sturti/E+ via Getty Images

Investment Thesis

With a much lower FW PE ratio compared to FY22, I wanted to take a look at Interface’s (NASDAQ:TILE) financials to see if it could be a candidate for a long-term investment. A huge pile of debt and unimpressive profitability and efficiency metrics, coupled with sluggish revenue growth, keep me away from investing right now, even though the valuation analysis tells me it is cheap, therefore, I give it a hold rating. I would like to see debt be paid down more aggressively and the company acquire some catalysts that could propel the company’s revenue growth.

Briefly on the Company

The company is a global manufacturer of commercial flooring with an integrated selection of carpet tiles and flooring. It sells modular carpet products, and it operates in most of the world, The AMS (Americas) is one segment, while the EA encompasses Europe, Africa, Asia, and Australia.

Financials

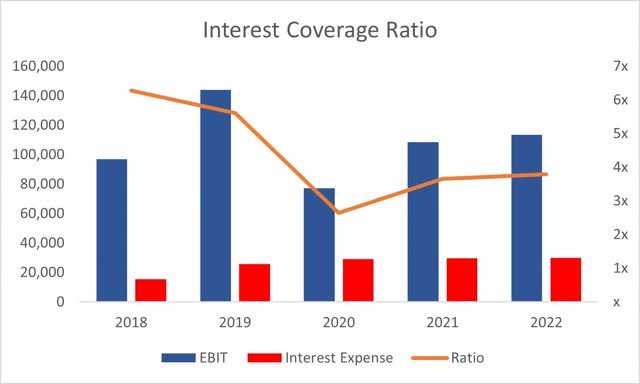

As of Q2 ’23, TILE had around $93m in cash against $465m in long-term debt. That is almost as much as the company’s market capitalization. So how worrisome is this debt? Well, historically, the interest coverage ratio has been hovering around 2x-6x, which is above what is considered to be a healthy interest coverage ratio (2x being healthy). I like to be more stringent, so I look for at least a 5x. As of Q2, the company’s coverage ratio stood at around 2x, so it’s decent, however, a little lacking for my standards. We still have two more quarters to see how EBIT develops, which I think will be higher than as of now.

Coverage Ratio (Author)

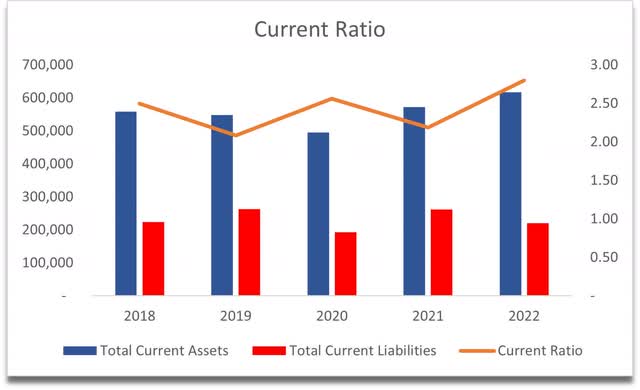

TILE’s historical current ratio has been very strong and slightly above what I consider to be an efficient current ratio range of 1.5-2.0. I believe that range is a good balance between the ability to pay off short-term obligations comfortably and still have assets like cash to expand operations. So, it is safe to say the company has no liquidity problems.

Current Ratio (Author)

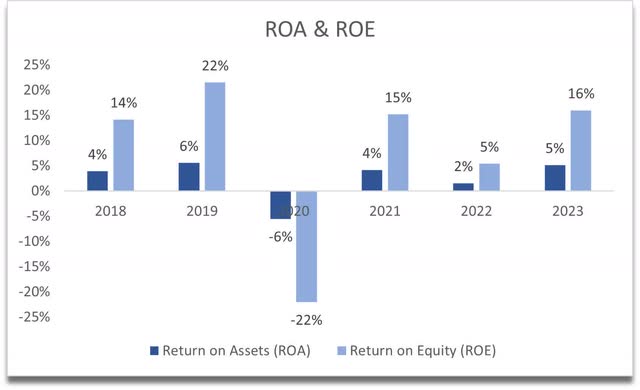

The company’s ROA and ROE have been much better in the past, which seems to be affected by goodwill impairments as of FY22, however, if we assume no impairment charges happen in FY23, then ROA and ROE seem to be quite decent in my opinion. This tells me that the management is utilizing assets and shareholder capital efficiently. ROA is at the minimum that I require, while ROE is around 6% higher than my minimum.

ROA and ROE (Author)

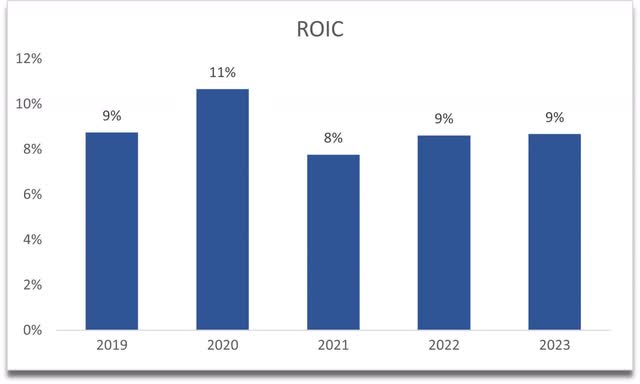

The company’s ROIC is not the worst, however, I would like it to go over 10% in the coming years as that would tell me the company has a competitive edge and a decent moat. The management is good at allocating capital at decent returns. I like that the company has been consistent in this metric, and I would look for it to continue in the future.

