio is over 10 years, and it also enjoys a passive Weighted Average Annual Rent Increase of 2.0%.

Management focused on only the very best deals

During the second quarter earnings call the management highlighted how during the year they scrutinized over $17 billion of potential deals, but they applied a particularly stringent framework that resulted in a very small number of transactions actually taking place during the quarter. The most important takeaway in my opinion is that BNL is in a position of being free to only invest when a great deal presents itself, because it has no need to grow just for the sake of growth. Management expressed very clearly this message:

Our flexible balance sheet and conservative leverage profile coupled with proceeds from dispositions at attractive cap rates in the high 5% to low 6% range will support our growth strategy in the second half of the year and into 2024. As I have said in the past, BNL is currently in a position to make decisions that we want to, not decisions that we have to, an especially important distinction in today’s real estate market.

Management had something to show for it, as few deals were actually closed during the quarter, which further proved their strategy. During the second quarter 2023, the company acquired 3 industrial properties for about $20 million at a very healthy initial cash cap rate of 7.4%. These properties are currently rented and the weighted average lease term is over 14 years, and it includes 2.0% annual rent increase.

At the same time, the company had the chance to dispose of some assets at a great value. During the quarter, 4 properties were sold at a weighted average cat rate of 5.6%, a rate that implies they were either underperforming assets or properties that still retained good market value. The company sold these properties for about $69 million, while their purchase price was $52 million.

Why the stock got punished so hard?

So what exactly happened to the share price? As briefly touched, the stock is not only down since its IPO level about 12%, but even just in the last week or so the stock has dropped precipitously about 11.5%. The main culprit of the recent weakness in my opinion is a spillover effect of what happened to W. P. Carey Inc. (WPC), one of the biggest and most popular net-lease REIT available on the market. Despite an uninterrupted streak of growing dividends lasting for decades, management has surprised the market by announcing a dividend cut. Nothing rattles REIT investors more than a surprising dividend cut, which understandably has spooked investors into selling off similar companies indiscriminately. For reference, WPC’s share price cratered about 15% just in the last few days and has received few downgrades since.

