Maddie Meyer

The curse of the Covid demand surge is that a vaccine company like Moderna, Inc. (NASDAQ:MRNA) is now reporting far higher revenues, but the company isn’t profitable anymore. Despite a promising vaccine pipeline, sales are only expected to dip in the years ahead. My investment thesis is Bearish on the stock due to the speculative nature of the business going forward and the curse of the biotech trying to recapture the glory from the 2021 to 2022 period.

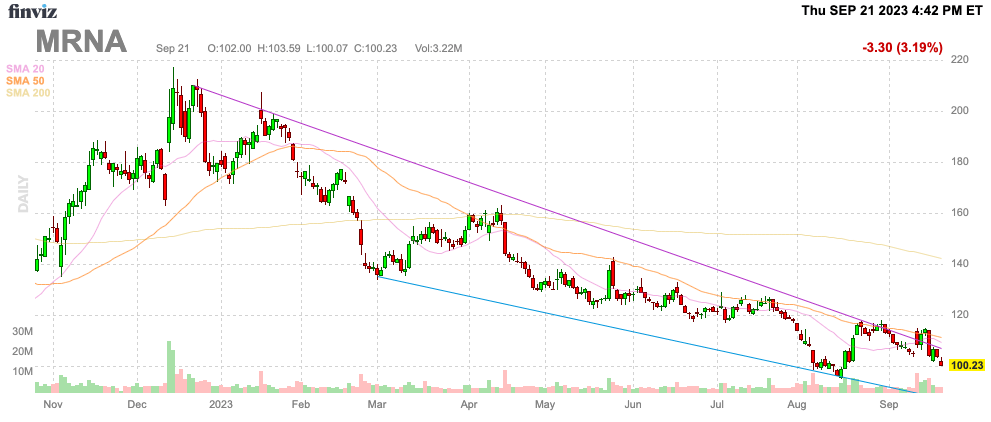

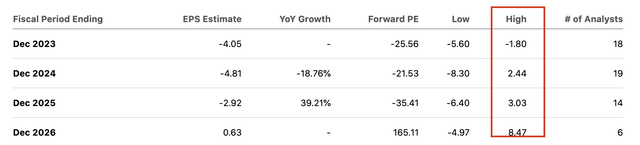

Source: Finviz

Covid Sales Risk

Back in Q2 ’23, Moderna reported a massive quarterly loss due to high spending and reduced revenues because of seasonal respiratory vaccine demand. In essence, the biotech now gets the majority of revenues during the December quarter.

The company only reported revenue of $344 million with a massive net loss of $1.4 billion. Moderna has suddenly gone from large profits to now burning a lot of cash.

A big red flag in the Q2 loss was a $464 million inventory write-down. Moderna is having a hard time accurately predicting Covid demand that has slumped fast.

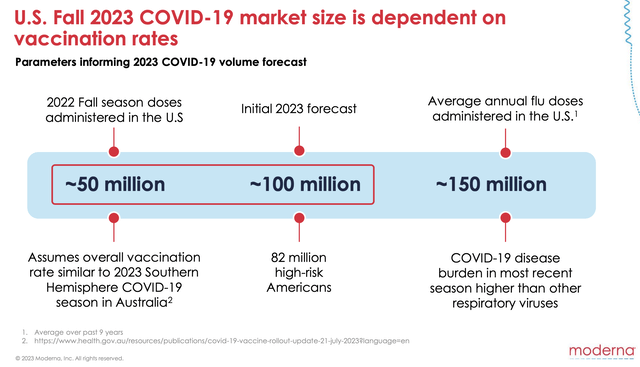

Moderna forecasts a Covid market of 50 to 100 million doses, but Pfizer (PFE) only targets ~82 million shots in the U.S. The large biopharma only forecasts 24% of U.S. adults getting the new Covid shot cutting off some market hopes for hitting the higher end of demand at 100 million shots and maybe approach the 150 million doses similar to the flu season.

Source: Moderna Q2’23 presentation

Moderna still forecasts sales of $6 to $8 billion for the year while cost of sales are forecast at a massive $3.5 to $4.0 billion. The flip side of the massive demand driven pull a few years back is that the Covid shots aren’t overly proprietary while the production costs are excessive.