ROIC (Author)

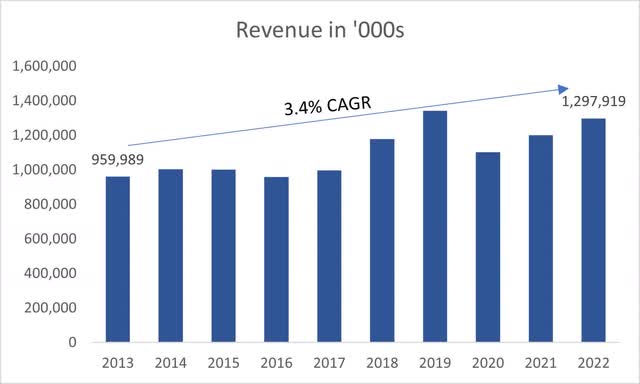

In terms of revenue growth, the company hasn’t seen spectacular growth overall. In the last decade, it averaged around 3.4% CAGR and I don’t see how it can outperform that in the future. So, I will anchor my valuation to the historical average.

Revenue growth (Author)

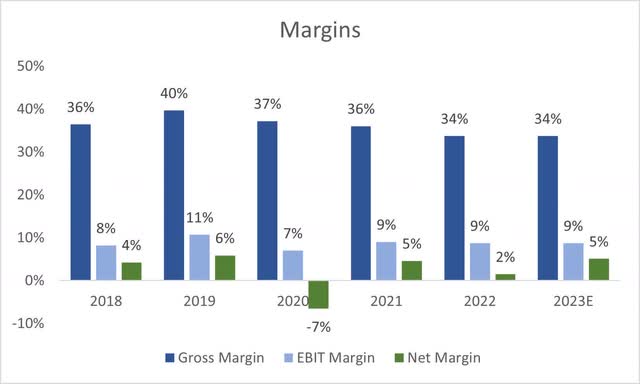

Margins saw a large decrease in FY22 due to the impairment charge of around $42m related to goodwill. If we take it out and look at non-GAAP, the company’s margins have been decent, and I estimate we will see similar results as in FY21 going forward.

Margins (Author)

Overall, it seems like the company is operating quite efficiently, with a decent competitive advantage and a moat. I also estimate that the company will see better results in FY23 if we take out the goodwill impairment charges. I don’t see the company’s revenue growth accelerating and that is what I believe is keeping the company’s FW PE ratio so low.

Valuation

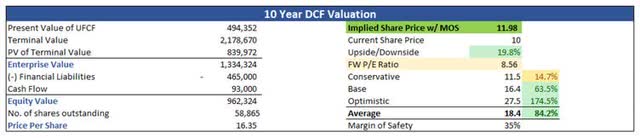

For my base case scenario, as I mentioned earlier, I will go with about the average the company achieved in the past, which is around 3.5% CAGR for the next decade. For the optimistic case, I went with a 5.5% CAGR, while for the conservative case, I went with a 1.5% CAGR to give myself a range of possible outcomes. I believe that all these scenarios are likely to happen in the future, an average of the three would be a good indication of the company’s growth.

In terms of margins, I decided to improve gross margin by around 600bps or 6% by the end of FY32, while keeping operating margins as they are for the analysis. I believe it is reasonable to assume the company will be able to achieve higher profitability and efficiency in the future, as just in FY19, the company saw much higher gross margins. With my assumptions, I’m improving gross margins to around FY19’s mark. These assumptions will bring net margins from around 2% in FY22 to around 10% by FY32.

Since the company is very small, I will require a higher margin of safety as these types of companies tend to fluctuate quite a lot more on low-volume trading and the company’s beta is around 2. I went with a 35% margin of safety, which I believe is going to be sufficient for my risk tolerance. With that said, the company’s intrinsic value is around $12 a share, meaning the company is currently trading at a discount to its fair value of around 20%.

Intrinsic value (Author)

Closing Comments

Even though the company seems to be cheap on paper, I am not a fan of the company’s high levels of debt. As I said earlier, I do look for companies that can easily cover interest expense on debt at least 5 times over. A coverage ratio of 2 for me is a little tighter than what I would like to see. I would like to see the company start to pay off the massive debt pile.

The lack of growth is also one factor that keeps me away from investing. A lot of investors may see it that way too and not invest, which will keep the company’s PE ratio on the floor, even though the GAAP P/E ratio is distorted by the impairment charges.

I’ll keep an eye on how the company’s financials develop over the next couple of quarters and reassess if needed.