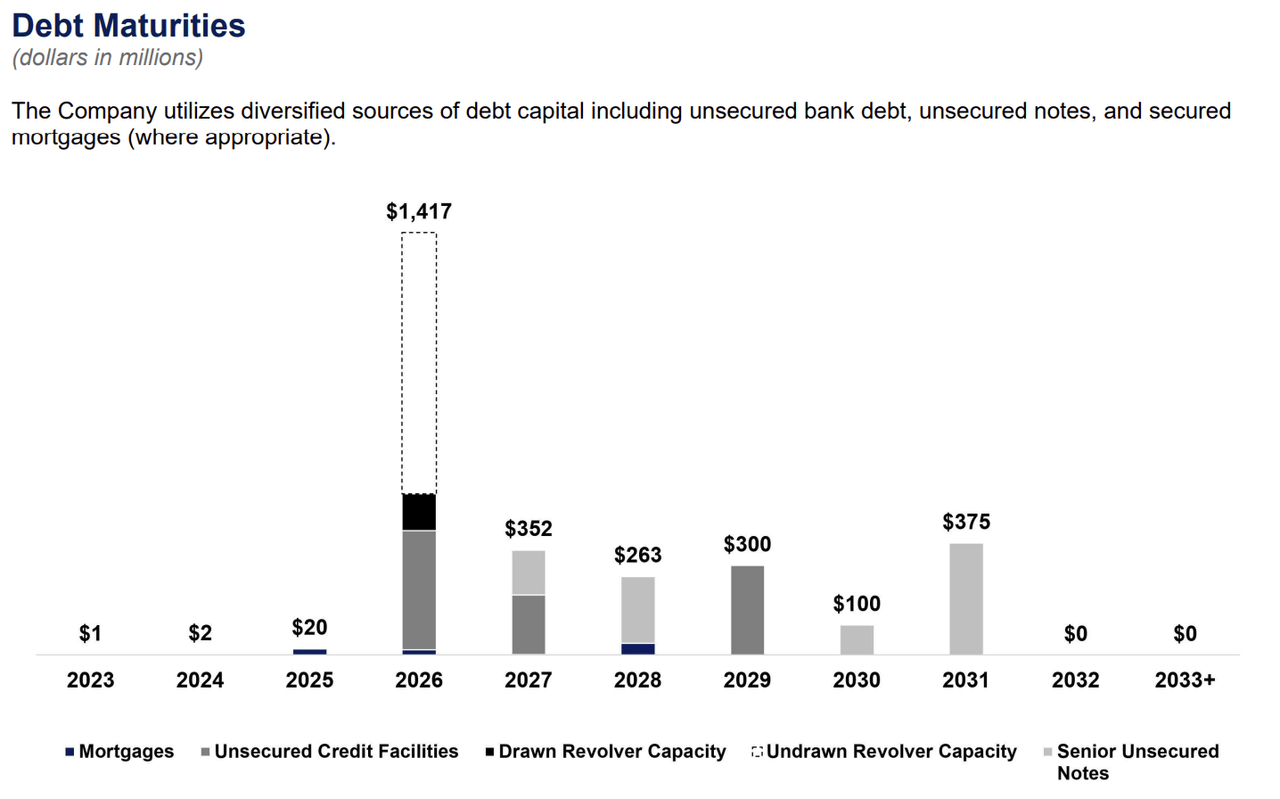

However, despite many similarities between the two companies, there is actually one crucial difference. WPC had major upcoming debt maturities, with over 58% of outstanding debt in need of refinancing between 2023 and 2026. Any company that is in need to refinance such a big portion of their debt will inevitably soon have to incur in much higher interest expenses. On the contrary, BNL has virtually no debt maturity at all until 2026 and all of its debt is fixed at a weighted average interest rate of 3.7%. It is true that the Federal Reserve is hinting at interest rates to stay high for a long time, but their most recent forecast still presumes that rates will drop to about 4% by the end of 2025. If that happens, BNL will be able to refinance their debt almost at the same cost as in the past.

No meaningful debt maturity until 2026 (BNL Investor Presentation Q2 2023)

The market is also clearly discounting a subdued growth in the short term. Management has recently reiterated their guidance for FY2023 of AFFO per share of about $1.40 to $1.42 which suggest basically no growth for the year. Some growth is coming internally from the rent escalators built in over 96% of the rents currently in place, but external growth coming from acquisitions will inevitably be muted for the foreseeable future due to the market environment. Management has highlighted how the stock price is currently too depressed to raise capital via equity issuance, while obviously debt has become way more expensive than in the past due to the current level of interest rates set by the Federal Reserve.

In my opinion, the lack of short-term growth does not impact the investment thesis, as investors are very well compensated by a current dividend yield of 7.83% and about 2% internal growth from rent escalators. That is a sufficiently high and safe return in my opinion while waiting for the macro environment to turn.

Few tenants are having difficulties

As with the past quarters, management has shared updated commentary around Red Lobster, Carvana and Green Valley Medical Center, the three watchlist tenants that are experiencing serious hardship.

While Red Lobster and Carvana have both shown positive signs (return to profitability, growth, cost-cutting measures), the latter has failed to achieve previously-set milestones. The tenant still hopes to start the operations at the property during the fourth quarter, but there is definitely less optimism on that front due to the difficulty in opening up a new hospital.

Although it is never good news to have some tenants losing money, it is still worth highlighting that thanks to BNL’s portfolio diversification these three tenants only represent a fraction of the total ABR. More specifically, Red Lobster and Carvana have a combined impact of 2.8%, while Green Valley Medical Center is undisclosed, which indicates an impact probably lower than 1%.

Valuation and key takeaways

I already liked BNL the last time I reviewed it at about $16.7 per share, I like it much more at today’s price. I think the risks are clear (smaller scale compared to more established peers, unfavourable macro environment, few tenants toying with unprofitability), but they are very well mitigated in my opinion.

Not only does BNL offer one of the highest dividend yield that is considered safe, but is also trading at a much cheaper valuation compared to rivals.

The stock is currently trading at a Price to AFFO of just 10.21, much lower than some of their larger peers such as Realty Income (O) at 12.61 or Agree Realty (ADC) at 14.27. I don’t foresee a higher repricing for the real estate sector any time soon, but at some point interest rates will stabilize and most likely drop to a more accommodating level (in the 3% to 4% range). When that happens, expect many REITs to be priced at meaningfully higher valuations, which will unlock nice capital gains for current shareholders. Patience is the name of the game, and BNL offers in my opinion the right risk-reward profile while being rewarded with a very high dividend.