The biotech has now burned $2.14 billion in negative cash flows from operations while spending another $0.35 billion on property and equipment. The total cash burn during the 1H of the year was an incredible $2.5 billion.

Moderna has a cash balance of $14.6 billion allowing the company to invest for the future, but the expanded pipeline adds additional risks to the investment story.

Pipeline Spending

Moderna spent $1.1 billion on research and development last quarter alone. The biotech is struggling to be profitable on a forecasted Covid vaccine revenue level of $7 billion due to heavy spending now that the mRNA platform has technically been proven out via the Covid vaccine.

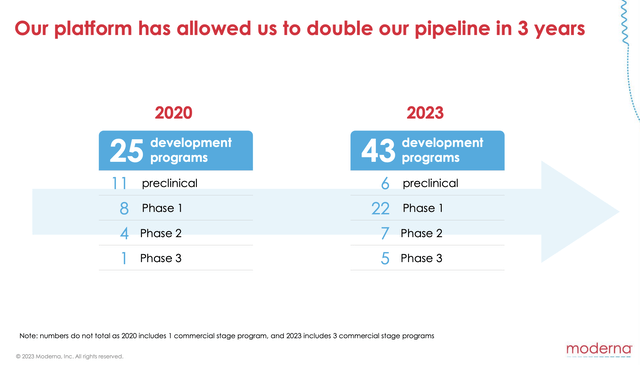

The company only spent $500 million annually on R&D until the Covid vaccine approval and revenue surge. Moderna now has a massive drug pipeline of 43 development programs dramatically increasing the costs without a blockbuster drug approval via the normal testing unlike what occurred with Covid.

Source: Moderna Business Update presentation

Moderna does have a promising combination program with the flu+Covid+RSV. The big question is how much the Covid revenues remain with a large portion of the 2023 revenues from APAs unlikely to repeat in the future.

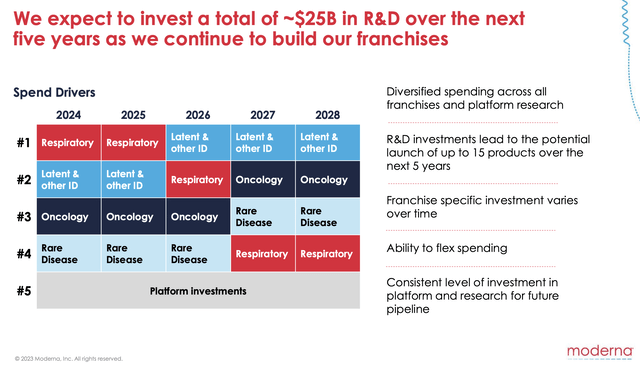

The biotech is already forecasting spending ~$25 billion in R&D over the next 5 years. The company is spending to capture an annual revenue potential of $20 to $30 billion.

Source: Moderna Business Update presentation

The big concern is that Moderna is forecasting Covid sales of $6 to $8 billion leading to $8 to $15 billion in respiratory virus sales in 5 years. The risk is that this number ends lower due to the biotech having no proprietary drug patent in this area with multiple drugs already approved for Covid and the flu.

The current consensus analyst estimates factor in massive losses for the next couple of years. The big concern is that the high-end analyst estimates appear far too aggressive, or those estimates haven’t been updated for the new reality of lower Covid demand.

Seeking Alpha

Moderna is set to report nearly $8 per share in losses over the next 2 years leading to over $3 billion in losses. These losses could even accelerate due to a spending increase on lower revenues next year.

Takeaway

The key investor takeaway is that the mRNA platform offers a lot of promises for new vaccine approvals over the next few years. Our research started under the premise of being bullish on the stock following the massive dip from the highs and the promises of new vaccine approvals for RSV and other drugs in the pipeline, but the excessive level of spending suggests management is wildly spending on new development programs.

If Moderna, Inc. consolidates focus on a more select group of drug candidates and reduces spending, our view would be more bullish. The stock might run into the Fall due to boosted Covid sales, but investors should sell any rallies.