Jean-Luc Ichard/iStock Editorial via Getty Images

Here at the Lab, today we are back to comment on Engie (OTCPK:ENGIY). Since our last update, Challenges For Mature Businesses, the company has been flat at the stock price level. We estimated a target price of €15.3 per share ($16.5 in ADR), providing a neutral rate, and Engie’s current stock price is pretty in line with our twelve-month forecast. However, as noted, with a 9% Yield On 2023 Numbers, the total return is double-digit.

Mare Past Analysis

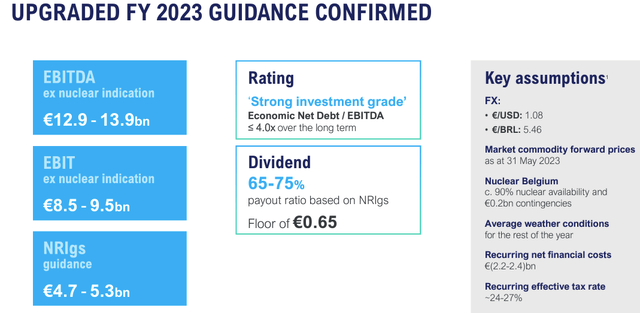

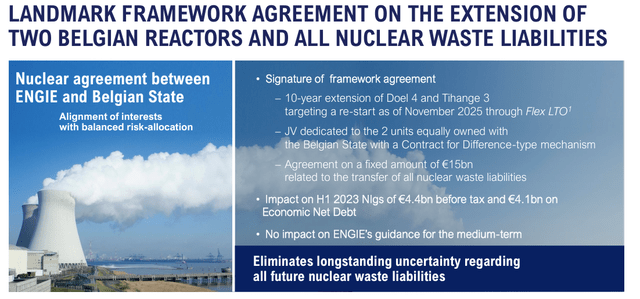

Before looking at the Engie strategic plan, we deep-dive the H1 results. Firstly, we look at how results were compared to expectations. We are impressed that the company delivered solid numbers (up from H1 2022) and reaffirmed its guidance, which was already upgraded. Notably, we report how the nuclear deal’s net debt impact is less than expected (€4.1 billion vs. €4.5 billion). Economic net debt/EBITDA is now at 2.7X and already factor the additional charge for the nuclear deal. Despite a normalized energy price environment, the GEMS division (energy marketing & trading) reported €2 billion in results. Post H1, we believe that investors would favorably see the company thanks to better margins, cash flow evolution, and a balance sheet in better shape.

Engie H1 Financials in a Snap

Source: Engie Q2 results presentation

Why are we still Neutral?

- Our analysis of Engie’s 2023-25 business plan suggests that 2024 guidance was rather conservative. This might imply that there is room for improvements or otherwise negative earnings surprises over the medium-term horizon;

- There are investors concerned about negative news flow on potential additional nuclear provisions. Here at the Lab, we believe this risk is now more limited, but we still anticipate a further increase in nuclear provisions given the asset life extension (Fig 1). As a reminder, last December, Engie increased provision by €3.3 billion;

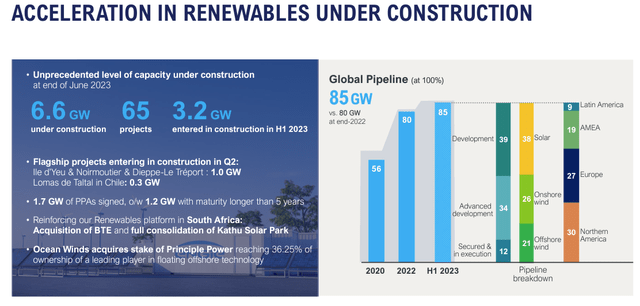

- Engie aim is to simplify its business model. There are many moving parts in Engie’s business plan (Fig 2). In addition, the company is targeting an aggressive CAPEX plan. In detail, Engie aims to increase investment by 50% with a €22-25 billion plan in the period between 2023 and 2025. This supports a renewable pipeline target of 85 GW with an impressive installed capacity (Fig 3). Here at the Lab, we already reported how comps such as Enel and Iberdrola find difficulties in delivery. This is mainly due to regulatory changes and inefficient personnel in the public administration (in 2022, Engie developed a 2 GW renewable project coming online vs. a base estimates of a 3.7 GW of annual growth in wind & solar net capacity additions);

- Our internal team positively views the transition towards cleaner energy solutions; however, execution is a risk that cannot go unnoticed. This is also one of the reasons why Enel and Engie traded at a discount versus peers;

- There might be a risk for a negative one-off due to the gas networks’ regulatory reviews, which will happen in 2024. Given the RAB remuneration-based, regulatory changes are a crucial risk that might disrupt investment return. We will have more information over Q4 for transport, storage, and distribution. This might be reflected in Engie’s future guidance, given an estimated fall in the core operating profit by the group for Networks in 2025. In the next quarter, there might be more clarity at the European level with a potential solution to reform the entire market. However, we do not believe it is going to be a game changer for our universe companies (Enagas might benefit from this development);

- Looking at the future, we anticipate less visibility on 2025 net profit delivery. We believe that Engie’s guidance is based on high commodity prices. While we see the GEMS division generate better results vs. pre-2022, we do not anticipate the company’s ability to achieve €1.1 billion of EBIT. Given more conservative assumptions on power prices, GEMS net income is set 10% below midpoint guidance;

- Here at the Lab, we aligned with the company’s 2023 EBITDA indication at €13.9 billion; however, given many question marks on energy and higher investment CAPEX, we are more skeptical about the 2025 business plan execution. This is also due to a more balanced approach between debt evolution and incremental CAPEX.

Engie Nuclear Snap Engie Activities Engie CAPEX Plan

On a positive note, Engie confirmed its payout ratio at 65%-75% of Net Recurring Income group share with an annual dividend floor of €0.65. In our estimates, we implied a DPS of €1.24 and €1.14 for 2024 and 2025. The company yield is set at an average yield of 7.85% for the next two years.

Conclusion and Valuation

At first sight, Engie’s valuation looks attractive, with an 8x P/E and a 7.5% dividend yield. Looking at the sector, Engie is at least 20% cheaper, and this discount has grown lately. Here at the Lab, we would like to see a simplified business model and a solid execution before changing our valuation to a buy rating. We like energy transition exposure and believe Engie is in the right direction. In our estimates, Engie’s wind & solar activities are on track to achieve a 30% EBITDA by 2030, but the group’s strong pipeline needs to be expected. Therefore, we continue to remain neutral. Our internal team is more supportive of Enel with a disinvestment plan, a higher exposure in renewable energy (already in place), a valuation discount, and a simplified model with less earnings volatility, given many exits in riskier countries.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.